Strait talking: Iran war scenarios and the future of energy

May 2026

May 2026

Author(s):

Massimo Di Odoardo

Vice President, Gas and LNG Research

Massimo brings extensive knowledge of the entire gas industry value chain to his role leading gas and LNG consulting.

Latest articles by Massimo

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

LNG: why a resilient portfolio is increasingly key to success

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

The Edge

How power markets can adapt to energy crises

-

The Edge

Ceasefire in the Middle East

Alan Gelder

SVP Refining, Chemicals & Oil Markets

Alan is responsible for formulating our research outlook and cross-sector perspectives on the global downstream sector.

Latest articles by Alan

-

The Edge

Oil and gas markets’ perilous dilemma

-

Opinion

The Hormuz shock: what the data reveals about global oil markets in 2026

-

The Edge

Has the oil price bubble burst?

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

UAE’s exit rattles OPEC’s grip on the oil market

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

Peter Martin

Vice President, Head of Economics

Peter is responsible for our global economic outlook to 2060.

Latest articles by Peter

-

The Edge

Will falling populations reshape energy demand?

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

Opinion

Investing for the long term: quantifying the economic costs of an accelerated energy transition

-

Opinion

European gas: 6 Q&As on prices, supply, and regulatory impact

-

Featured

Metals & mining 2026 outlook

-

Opinion

Tariffs, trade and technology: the macro forces shaping metals markets

The fragile ceasefire between the US and Iran has brought some respite to the Middle East from intense military conflict. A durable peace agreement is proving elusive, however, and a prolonged closure of the Strait of Hormuz is now the greatest single risk to both energy markets and the global economy.

More than 11 million b/d of Gulf crude and condensate production is curtailed right now due to the closure of the strait. Meanwhile, gas consumers around the world have lost access to over 80 Mtpa of LNG, equal to 20% of global supply.

The longer the Strait remains closed, the higher oil, gas and electricity prices will rise – and the greater the impact on energy demand and the global economy. Even once a peace agreement is reached, regional tensions are likely to persist, risking further damage to Gulf supply and intermittent disruption to the transit of oil, liquefied natural gas (LNG) and other commodities into the global market.

Uncertain times compel consideration of divergent outcomes. Wood Mackenzie has developed three distinct scenarios that assume differing timelines for the end of the war and, crucially, the reopening of the Strait of Hormuz. Here, we analyse the impact of these scenarios on oil and gas supply, demand and prices, and consider the wider implications for energy markets and the global economy.

Three scenarios for reopening the Strait of Hormuz

Quick Peace scenario

This is the most optimistic outcome and is aligned with our recently published Strategic Planning Outlook base case for oil and gas/LNG. The Quick Peace scenario assumes a workable peace agreement is achievable in the near term, leading to the Strait of Hormuz reopening by June, with minimal restrictions on transit. The global economy bounces back swiftly, returning broadly to our pre-war trajectory by Q4 2026.

Summer Settlement scenario

The current ceasefire holds, but a peace agreement takes longer, with no settlement until late summer 2026, and the Strait of Hormuz remains largely closed to traffic until September. There is an extended impact on oil and LNG supply, resulting in shortages of crude and products through Q3, leading to higher near-term prices and a shallow global recession in H2 2026.

Extended Disruption scenario

The Extended Disruption scenario assumes slower progress towards a peace agreement, with persistent tensions flaring into short-term conflicts. The Strait of Hormuz remains closed through the end of 2026, leading to a deeper global recession and economic scarring as shortages of key commodities and high prices erode demand and force tough policy decisions for import-dependent countries. Further damage to existing production facilities and infrastructure lengthens the recovery time of exports back to pre-war levels, and transit through the Strait remains at risk of sporadic disruption beyond 2026.

The risks surrounding the scenarios are asymmetrical. The lack of concrete progress on resolving the underlying issues behind the war so far casts considerable doubt on a Quick Peace outcome. Similarly, the far-reaching impact of the Extended Disruption scenario we present here is just one of many potential outcomes of a prolonged conflict and disruption to energy exports through the Strait of Hormuz. Yet, the dire consequences of that Extended Disruption scenario, which go well beyond energy and include future food availability and social cohesion, underline the necessity for all sides to urgently embrace a pragmatic approach to achieving a resolution.

