Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

European gas storage plans for 2023 still stand despite cold snap

Reduction in gas demand and increased LNG imports supports a positive outlook for 2023

2 minute read

Colder temperatures across Europe have increased month-on-month heating demand by 20% in December, but behavioural change in households and services means the amount of gas used in these sectors is 16% lower than previous average consumption patterns for similar temperatures says Wood Mackenzie, a Verisk business (Nasdaq:VRSK).

Despite the recent cold weather, Europe is still on track to end this winter with gas storage levels at 38% and looks set to meet the 2023 European Union target of having inventories up to 90% by November next year.

The findings were published in Wood Mackenzie report: Europe Gas & Power Markets Short-Term Outlook Q4 2022.

Penny Leake, Wood Mackenzie research analyst for European gas said: “Gas demand has decreased by 10% in 2022, equivalent to 50 bcm. In 2023, gas demand will continue falling, albeit at a slower rate year-on-year, under normal weather conditions. Demand in the residential sector will reduce by 12% compared to the five-year average, however, it will be similar to levels in 2022 as this was a relatively warm year. Demand in the industrial sector will reduce by an additional 7%. Gas demand in the power sector will fall by 4% as renewable build out continues to grow and despite nuclear and hydro output remaining weak.”.

Leake added “From April to October 2023 there will be up to 25 billion cubic metres (bcm) less Russian gas. But with storage levels reaching 38% at the end of this winter, Europe’s requirement to refill storage levels next summer will fall by 19 bcm compared to the corresponding period of 2022. This, combined with 9 bcm additional liquefied natural gas (LNG) imports, will help hit the 90% gas storage capacity target set by the EU.”

“The EU and UK combined are projected to import 164 bcm of LNG in 2023, a record high, and 13 bcm more than 2022,” said Leake. “This will be supported by accelerated regasification capacity projects that are currently underway and will help Europe’s storage levels refill by next summer.”

Pricing to soften in 2023

Mauro Chavez Rodriguez, Research Director European Gas & LNG markets, added: “Prices will need to remain high to keep demand low and to attract LNG. However, if Europe’s storage levels reach 38% by March as forecasted, there is a downside risk to the current forward curve, which is trading at US$40/million British thermal units (mmbtu). Part of this reduction will also be facilitated by increased regasification capacity in the Netherlands and Germany, helping reduce bottlenecks from gas piped flows from UK to the continent, helping TTF ease to levels closer to NBP and DES LNG prices.”

“Weather remains the biggest risk factor to this view If a colder-than-expected winter hits the northern hemisphere, European demand could increase 13 bcm and Asian LNG demand 7 bcm, potentially taking inventories to just 19% by winter’s end and only 73% ahead of winter 2023/2024, providing upside to the current forward curve.”

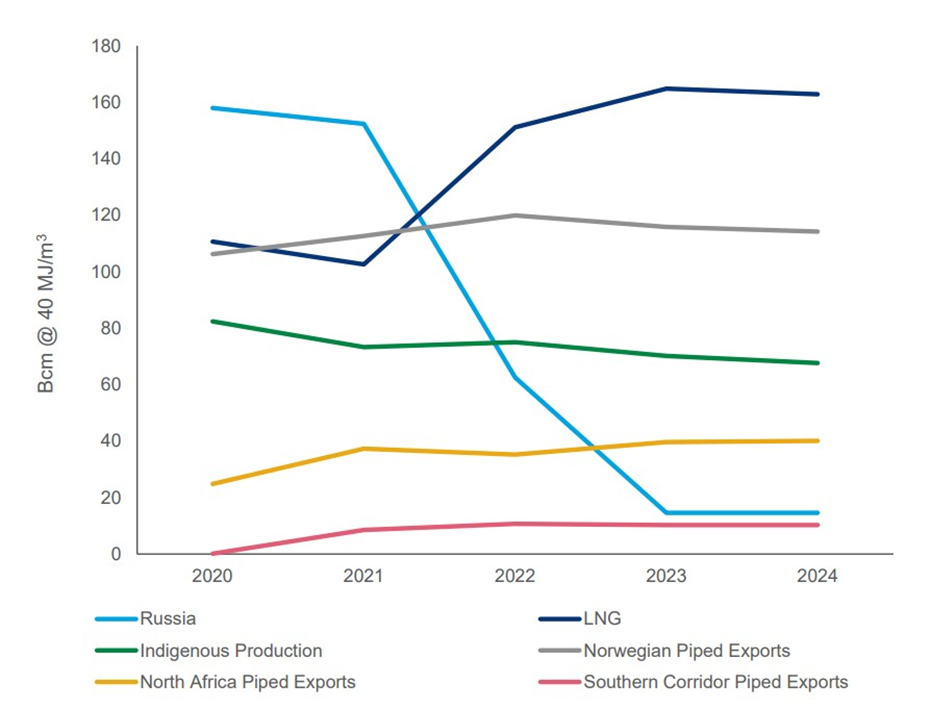

Europe gas supply mix

Source: Wood Mackenzie; *Europe excluding Turkey