Sign up today to get the best of our expert insight in your inbox.

Building an energy superpower

How India fuels its future growth

4 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

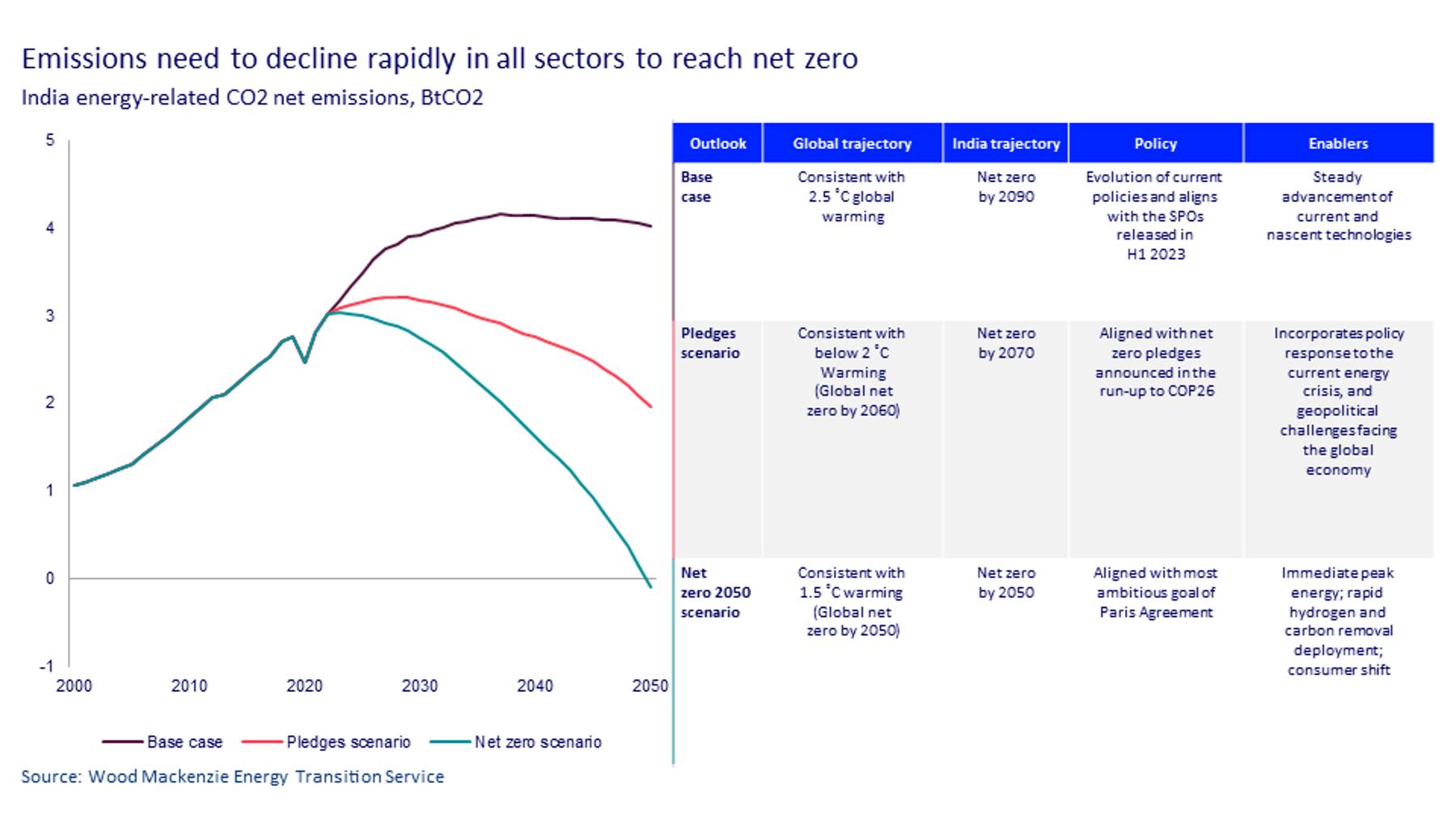

India’s star continues to rise. The fastest-growing major economy today, it will boast the world’s third largest by 2032. But with a fossil fuel-dominated energy system, India is already the third-largest emitter of greenhouse gases.