Oil

Scenario snapshot:

- Quick Peace: oil market tight through Q2 2026, returning to over-supply in 2027

- Summer Settlement: risks to over-supply in 2027 reduced by slower recovery in transit flows

- Extended Disruption: global oil market reshaped by push for greater energy security, lowering long-term oil demand and prices

Quick Peace scenario: transit flows through the Strait of Hormuz begin to normalise within weeks. Upstream supply from the region’s strongest producers could be restored quickly, but operators are likely to prioritise stored volumes for export in the early stages. Countries with less storage capacity and mature, heavy or complex assets – particularly Iraq – face a longer, tougher recovery pathway. The oil market remains tight through the summer, before prices weaken in Q4 2026 to US$80/bbl for Dated Brent by year end.

Despite oil demand growth recovering and depleted inventories being refilled, the oil market returns to US$65/bbl through 2027, strengthening to around US$70/bbl in the early 2030s before demand peaks in 2032.

Summer Settlement scenario: prices continue to increase throughout summer 2026 and remain higher in 2027 than under the Quick Peace scenario. The timing and pace of production recovery are slowed and inventories are drawn further. Oversupply in the Quick Peace scenario is damped as inventory refill counters weaker demand recovery. The spillover consequences for subsequent years remain modest, as oil price escalation is of limited duration, assuming no further major infrastructural damage.

Extended Disruption scenario: global inventories of oil and refined products continue to deplete through 2026. Further OECD stock releases calm fears of major shortages, but provide only temporary relief as the supply shock becomes global. Demand for refined products (gasoline and jet) falls sharply in response to rising prices. Meanwhile, industrial production declines as the global economy tips towards a deep recession, with the Asian petrochemical sector struggling to source feedstock. In H2 2026, oil demand falls by 6%, but inventory depletion continues to send oil prices towards US$200/bbl by year end.

Global oil demand continues to fall through H1 2027, despite the re-opening of the Strait of Hormuz as the global economy shrinks, bottoming out by mid-year. Weak demand prompts a sharp drop in oil and refined product prices, despite the months-long lag before tanker readiness and transit flows normalise and an even longer gap before crude production fully recovers. Shut-in Gulf production reaches over 70% of pre-conflict levels before summer 2027. However, full production restoration requires repairs and intensive intervention, and outages last beyond the end of the year.

Then comes the reassertion of fundamentals. Global supply growth outpaces demand growth in H1 2028, and high levels of inventory rebuild cannot prevent prices falling below pre-conflict levels to around US$50/bbl. Assuming no voluntary OPEC/OPEC+ cuts, the weak pricing environment persists through 2029, as demand only returns to pre-conflict levels towards the end of that year.

The long-term outlook is for a structurally weaker oil price than our pre-conflict assessment should importing countries intensify efforts to reduce their oil dependence. If oil-importing countries choose to aggressively pursue faster electrification, as much as half of their forecast oil imports might be displaced. This would exacerbate downward pressure on oil prices, with Brent tracking towards US$60/bbl in 2050, rather than our base-case outlook of around US$75/bbl in real terms. The projected competitiveness of oil underlines the comparative cost challenge for importing countries committed to weaning themselves off oil.

