Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Southeast Asian upstream M&A could hit US$14 billion

Gas in frame with more than 5.4 billion boe potentially up for grabs

1 minute read

According to a new report by Wood Mackenzie, Southeast Asia could take centre stage in the region's upstream M&A activity in 2019, with up to US$14 billion worth of assets potentially switching hands.

Upstream M&A in the Asia-Pacific region is off to a strong start this year, with US$2.8 billion worth of deals already announced in the first quarter of 2019. This includes Murphy Oil's US$2.1 billion divestment of its Malaysia business to Thailand's national oil company (NOC) PTTEP. With the exit, Murphy Oil will focus on its core positions in US Gulf of Mexico, North American onshore and Latin America.

{kind=link}

"We have observed for a while now the trend of oil Majors exiting countries in the region as their portfolios mature and contracts expire. Drawn to more commercially compelling opportunities elsewhere, Southeast Asia is also becoming a non-core region for large- and mid-cap international oil companies (IOCs)," said Wood Mackenzie research director Andrew Harwood.

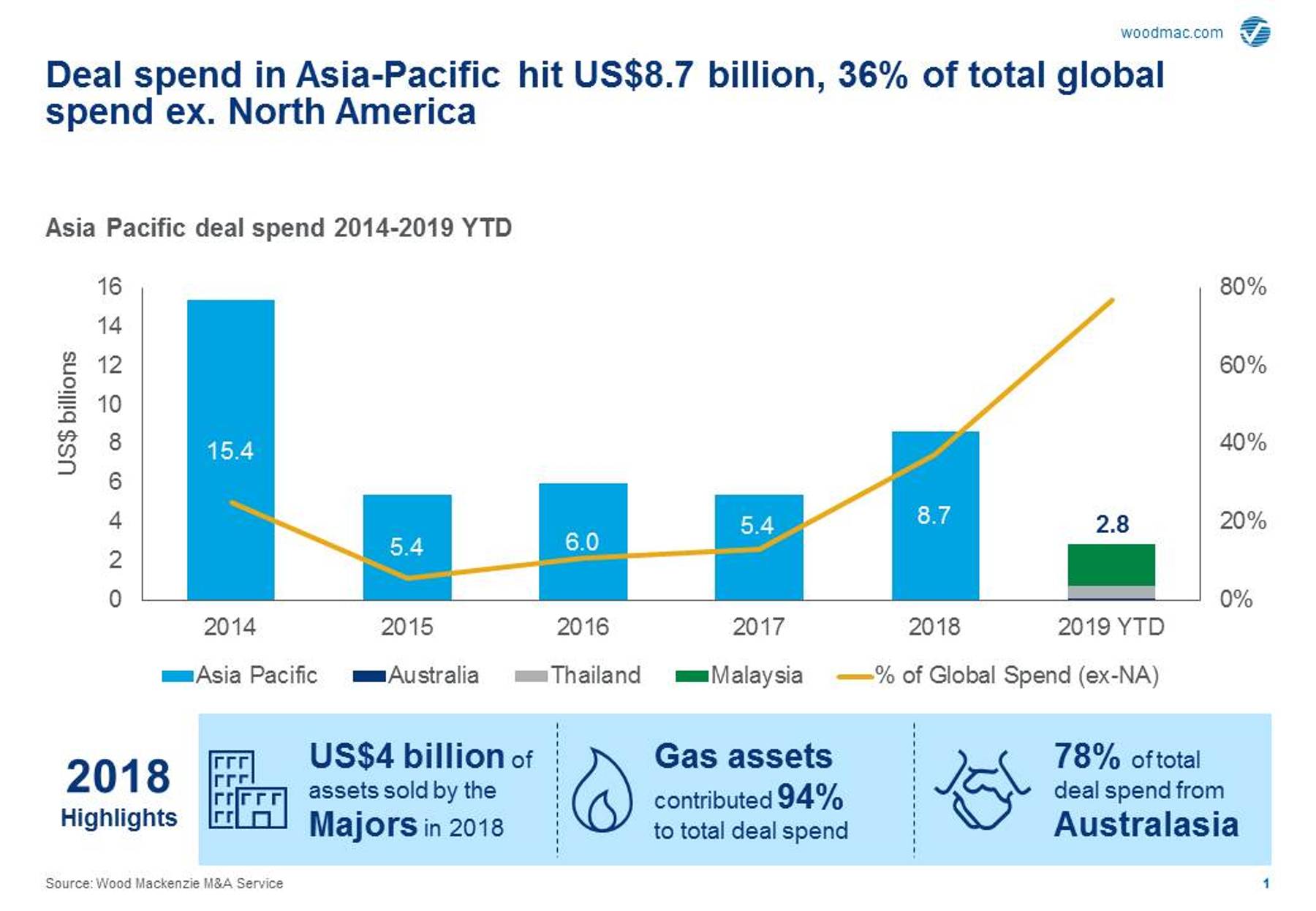

Asia-Pacific upstream deal spend hit US$8.7 billion last year, accounting for over a third of global spend (excluding North America). This increase in activity was primarily driven by a reshuffling of portfolios in Australia and New Zealand. However, Southeast Asia is set to feature more prominently in 2019, with more than 5.4 billion barrels of oil equivalent (boe) of predominantly gas assets potentially coming to market.

Alongside retrenchment by traditional E&P players, 2019 M&A potential will also be driven by regional NOCs farming down assets to bring in technical and financial partners to manage newly-expanded portfolios. In fact, two of the region's biggest portfolio owners, PERTAMINA and PTTEP, must spend a collective US$32 billion over the next five years to maintain their domestic supply outlook.

"Pre-development projects that been stalled during the oil price downturn is also another theme for smaller players and new entrants to take note of. As economic conditions improve, there could be new owners and new capital looking to monetise these assets," added Harwood.

With the region's M&A stakes stacked high, it begs the question: Who are the potential buyers?

Harwood said: "The M&A bear view would be that there is a smaller universe of potential buyers, but we think regional NOCs, Middle Eastern operators and regional specialists, will continue to be active players shoring up assets in Southeast Asia.

"Recent global corporate activity will have a knock-on effect on Southeast Asia portfolios. And changes in the regional investment climate following recent elections, fiscal adjustments and exploration success could spur new activity. The dominoes in Southeast Asia's M&A space have already started to fall."