Sign up today to get the best of our expert insight in your inbox.

Is Argentina’s giant shale play the next Midland Basin?

Crude and LNG exports will help diversify global supply

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Pietro Ferreira

Senior Research Analyst, Upstream

Pietro Ferreira

Senior Research Analyst, Upstream

Senior upstream analyst covering Latin America with deep expertise in asset valuation and regional energy markets.

Latest articles by Pietro

-

Opinion

Where is Latin America's next upstream opportunity?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Ryan Duman

Director, Americas Upstream

Ryan Duman

Director, Americas Upstream

Ryan specialises in supply forecasting, basin characterisation, upstream decarbonisation and economic modeling.

Latest articles by Ryan

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

-

Opinion

How US shale and deepwater are reshaping Major upstream competitiveness

-

Opinion

US shale gas is back: new demand signals underpin upstream opportunity

-

Opinion

US shale gas is back: new demand signals underpin upstream opportunity

-

Opinion

Gas prices enter a bearish spring amid crude market volatility

-

The Edge

Three factors driving US liquids production to new heights

Kristy Kramer

Head of LNG Strategy and Market Development

Kristy Kramer

Head of LNG Strategy and Market Development

Kristy brings over fifteen years of gas and energy industry experience to her role leading our Gas and LNG Consulting.

Latest articles by Kristy

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

-

The Edge

The energy crisis is coming to the boil

-

The Edge

War is once again reshaping gas and LNG

-

Opinion

Five key takeaways from our Gastech 2025 Leadership Roundtables

-

Opinion

US LNG expansion: Balancing growth ambitions with oversupply risks

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

Argentina is on the cusp of a shale revolution. The Vaca Muerta in the Neuquen Basin has proved to be a world-class shale resource, setting the stage for a new era of oil and gas production growth that could last for decades.

A sense that something big is unfolding pervaded my meetings with the main operators in Buenos Aires last month. The parallels with early-stage US unconventionals are unmistakeable – for the Neuquen Basin Argentina 2026, think Midland, Texas 2010.

The timing is perfect as buyers of oil and LNG seek to diversify supply sources away from the Middle East. Pietro Ferreira and Ryan Duman (Upstream) and Kristy Kramer (Gas and LNG) shared six insights on an opportunity that could be transformational for the Argentine economy.