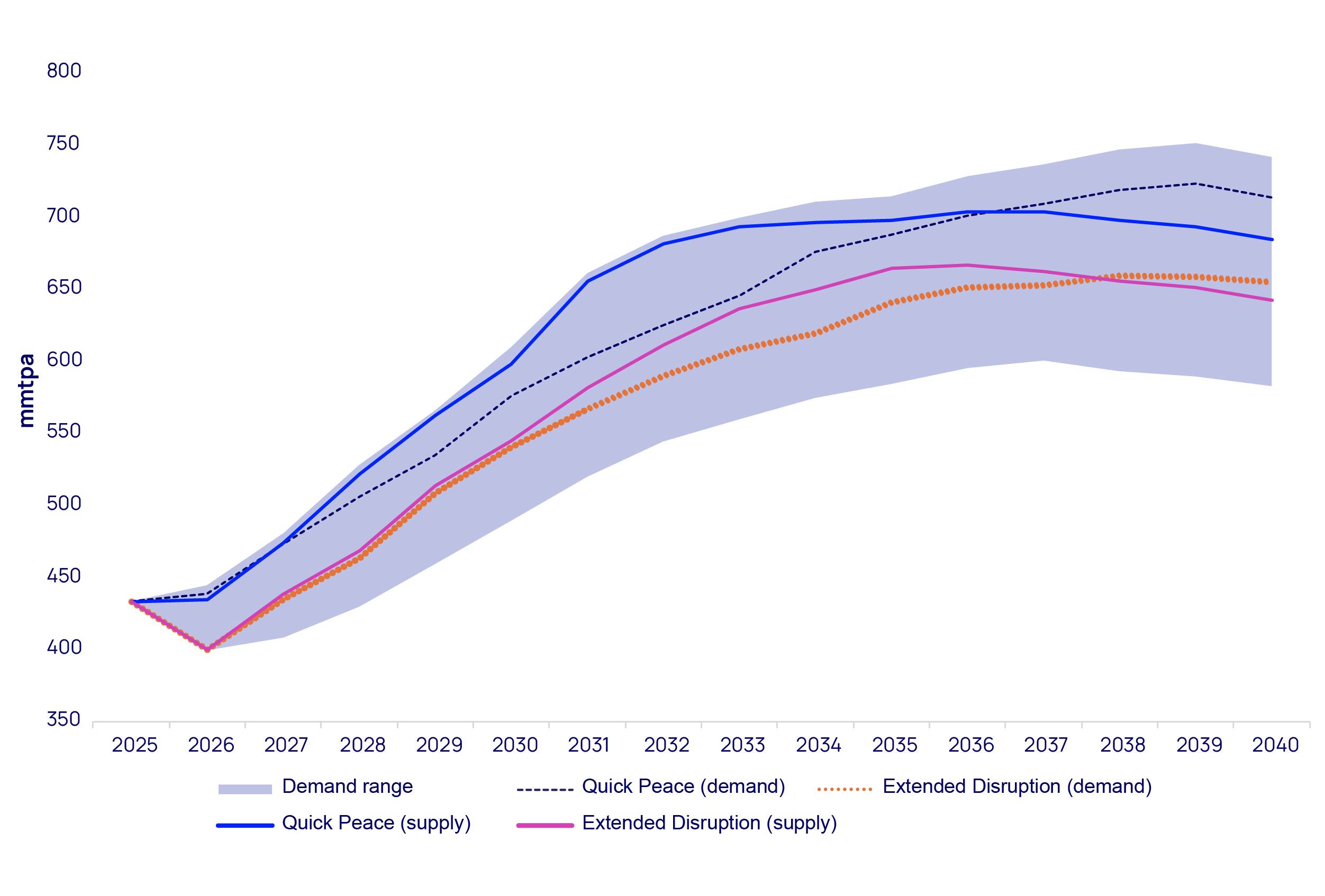

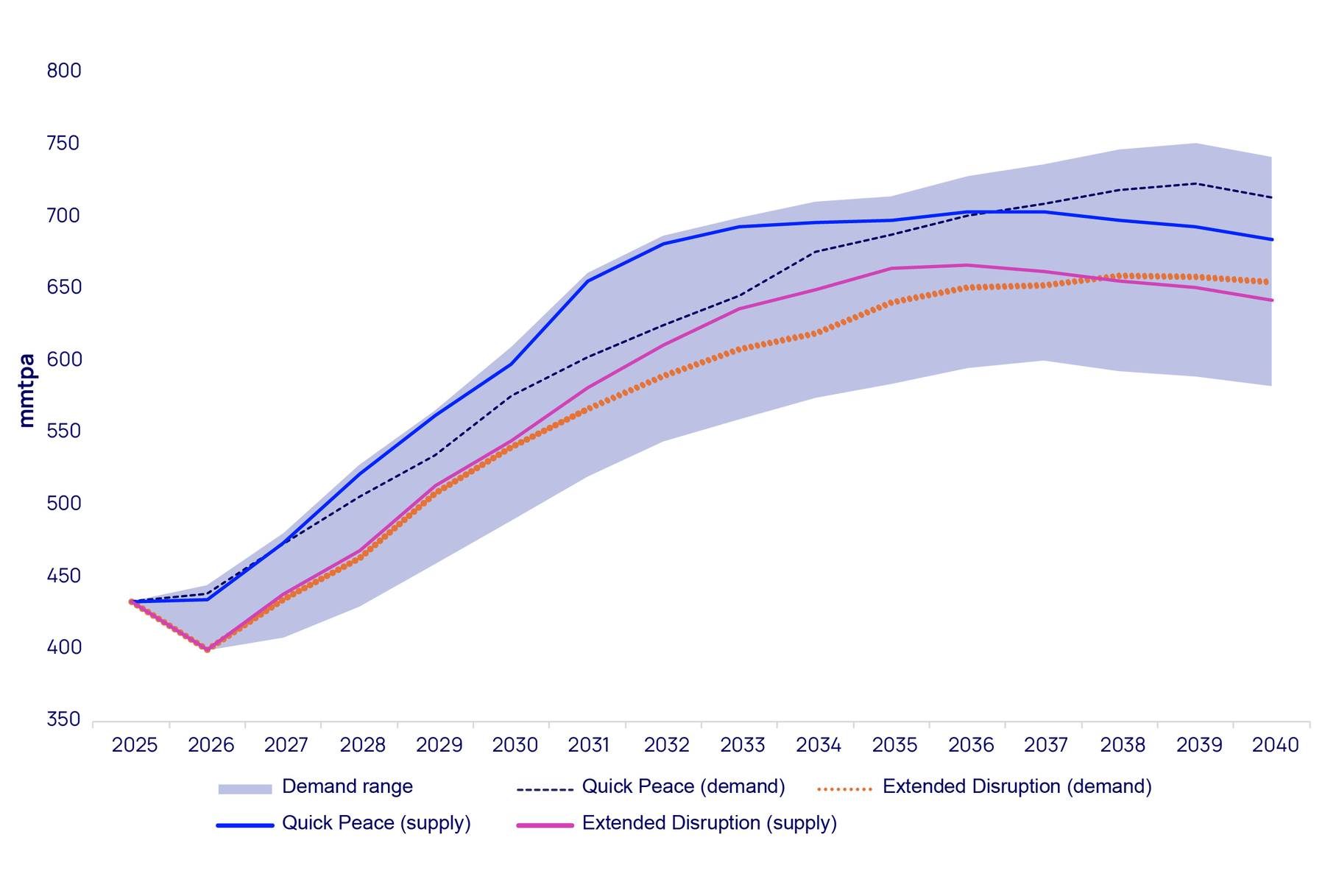

LNG

Scenario snapshot:

- Quick Peace: global LNG market tight through Q3 2027, supply growth outpaces demand from 2028

- Summer Settlement: new Gulf projects delayed, but oversupply only stalled until 2029

- Extended Disruption: global LNG market fundamentally reshaped — lower supply, demand destruction and volatile prices

Quick Peace scenario: LNG prices soften soon after a peace deal is announced, but global LNG markets are tight until summer 2027. LNG supply from undamaged Gulf facilities take time to return to full capacity, with delays to projects currently under construction in the region. The anticipated oversupply, albeit delayed until 2028, remains inevitable once the strait reopens from June, however.

With a major expansion in global LNG capacity under construction, supply is set to increase by about 50% from current levels, restoring confidence in LNG and driving a new phase of demand growth in emerging Asian markets. However, the combined impact of short-term demand destruction and levels of new supply results in a market imbalance. US LNG cargo cancellations are likely to be required to balance the market, more than halving European prices by 2031. Prices then recover slightly between 2030 and 2035.

