Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

US$500 billion worth of investments needed to meet burgeoning power demand

1 minute read

In celebration of ASEAN's 50th anniversary, our APAC gas and power senior analyst, Edi Saputra, reflects on ASEAN's energy developments and what to look out for in the coming years:

Since its inception, ASEAN has grown to become the 6th largest economy in the world, with a combined GDP of US$2.8 trillion in 2017.

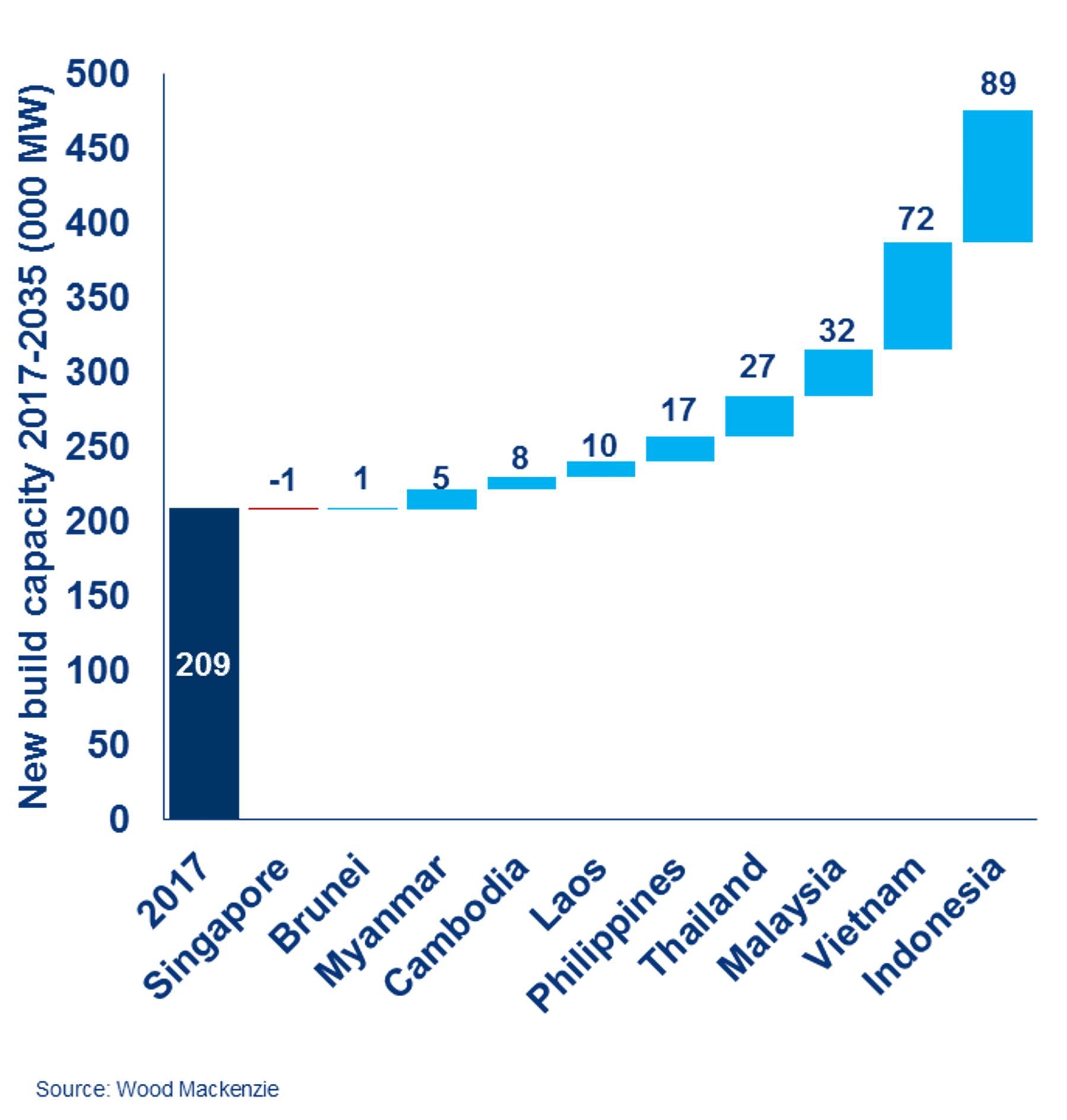

The region has installed 209 GW of power capacity as of this year, and needs an additional 270 GW of new capacity by 2035, to meets its burgeoning power demand. We estimate around US$500 billion investments will be needed to build the much needed power capacity.

Countries such as Indonesia, Vietnam, Philippines, Myanmar, Laos and Cambodia have low power consumption per capita, between 300 and 1,800 kWh/person. They are also lagging in power supply reliability, and therefore we could see a lot of development in those markets. With the region lacking the internal capital, it becomes a strong magnet for foreign direct investments.

While there are a lot of plans and aspirations for energy cooperation within ASEAN, progress has been quite limited. It has not achieved real success in terms of energy policy, when compared to the EU for instance. This is partly due to the lack of joint regulations and enforcement authority of the organisation upon its members. Moving towards a more authoritative structure may not be desirable, as ASEAN has always relied on consensus building and voluntary adoption, which has worked well so far in maintaining the cohesion.

To stay relevant however, ASEAN has to explore new ways of fostering energy cooperation among its members, instead of merely relying on individual efforts in isolation, apart from each other.

Two of the key initiatives in ASEAN's energy cooperation are the Trans ASEAN gas pipeline (TAGP) and ASEAN power grid. While there are some existing bilateral gas pipeline interconnections, the full realisation of the programme depends heavily on the monetisation of the giant Natuna D-Alpha field, which is full of challenges due to high costs and economic demands. At the same time, the arrival of LNG into the region since 2011, has reduced the urgency of this project.

