Get Ed Crooks' Energy Pulse in your inbox every week

Middle East conflict adds a new dimension to hydrogen strategies

Energy security concerns strengthen demand for alternative supply sources, but government support will be essential

1 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is the competitive power market model broken?

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

When enthusiasm for low-carbon hydrogen was surging in 2021-2023, you would sometimes hear it described as the Swiss Army knife of energy, useful for power generation, transport, domestic and industrial heat, and more. Today, a more appropriate metaphor might be that hydrogen is seen as a jack-of-all-trades, but master of none. For many of the proposed uses of hydrogen, there are alternatives that are cleaner or cheaper, or both.

The conflict in the Middle East has changed the terms of that debate. The prospect of long-term threats to energy exports from the Gulf region, even after the current crisis has been resolved, has revived interest in hydrogen as an alternative to hydrocarbons.

Before the Iran war, about 20% of the world’s LNG, 25% of the internationally traded ammonia and 37% of the urea was exported through the Strait of Hormuz. The slump in traffic through the strait sent prices for LNG, urea and ammonia soaring in markets around the world. And although some of those prices have subsequently fallen back, many remain well above pre-war levels.

In conversations around hydrogen today, there is much more emphasis on its role in reinforcing energy security than on its impact on greenhouse gas emissions. Hydrogen can be an alternative to oil and gas, whether used directly or converted into other fuels and feedstocks, including ammonia and methanol.

There are also critical sectors, including refining and fertilisers, which currently rely on hydrogen produced from natural gas. If competitively priced alternative sources were available, that would be a significant benefit for those sectors.

The Trump administration has comprehensively rejected the idea of using government policy to tackle climate change. But last month, Brooke Rollins, the US agriculture secretary, celebrated the progress made at the world’s largest low-carbon ammonia project, at CF Industries’ Blue Point complex in Louisiana.

Secretary Rollins said the project was progressing at “Trump speed”, after the administration expedited the award of the permits it needs.

The project will produce blue ammonia, made from natural gas with the carbon dioxide emissions captured and sequestered. So its commercial viability is based on abundant US natural gas supply, not on bypassing the hydrocarbon supply chain. But it will contribute to the development of a global low-carbon ammonia sector that, over time, will include more electrolytic hydrogen.

Meanwhile, China has set the development of an electrolytic green hydrogen industry as one of its strategic priorities for energy. The 15th Five-Year Plan, published in March, identified hydrogen as one of the “key areas that will lead future development”, alongside technologies such as nuclear fusion and brain-computer interfaces.

China holds more than half of the world’s green hydrogen production capacity that has reached a final investment decision. The Envision Chifeng project in Inner Mongolia is the world’s largest, and lowest-cost, green hydrogen and ammonia plant.

Other economies, including the EU and India, have been pressing ahead with developing their hydrogen industries, despite technical and economic challenges. In January, India-based green hydrogen developer AM Green and European energy company Uniper signed the world’s largest green ammonia offtake deal.

Last year, the EU’s third Renewable Energy Directive (RED lll) set demanding targets for green hydrogen use, and is expected to have a significant impact on Europe’s industry.

Low-carbon hydrogen is still an expensive option. The critical questions are whether higher prices are worth paying as insurance against the risk of further disruption to global supplies of hydrocarbons, and how far the cost of that insurance can be brought down to acceptable levels.

The Wood Mackenzie view

Last week, Wood Mackenzie held its annual Hydrogen Conference, with energy security a key theme of the discussions, both on stage and in the corridors.

Murray Douglas, our head of hydrogen research, presented data that showed how the Middle East conflict had changed some of the calculations around the low-carbon hydrogen supply chains in Europe.

The cost of producing conventional grey ammonia depends on the price of natural gas, which has soared in international markets since February. At current short-term prices for European benchmark TTF gas, roughly US$17 per million British thermal units, grey ammonia will cost about US$800 per ton to produce.

Meanwhile, the delivered cost of low-carbon ammonia in Europe will be in a range of US$700 to US$1,100 per ton, Wood Mackenzie estimates. So the lowest-cost low-carbon projects could be competitive on price with conventional ammonia.