Summer Settlement scenario: prices continue to increase through summer 2026 and remain strong well into 2027. Additional delays to Gulf projects under construction reduce supply further, but this only pushes the oversupply into 2029. As countries look to reduce their exposure to LNG, demand downside risk cannot be ruled out, potentially exacerbating the oversupply after 2030.

Extended Disruption scenario: the global LNG market is fundamentally reshaped. Prices skyrocket, potentially reaching US$40/mmbtu if the conflict restarts. Persistent geopolitical risks and sporadic Strait closures could reshape the LNG market in the long term.

Future export levels in this scenario are inherently uncertain. The longer the conflict lasts, the greater the risk to future Gulf LNG supply. Unlike liquids, where producers such as Saudi Arabia have alternative export routes and will likely build more, gas will be much harder to reroute.

Some of the region’s existing supply could be permanently lost. The 60 mmtpa of capacity under construction experiences multi-year delays, while Qatar’s North Field West project – approved earlier this year – could be postponed indefinitely.

Gas and LNG demand will also be lower as demand destruction follows a prolonged closure of the Strait and takes time to recover. Persisting Gulf LNG supply risks push more countries to diversify away from imported gas and LNG, while higher LNG prices limit emerging Asian markets’ appetite to develop new gas-fired plants, providing more momentum for renewables and coal. Europe could further accelerate the electrification of heating and suitable industrial processes and build even more solar and wind capacity.

What emerges is a market driven by geopolitical risk, periods of extreme price volatility and lower supply and demand. Prices spike during periods of increased tensions between the US and Iran, then fall as LNG supply from the Gulf resumes. In this scenario, LNG prices average US$14/mmbtu in Europe from 2027 to 2030, with Asian LNG prices trading at a significant premium. With more LNG supply outside the Gulf likely to be sanctioned and demand growth slowing post-2030 as greater energy diversification emerges, prices remain subdued for an extended period. As with oil, any future risk to transit through the Strait of Hormuz could still quickly spark a return to market tightness and volatility.