Last week, I again had the honour of joining Prime Minister Narendra Modi to discuss his country’s energy future at India Energy Week (IEW) in Goa. With India’s need for ever more energy, the prime minister’s vision combines a commitment to increasing domestic oil and gas output with huge investment in developing low-carbon technologies.

The big question posed in our recent Horizons is: can India’s economic growth be achieved without a massive increase in carbon emissions? After participating at IEW, here are our thoughts.

Oil and gas are still essential to meet energy demand

The stark reality is that India’s super-charged economy will continue to rely on hydrocarbons for the foreseeable future. We forecast oil demand will increase by a third, to almost 7.3 million b/d by 2034. Indeed, India becomes the primary engine of global demand growth as China’s oil consumption peaks this decade. India also aims to increase the share of natural gas in its energy mix to 15% by 2030, from 6% today.

In 2022, the government opened up vast areas of deepwater acreage previously closed to explorers. The licensing round came with enhanced fiscal terms, including some of the most competitive in the world for deepwater gas.

Frontier explorers have yet to bite – no new exploration contracts have been signed. The stumbling block isn’t subsurface, but above-ground risk. In recent years, countries making ad-hoc fiscal changes – such as introducing windfall taxes – have experienced much-reduced investment. More than ever, fiscal stability is the foundation for high-cost/high-risk upstream investment. Resolving investors’ doubts is critical to open the flow of capital.

Petronet deal revives LNG ambitions

PM Modi has spoken of his desire to build a ‘gas-based economy,’ but India’s notoriously price-sensitive buyers ran for the hills when prices spiked in 2022. The recent fall in global prices is whetting the appetite among buyers, and we expect demand to double to 39 mmtpa by 2030. The 20-year extension of the Petronet LNG and QatarEnergy LNG contract, signed at IEW last week, demonstrates buyer/seller realignment and is the largest-ever LNG SPA. Lower-cost gas will allow gas-fired power plants to run at higher load factors, displacing higher carbon-intensive coal plant.

Renewables moving in the right direction

India already has the fourth-biggest installed renewable capacity, with wind, solar and hydro accounting for around 43% of the country’s total generation capacity.

Maintaining the rapid renewables roll-out is paramount for India’s electrification. The government’s ambitious Panchamrit initiative seeks to triple non-fossil-fuel capacity in just six years. That’s a huge task, equivalent to adding all of Europe’s current solar and wind capacity. In tandem, India must develop low-cost domestic supply chains for utility-scale solar and wind power, off-grid and decentralised renewables, and energy storage.

Commercialising uniquely Indian opportunities

India has massive potential in green hydrogen, biofuels and energy efficiency, but realising commercial applications will take huge investment and the right government incentives.

In the past year, the government has shown its intent, implementing the National Green Hydrogen Mission, cementing its position as a global leader in compressed biofuels and launching the Global Biofuel Alliance.

With excellent conditions for renewable power, we estimate India’s levelised cost of hydrogen can fall to US$4.3/kg H2 by 2030, the second lowest in Asia, behind China. As an incentive, the government has allocated US$2.1 billion to help reduce electrolytic hydrogen production costs. But to achieve its 5 Mt green hydrogen production target by 2030, India will have to build an additional 125 GW of renewables – on a par with the country’s current wind and solar capacity.

Approval for sustainable aviation fuel production this year will be a big step forward for India’s biofuels sector. But building modern biofuel production to scale will require major federal funding and expansion of the domestic biomass supply chain. India is also striving to increase energy efficiency, introducing the world’s largest zero-subsidy LED bulb initiative – the type of national policy with local impact at which it excels.

CCUS, industrial decarbonisation still lagging

India’s government must go further in other sectors critical to its low-carbon future. Identifying 600 gigatonnes of CCUS potential acknowledges the market opportunity, but India lacks a defined timeline and financial support. The upcoming carbon pricing regime will help, but more incentives are imperative.

India’s ambition to rapidly increase manufacturing output must come with a clearer focus on low-carbon energy supply and feedstocks for a burgeoning industrial sector. Failure to do so risks exacerbating the emissions profile.

India’s prize

We are under no illusions as to how difficult the task ahead will be: sustaining rampant economic growth supported in large part by oil and gas for years to come, while simultaneously building out a low-carbon energy system. The prize, though, won’t just be India’s contribution to global net zero, important as that is, but greater energy independence, new industries and jobs for the coming generations, and affordable energy for its people.

{kind=link}

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.