There are some important qualifications to those calculations. The low-carbon projects are mostly not online yet, so they cannot make any contribution to easing the impact of the crisis. When the conflict is over and the Strait of Hormuz reopens, allowing LNG from Qatar and the UAE to reach world markets, European gas prices are expected to drop sharply, making low-carbon ammonia uncompetitive again.

But the comparisons do indicate how hydrogen could help support energy security and resilience in Europe by diversifying its supply chains.

In the longer term, the economics of low-carbon hydrogen and its derivatives will be strongly influenced by the cost of carbon in the EU, as well as the price of natural gas. If China establishes itself as the lowest-cost producer of green hydrogen in world markets, the EU will also face some tough decisions about whether using it to replace hydrocarbons is simply exchanging one vulnerability for another.

Resolving these questions will be up to governments. Wood Mackenzie projects that costs for low-carbon hydrogen will fall significantly over time as the industry scales up. But it is unlikely to be competitive with hydrocarbons on an unsubsidised basis for a long time to come.

As Wood Mackenzie’s Douglas puts it: “For the next 15 to 20 years, at least, low-carbon hydrogen is likely to continue to rely on government support.”

Attacks continue in the Middle East

Hostilities between Israel and Iran flared up over the weekend, casting doubt on an imminent peace agreement in the Middle East. On Sunday, Iran fired ballistic missiles at Israel, following Israeli strikes on Beirut, and warned of wider attacks on US-linked targets across the region.

The situation remains confused, with both the US and Iran expressing willingness to agree a peace deal. President Donald Trump posted on his Truth Social network that both Iran and Israel were seeking an immediate ceasefire. He said final negotiations on a peace agreement were proceeding, “subject to ignorance or stupidity getting in its way”.

In the meantime, a few vessels, including tankers, have been passing through the Strait of Hormuz, often while switching off their automated identification system beacons. Still, the number of transits has remained well below its pre-war levels.

Wood Mackenzie VesselTracker data showed a modest pickup in ship traffic through the strait last week. But with only about 30 transits on the most active day, it hardly compares to 170 or so on a typical day before the war.

In an illustration of the hazards still facing vessels in the region, the UK Maritime Trade Operations Centre reported on Monday a fire onboard a tanker off the coast of Oman. The crew was evacuated from the ship.

Other views

Ten takeaways from WoodMac’s LNG Conference – Simon Flowers and others

Global upstream update: handpicked for small and mid-sized E&Ps – Fraser McKay

Safety officials finally have a good idea of what a big rocket explosion can do – Stephen Clark

Quote of the week

“People are really saying… ‘My company spent my entire 2026 budget in Q1. Can you make this more efficient?’ We are continuing to push on that more with models. I think we’ll have a lot of ways we can help people get more value for less spend. But that went from, at the beginning of this year, an issue that never came up – people were totally happy with the amount that they were spending – to, all of a sudden, a huge issue.”

Sam Altman, chief executive of the AI pioneer OpenAI, said in a corporate interview that concerns about costs and value for money were now one of the main issues raised by the company’s customers.