LNG has changed the regional gas landscape, exposing ASEAN to the global LNG dynamics. The arrival of LNG has partly driven countries such as Singapore, Malaysia, Thailand and Indonesia, to evaluate its market structure, making the case for market liberalisation. ASEAN needs to shift its focus towards LNG cooperation, in building virtual pipeline interconnections, instead of dwelling on the uncertain initiative.

Singapore, for instance, has the first-mover advantage in LNG trading with strong aspirations to be the Asian LNG trading hub. It is best positioned to foster cooperation in the LNG sector. At the same time, it could look to its neighbours, to get wider adoption of its LNG index or to gain support for its trading hub position by capitalising on the region's strong LNG demand. We expect ASEAN's LNG demand to triple to 35 mmtpa in 2025, and grow further to 72 mmtpa in 2035. Looking at this robust growth, the region should explore collaborative ways on how to make LNG procurement more competitive.

Thailand has been relatively successful in developing its domestic gas market, with the established Natural Gas Vehicle infrastructure. Malaysia started liberalising its gas market this year, something that other countries in ASEAN are contemplating to do.

On the power sector, despite stronger anti-coal rhetoric, ASEAN continues to invest in coal generation, sanctioning more than 10 GW of new coal capacity last year. With growing environmental concerns, it needs to embrace cleaner forms of generation, fostering cooperation in the renewable front. Philippines is the hot bed for renewable investments at the moment. Together with Philippines, Vietnam has one of the highest wind potentials in Southeast Asia and has aspired to tap this energy.

Indonesia has been the pioneer of island electrification, and is developing small-scale LNG projects across the country. This is something that can be replicated elsewhere in the more remote areas of ASEAN, where access to electricity is still unavailable. The electrification rate in Myanmar for instance, currently stands at 52%, requiring more distributed power generation which is cheaper and has shorter time to delivery.

Against the backdrop of aversion towards conformity, learning from each other's experience seems to be the way to grow for ASEAN.

{kind=link}

{kind=link}