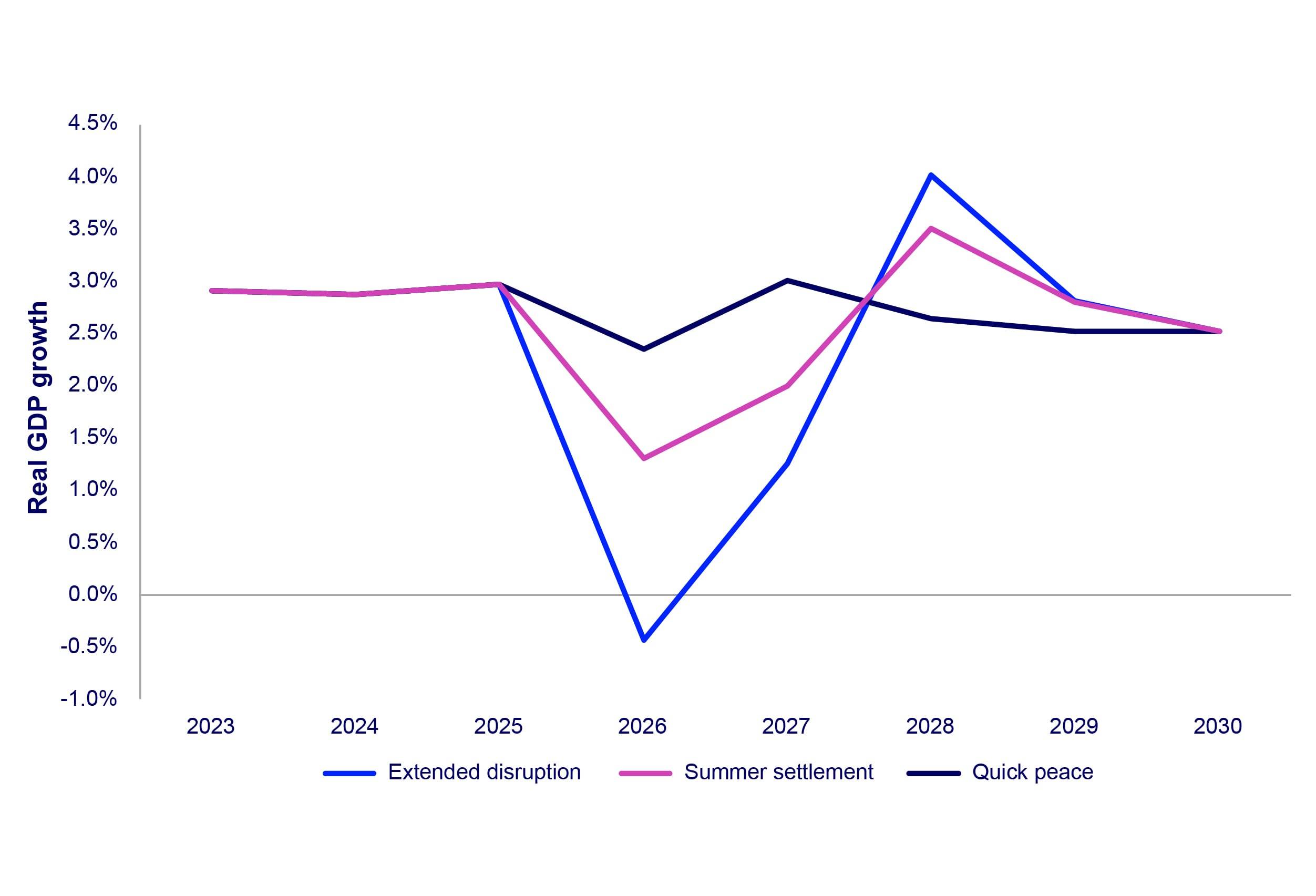

Global growth at risk: three scenarios

The Quick Peace scenario limits the war’s economic impact. Even so, global gross domestic product (GDP) growth slows in 2026. Only the Middle East enters a recession due to the conflict. Global GDP is back to pre-war levels by 2030 and there is no long-term damage to global growth prospects.

Our Summer Settlement scenario sees the Middle East suffer an exacerbated contraction. Elsewhere, short technical recessions in key economies lead to a shallow downturn. Modest economic scarring occurs in the short term, but the global economy’s long-term growth potential is unaffected.

The Extended Disruption scenario delivers the global economy its greatest energy supply shock of the past 100 years, resulting in a deep recession in 2026. This would mark the third global recession this century, though it would be less destructive than the 2008 financial crisis or the Covid-19 pandemic.

The economic impact of the Extended Disruption scenario is asymmetrical, however. The Middle East suffers the largest shock in GDP terms, while significant energy supply shortages suppress Asian economic activity to levels that the available energy can support. In Europe, energy prices stoke inflation, while high public debt and deficits constrain policy response options. Domestic energy resources provide a buffer for the US and China, but not immunity.

The global recovery starts in the second half of 2027 under the Extended Disruption scenario, followed by an above-trend surge in GDP growth in 2028 and 2029. Nevertheless, the crisis results in significant economic pain.

A changed world: how the crisis could reshape the energy order

The war in the Middle East is challenging the existing geopolitical and energy order. Should major economies take decisive – and expensive – action to reduce their import dependency, the consequences of the Iran war could be profound for energy markets.

{kind=link}

{kind=link}

{kind=link}

New era of energy price volatility

Whatever the timing of the reopening of the Strait of Hormuz, resuming energy exports from the Gulf is unlikely to be smooth sailing. Iran has demonstrated its ability to deny free passage through the Strait at its choosing, posing an obvious and ongoing risk to future exports of oil and LNG through the Gulf even after a peace agreement is reached.

This could lead to a divergence between market fundamentals and the perceived risk to oil and LNG supply. Traded prices for both commodities are forecast to fall sharply once the Strait reopens and over-supply emerges. But any threat, let alone actual closure, of the Strait of Hormuz by Iran risks spiking energy prices and ushering in a new period of price volatility.

