Sign up today to get the best of our expert insight in your inbox.

Nigeria’s oil and gas independents come of age

Realising ambitious plans for production growth

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

View Gavin Thompson's full profileNigeria’s independent oil and gas producers are helping to reinvigorate the country’s upstream sector and boost production after years of decline. These companies now contribute 27% of Nigeria’s overall production, a sharp rise from 12% a decade ago.

At Wood Mackenzie’s Nigeria Executive Briefing held in Lagos last month, the mood among the independents was optimistic but tempered by the challenges that lie ahead. Given the country’s lofty oil and gas growth targets, can Nigeria’s indigenous producers step up?

What has driven the growth of Nigeria’s independents?

Right place, right time. Ambitious and entrepreneurial local companies leapt upon a unique set of circumstances, not least the Majors’ divestment of their non-core onshore and shallow-water portfolios. Supportive government policies and a strong domestic skills base – often acquired from the leading international oil companies – have helped underpin growth. With over 100 local players active across its upstream sector, Nigeria boasts Africa’s most diverse corporate landscape.

How important are Nigeria’s independents?

Critical. Structurally lower investment has resulted in Nigeria’s liquids production falling from above 2 million b/d a decade ago to around 1.6 million b/d currently. With the government setting an ambitious 3 million b/d target by 2030, Nigerian companies are playing their part. Local players now contribute more than a quarter of total domestic oil production, bolstered by post-M&A development activity and increased output from marginal fields. Nimbler operating models, higher risk tolerance and close relationships with government and state-owned NNPCL have provided competitive advantages.