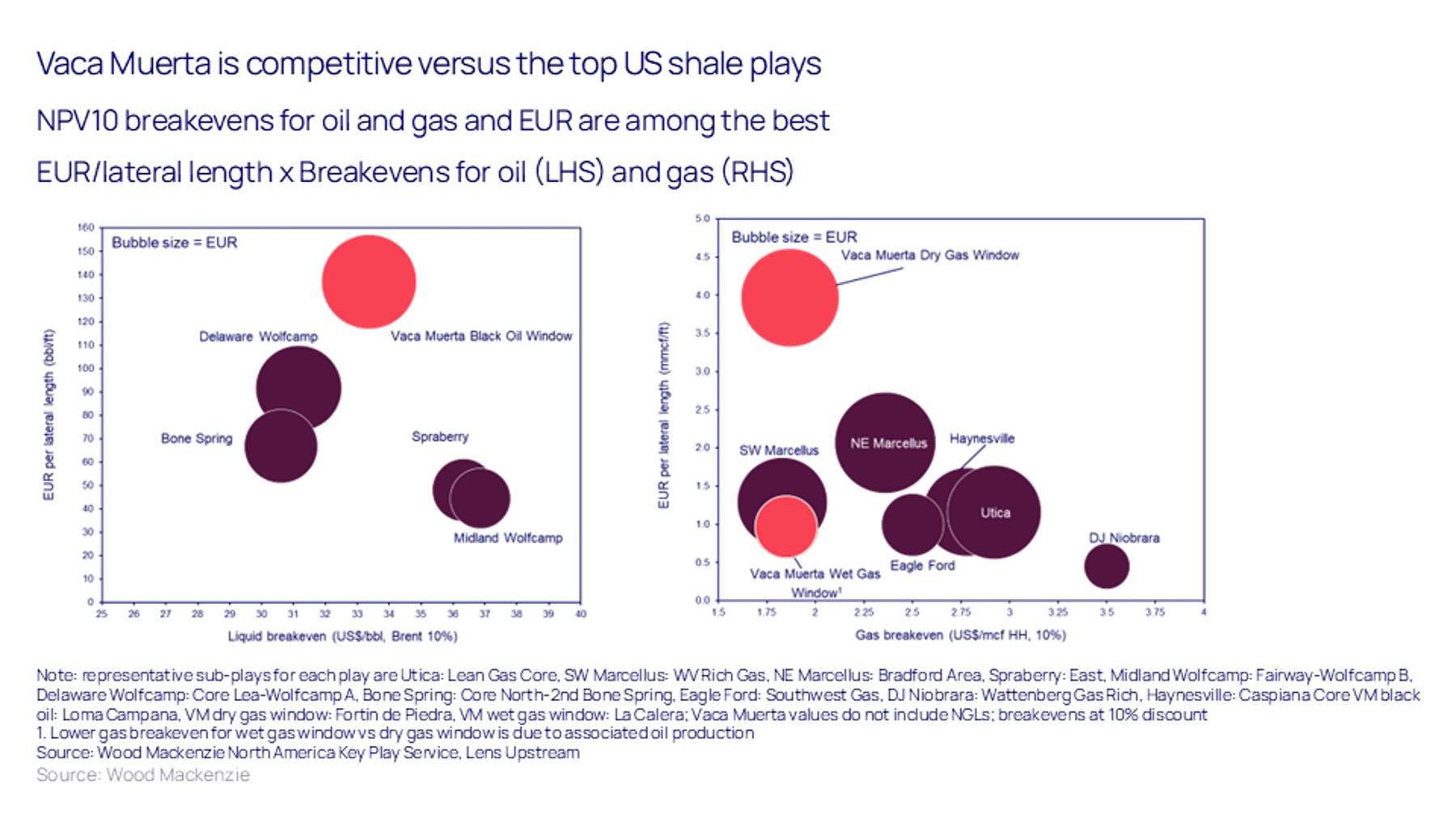

First, the resource is top tier

High-quality rock gives the Vaca Muerta sweet spots high productivity for both oil and dry gas. NPV10 breakevens are similar to the best US plays at around US$35/bbl for the black oil window and under US$2/Mcf for dry and wet gas.

The Vaca Muerta has largely caught up on well performance metrics with comparable US plays, even in these early stages of development. But wells are 50% more expensive to drill and complete than in the US, for a number of reasons – not least, limited service-sector capacity. Lower drilling density and technical challenges – such as high reservoir temperatures, which require specialist equipment – are contributory factors. Strengthening the supply chain is essential to maximise production and minimise costs.

Second, politics and regulation are supportive

The election of President Javier Milei in November 2023 has dovetailed with the technical advances. The government is in the process of establishing a legal framework to alleviate investor concerns.

Its economic motivation is clear – the Vaca Muerta could turn Argentina’s current energy trade deficit into a surplus. The RIGI framework (Incentive Regime for Large Investments), introduced in July 2024, provides tax, currency exchange and customs incentives and is key to attracting investment in capital projects. The current RIGI project pipeline now exceeds US$100 billion, including the new VMOS oil pipeline, LNG developments and shale oil.

Investors are aware that there is political risk in Argentina in the long term.

Third, M&A has taken off, with disclosed deals of US$4 billion since 2023

ExxonMobil, TotalEnergies (partially), Equinor and Petronas have exited while Argentine buyers – including YPF, Pampa, Pluspetrol and Vista – leveraged local capital and international markets to consolidate their exposure. The top five Vaca Muerta producers are all now locally focused.

Chevron is the sole Major and has recently committed to develop its 100% equity shale oil block. Continental’s acquisition of its first operated shale development outside North America highlights the growing attraction of Vaca Muerta to US shale specialists.

Fourth, the upside potential is material

Production today is just under 0.9 million boe/d, easily the largest producing shale play outside North America. Wood Mackenzie forecasts total Vaca Muerta production to climb steadily to over 1.6 million boe/d by 2035. Leading producer and acreage holder YPF is more aggressive, targeting 2030 to double its oil production to 0.8 million b/d and more than double gas to feed LNG exports, which begin from 2027.

Three consortia will drive the infrastructure buildout: nine companies are partnering to evacuate the crude; Southern Energy (Pan American Energy, YPF, Pampa Energia, Harbour Energy and Golar) will invest in the gas evacuation and LNG export operations; as will YPF, Eni and XRG for Argentina LNG. Combined upstream investment will ramp up from US$10 billion spent in 2025 to average US$15 to US$16 billion a year beyond 2030. A further US$5 billion a year will be spent on LNG export infrastructure and related gas pipelines.

Argentina already has a good track record of delivering larger-scale energy infrastructure, including the Perito Moreno gas pipeline (US$2 billion) and Northern Gas Pipeline reversal (US$740 million), both in 2024. The VMOS oil pipeline, at US$2.4 billion, is due to be completed end-2026.

Fifth, Argentina is set to become an LNG exporter, capitalising on buyers’ desire for supply diversity, triggered by the Ukraine and Middle East conflicts

Domestic gas demand is highly seasonal – the country currently imports LNG at winter peaks while curtailing production in the summer. Market reforms and RIGI incentives have helped unlock huge volumes of Vaca Muerta gas for export.

The LNG economics are resilient to low domestic and international prices, thanks to some liquids-rich upstream positions. Southern Energy will develop two projects with total capacity of 6 Mtpa (Phase 1 start-up 2027, Phase 2 in 2028). Argentina LNG targets 12 Mtpa (FID by 2027, start-up early 2030s) with expansion potential to 18 Mtpa. Using floating LNG facilities will reduce in-country execution risk.

Finally, the buzz I encountered in Buenos Aires extends beyond oil and gas

Urea and data centres are in the conversation to monetise cheap gas while some E&Ps are looking to diversify into lithium – indicators of how much is in motion across the economy. If the investment delivers, Vaca Muerta may become Argentina’s Midland.

{kind=link}

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.