- Traders and LNG portfolio players: increased price volatility plays to the strengths of the world’s largest trading companies and LNG portfolio players. Trading becomes imperative for all large oil and gas companies.

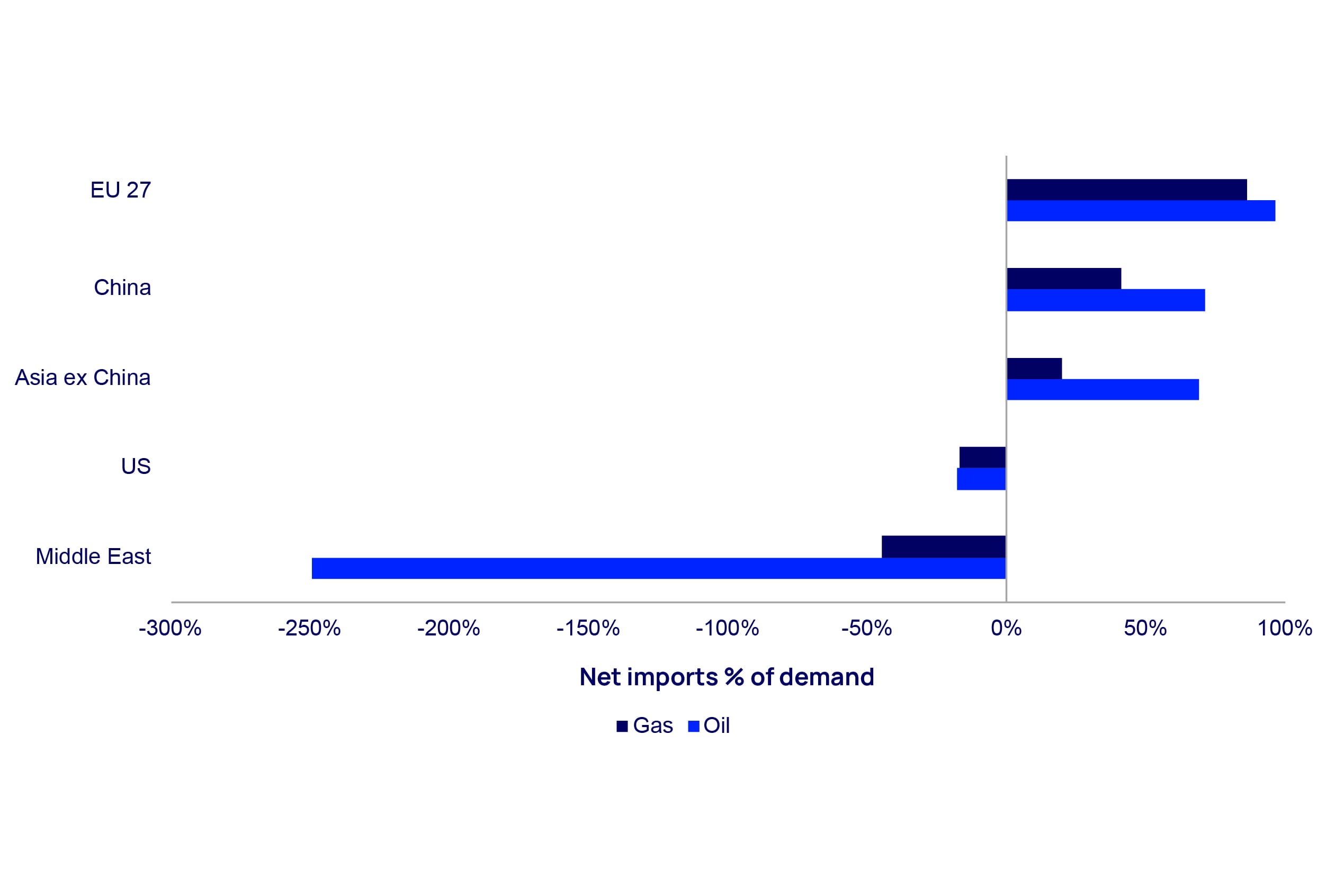

Pursuit of energy independence

The war in Iran is not only eroding long-established international alliances but, in our Extended Disruption scenario, it also encourages a radical policy pivot by import-dependent countries – including most of Europe and Asia – to push for energy independence. Such a pivot is only one possible outcome, however, and would come with its own trade-offs, not least costs and the reliability of supply through any change.