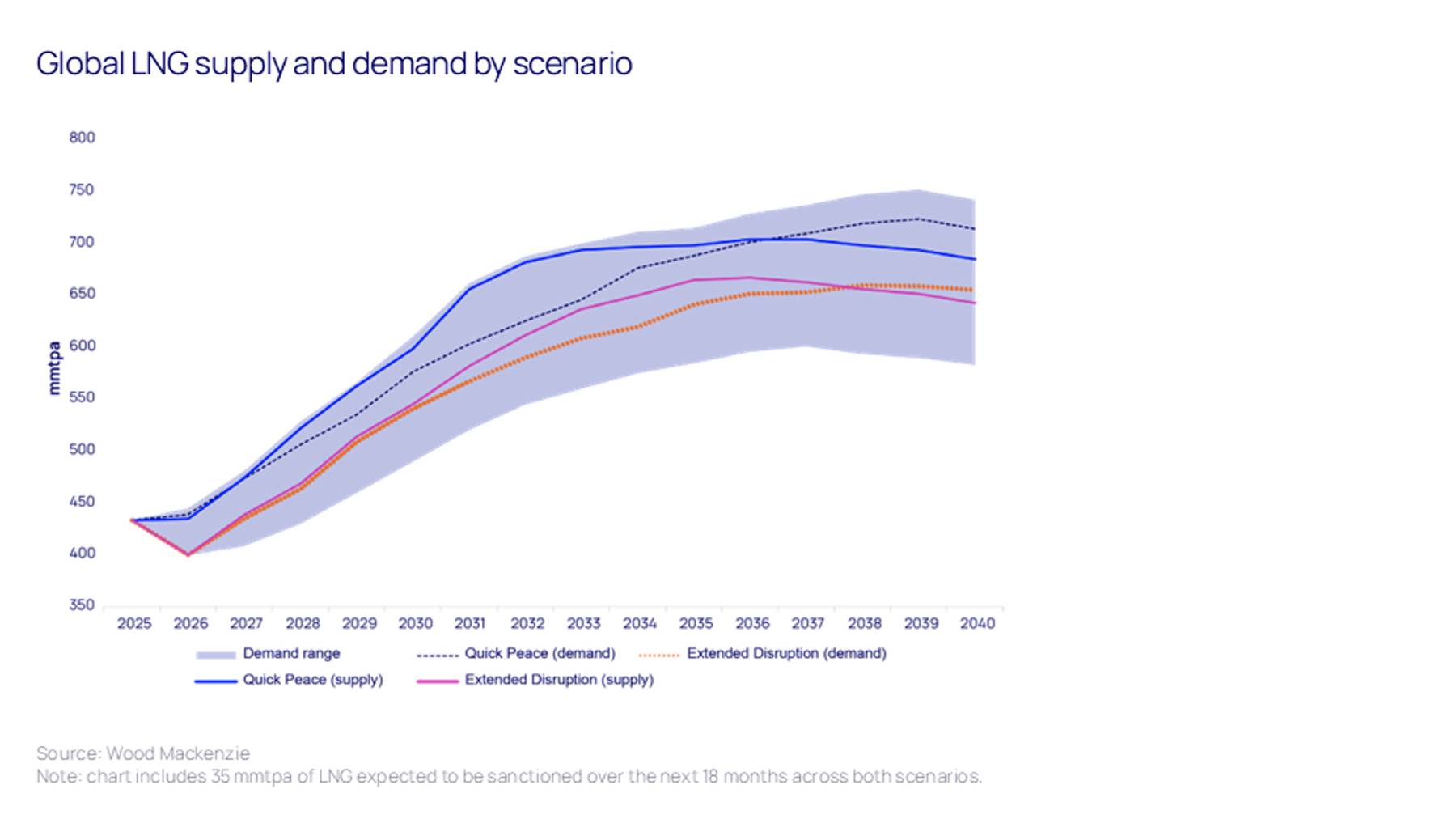

Chart of the week

In the previous Energy Pulse, I showed Wood Mackenzie’s projections for global economic growth in our three scenarios for the outcome of the Iran war. This chart shows potential outcomes specifically for the LNG industry. The lines show central projections for global LNG supply and demand in the two main cases: Quick Peace, which reflects a reopening of the Strait of Hormuz within a few weeks, and Extended Disruption, which assumes a conflict continuing until the end of the year.

Before the war, Wood Macenzie was projecting an excess supply of LNG on world markets by the late 2020s. Even in the Extended Disruption case, that oversupply still arrives eventually, but its emergence is pushed back about three years, from 2028 to 2031.

However, that oversupply is not inevitable. The shaded blue area indicates uncertainty over the outlook for demand, which grows over time. Wood Mackenzie analysts predict “a market driven by geopolitical risk, periods of extreme price volatility and lower supply and demand”.

Read the full Horizons report for more details of the scenarios’ implications for oil, gas and power.

{kind=link}

Get The Inside Track

Ed Crooks’ Energy Pulse is featured in our weekly newsletter, the Inside Track, alongside more news and views from our global energy and natural resources experts. Sign up today via the form at the top of the page to ensure you don’t miss a thing.