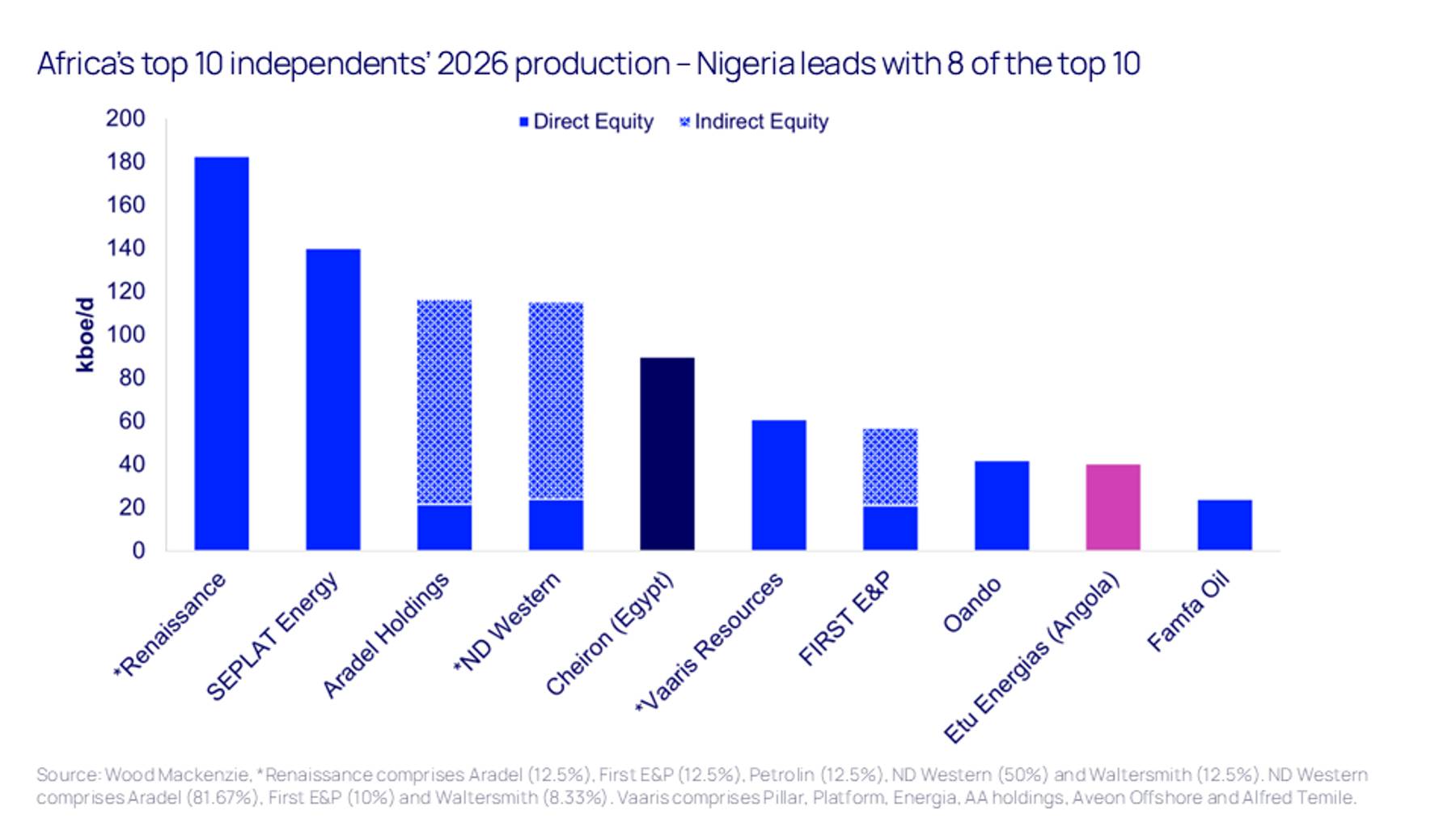

Consequently, Nigeria’s independents now make up eight of the top ten indigenous African producers, with Renaissance Africa Energy and SEPLAT Energy at the top of the pile. With a combined value of US$12 billion, Nigerian companies represent around 75% of the African independents peer group value.

{kind=link}

What are their future growth plans?

Nigeria’s independents don’t lack ambition. Renaissance, SEPLAT and Oando JVs are targeting around US$35 billion of spend on a comprehensive work programme of greenfield and brownfield activities aimed at boosting output. Presidential directives intended to unlock growth in gas development are also offering opportunities for Nigerian independents that hold around one-third of the country’s gas reserves. Continued high grading of the Majors’ portfolios could also deliver more opportunities in onshore and shallow water developments, while M&A activity may evolve to include consolidation within the indigenous peer group.

Beyond M&A, licensing can play its part. Nigeria’s active 2025 licensing round focuses on discovered resource opportunities in the established producing Niger Delta heartlands. The round is set to conclude in Q4, though local companies have raised concerns around data reliability and the marginal nature of available assets.

What could hold back future investment?

Financing remains the major obstacle. Nigerian independents are challenged with financing late-life projects in a high-risk environment without the luxury of large balance sheets. With more than half of Nigeria’s oil production coming from fields that started up before 2000, operating depleted and marginal fields will become increasingly difficult.

Lenders must also consider Nigeria’s high costs and emissions and its less advantaged resources, which provide lower value on a unit basis. Operating costs for Nigerian independents average close to US$15/boe, the highest across Africa. While the county’s diverse corporate landscape has helped reinvigorate the sector, it also brings complexity and risk to operations and project execution.

What more can the government do to boost investment?

Much has already been done. Laws promoting local content, alongside a new regulator to enforce them, have prioritised domestic company participation. The competitive licensing framework, which typically issues smaller block sizes, supports this approach. But more action is needed to reduce risk: increasing facility uptime, accelerating project approvals and ensuring security are key.

Without further improvements, Nigeria risks curbing investment by its independents. Even with significant resources to go after, some are already looking beyond Nigeria for growth. Current high oil prices offer a massive opportunity to increase domestic production with the help of indigenous players. Losing this investment to other markets should not be an option.

Does the independents’ growth mean the Majors are retreating from Nigeria?

No, it’s more a high grading of portfolios. Big Oil’s Nigerian joint venture divestment programmes are nearing completion, with the Renaissance JV seeing TotalEnergies’ sale of its equity interest awaiting completion and Eni’s anticipated exit reportedly in progress.

Once done, the Major’s focus will primarily be on greenfield deepwater oil and gas supply projects into the Nigeria LNG facility. Shell’s announcement of the development of its deepwater Bonga North project in late 2024 was Nigeria’s first deepwater final investment decision in more than a decade. That is likely a taste of things to come. Backed by supportive fiscal policies, Bonga South West Aparo (Shell-operated), Usan West and Owowo West (ExxonMobil-operated), Etan Zabazaba (Eni-operated) and the shallow-water Ima Gas Field (TotalEnergies 40% participation) are expected to follow.

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.

Sign up today using the form at the top of the page.