- Power generation: Import-dependent economies across Europe and Asia could invest in a quicker transition. However, the ability to meaningfully reduce their reliance on gas for power generation only starts after 2030 as coal retirements are deferred and renewables, storage and grid modernisation expand. The energy mix diversifies further after 2040 as nuclear power scales up rapidly.

- Supply chains: with its low-cost cleantech advantage, China benefits from a pivot towards energy independence. But relying on Chinese low-carbon energy value chains risks replacing dependence on energy imports with dependence on China. Elsewhere, regions including the Middle East and North Africa that are developing supply-chain hubs for clean technologies are facing conflict-related challenges. The war has already resulted in delays and cancellations of more than 30 GW of planned solar module factories in these markets, while battery storage shipments for the year have been revised down by 25%.

- Miners: the value of supply chains for critical minerals increases as renewables, battery storage and electric vehicles (EVs) grow faster than in our base case. However, miners are largely unprepared to deliver the critical metals required to meet this surge in demand, which would require higher prices.

Molecules versus electrons

One path towards energy independence for importers is aggressive electrification. Delivering this, though, requires deep pockets to accelerate the shift to an economy powered by electrons and away from a dependence on imported oil and gas molecules.

- Energy importers: energy costs rise as countries prioritise security over efficiency. Domestic supply, redundant infrastructure and nuclear deployment all carry price premiums. It proves politically challenging to deliver as oil and gas prices fall.

- Resource holders: resource-rich countries seek to maximise hydrocarbon production. The US continues to pursue energy dominance through oil and gas, while developing economies with oil and gas resources incentivise investment to lower costs and maintain competitiveness.

Climate and emissions

Aggressive electrification for energy security creates a near-term emissions penalty. Coal-to-gas switching reverses in power and industry, and deferred plant retirements keep more coal capacity online for longer. Further out, the emissions picture grows more nuanced as hydrocarbon demand falls and nuclear and renewable capacity increases.

- Global efforts on emissions: already on life support, global agreements to tackle emissions are deprioritised as coal-fired generation expands to boost energy security.

A reshaped global energy landscape

The war raises potentially significant risks for oil and LNG demand beyond 2030. Governments and producers have a range of options in response.

- Gulf oil and gas producers: the region will remain a critical source of oil and gas for the foreseeable future. Producing countries will seek to mitigate risks to future supply. Developing infrastructure for oil exports to bypass the Strait of Hormuz and investment in storage closer to demand centres will increase energy security and prove lower cost than aggressive energy independence for importers.

- International oil and gas companies’ Middle East strategies: as other basins mature, including the Permian, the Middle East will remain increasingly crucial to the strategies of the Majors and larger Independents. Alternative egress routes would support investment.

- Oil and gas producers outside the Gulf: low-cost producers in stable regions could expand output. LNG producers will look to capitalise on buyer interest in supply diversification.

- Refiners in oil-importing countries: refiners face a tougher market outlook as long-term oil demand weakens in import-dependent markets.

- Cleantech manufacturers: as electrification accelerates, renewable and nuclear manufacturers and electric vehicle (EV), battery and charging infrastructure producers stand to gain. But rapid electrification requires massive investment in grid development, with major cost implications.

Liked this article? Join the debate

On our Horizons Live webinar this month's report authors discussed the key findings, latest developments and tackled questions in an insightful Q&A session. Missed it?

Explore our latest thinking in Horizons

Loading...

For details on how your data is used and stored, see our Privacy Notice.

Why sign-up?

By submitting your details you’ll gain access to the latest Horizons report, part of a thought-leadership series exploring the themes shaping the energy natural resources landscape. You’ll also receive the Inside Track, our weekly newsletter, so you won’t miss out on future editions.