Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

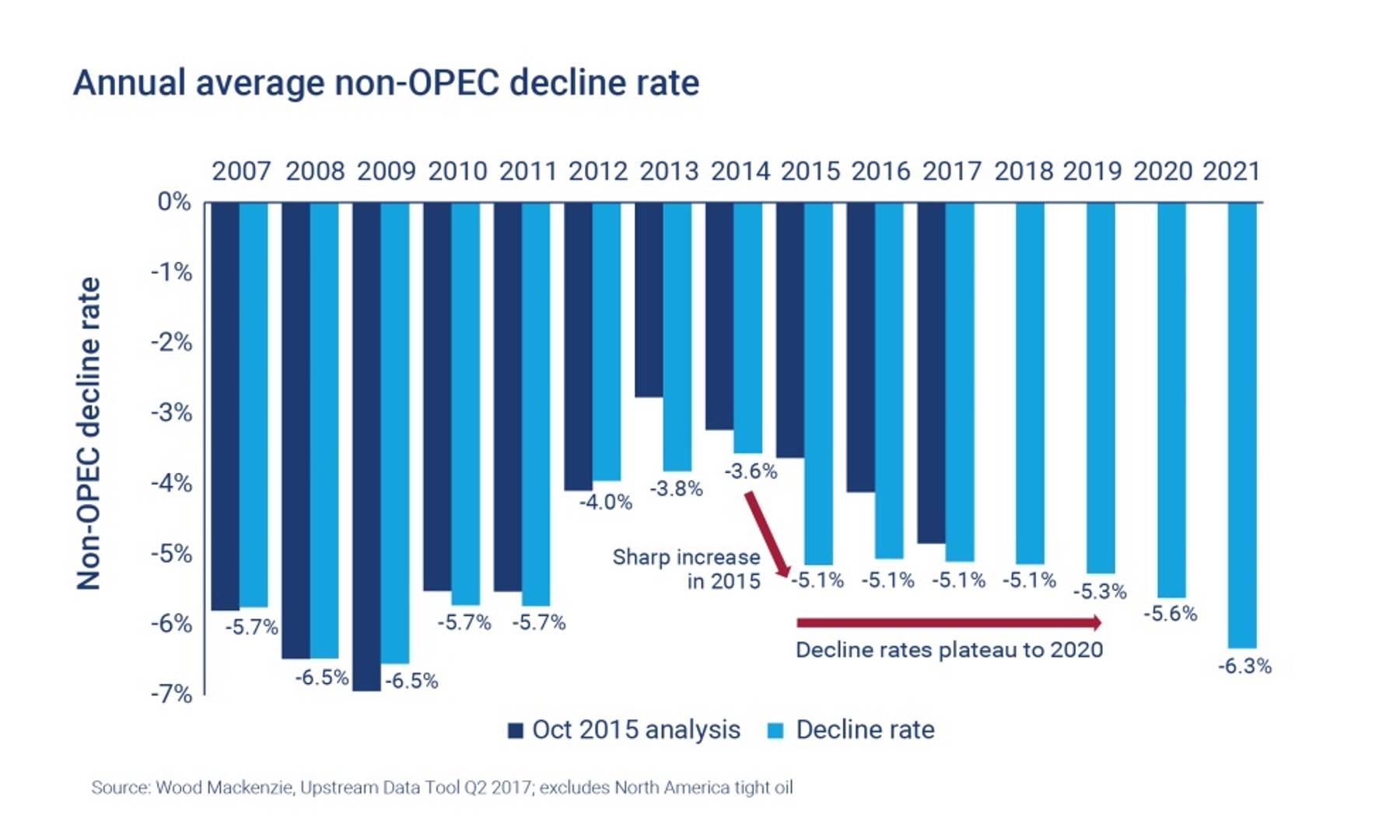

Edinburgh/London/Houston/Singapore - Through operational excellence programmes and smart spending, operators have managed to maximise production and improve efficiencies, bucking expectations of an increase in decline rates. In fact, non-OPEC decline rates have remained stable since 2015. A new report by Wood Mackenzie, Non-OPEC Decline Rates: Lower for Longer, looks at the factors influencing this stability, how long it can be maintained and the impact future shifting decline rates may have on the oil market.

Dr Patrick Gibson, Research Director, Global Oil Supply, at Wood Mackenzie, said: “Decline rates are a critical factor influencing the current rebalancing of the oil market and price recovery. A 50% cut in investment in non-OPEC producing oil fields and a dwindling pipeline of new projects since the price crash should have led to progressively steeper decline rates. Nonetheless, decline rates have held steady at around 5% since 2015 and we expect they will remain at this level until 2020.”

Wood Mackenzie's analysis shows that, annual decline rates for conventional fields peaked at nearly 7% during the last decade, or 2.4 million barrels per day (b/d) a year. However in 2014, they reached an historical low of just 3.6%, or 1.2 million b/d. The price collapse saw decline rates increase to 5.1%, or 1.9 million b/d in 2015, on the back of steep spending cuts. Decline rates have stayed at around that level since.

"Stable rates of non-OPEC decline is a disappointing story for those looking for significant price support coming from declining conventional production," Dr Gibson said.

He said improved operating efficiency and focused capital expenditure (capex) have helped maintain decline rates at current levels. Operators have maximised production rates by focusing on the best-performing wells, as well as targeting processes and maintenance programmes so uptime is increased.

"Careful budgeting is also in play," Dr Gibson added. "Slashed capex now predominantly targets short-cycle opportunities with high returns potential, while development plans and service-sector cost cuts have bolstered spending efficiency."

While some shorter-term measures may relax, longer-term factors, such as increased production from 'zero decline' assets and early-life assets, will help keep decline rates steady. Wood Mackenzie's analysis shows early-life assets increasing their proportion of production from 6% in 2010 to 30% by 2020. The lower decline rates of these assets counter-acts the higher declines of more mature assets.

{kind=link}

{kind=link}

Dr Gibson said: "Canada's oil sands and Brazil's deepwater pre-salt play are adding a growing proportion of production, significant enough to offset global decline rates. The oil sands alone could reduce decline rates by as much as 0.6% in 2020."

Technology will also play a role in maintaining stable decline rates, as evidenced by developments in horizontal drilling, hydraulic fracturing, enhanced oil recovery techniques and CO2 flooding in the US, Canada, and Russia.

Beyond 2020, Wood Mackenzie expects decline rates will return to the historical norm of around 6%, and higher oil prices will be needed to incentivise investment in new production to meet a widening supply gap. Even moderate swings in average annual decline rates are capable of influencing the market; the rate of decline for non-OPEC fields is crucial to the global supply picture. A 1% shift in annual global decline rates would have a significant effect on supply, potentially adding or removing 2 million b/d by 2021.

"Our current modelling shows stable decline rates until 2020, then a widening to 6% in 2021. Although the present picture is one of resilience and smart spending, further gains remain unlikely. With investment so low, the industry is potentially storing up problems for supply that won't become apparent until after the end of the decade."

Corporate week in brief: non-OPEC decline rates – lower for longer?

Corporate week in brief: non-OPEC decline rates – lower for longer?