Will oil companies start spending again?

Cash generation could hit record levels in 2021

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

This could be the year oil and gas roars back. Tom Ellacott, SVP Corporate Analysis, saw in early December that the industry could have its own V-shaped recovery from a calamitous 2020, and generate record free cash flow. I asked how it’s shaping up and whether companies will fall back into old habits and start spending again.

Why is the outlook suddenly upbeat?

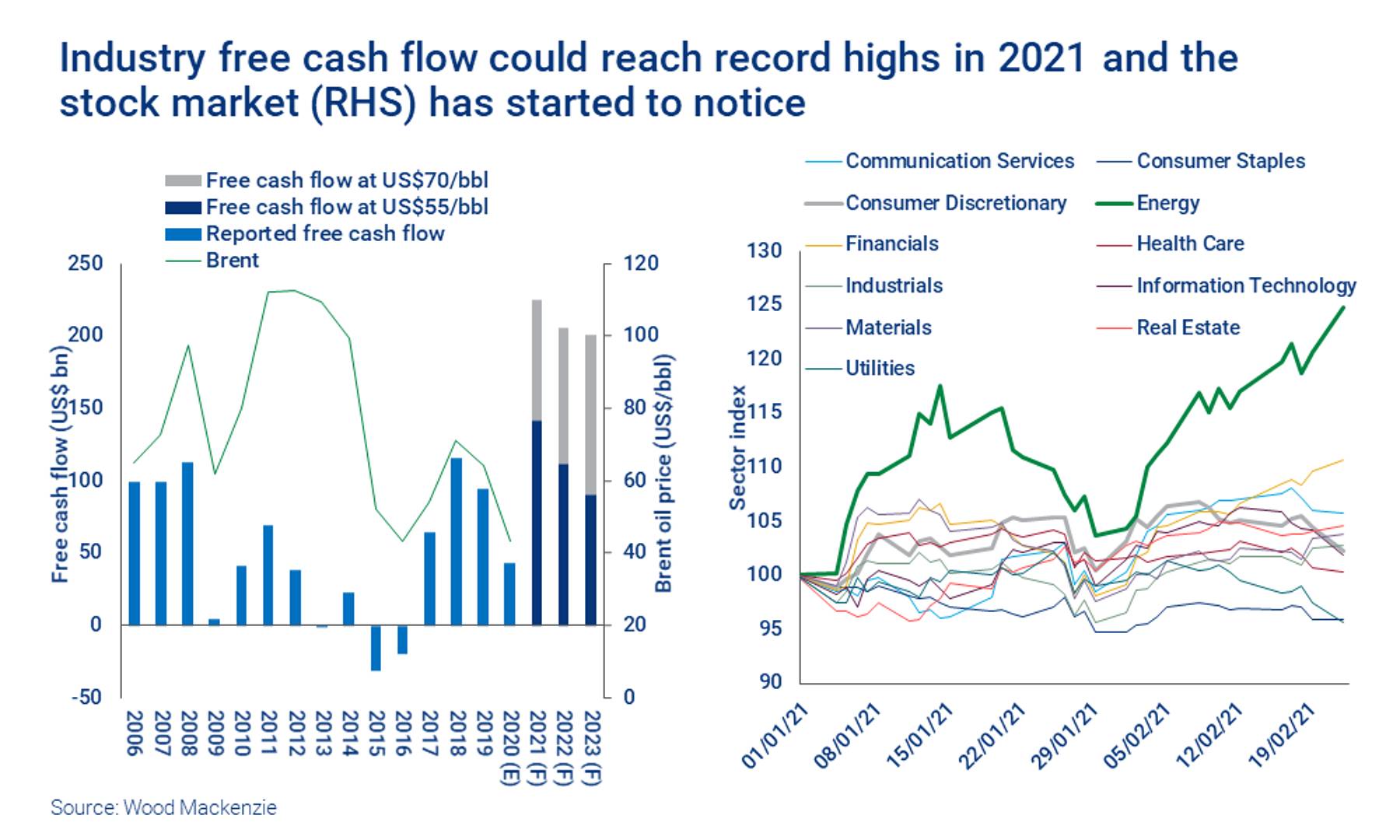

The industry primed itself for recovery, acting fast and hard in the crisis of 2020 to reset the cost base. By cutting distributions to shareholders, investment and operating costs, IOCs reduced the Brent price needed for cash flow to break even from US$54/bbl a year ago to US$38/bbl in 2021. Companies can now cope with low prices; but are also highly leveraged to the oil price recovery that’s underway. There’s a juicy cash flow margin at today’s Brent price of over US$65/bbl, and pure upstream players with undiluted leverage to higher oil and gas prices should benefit most.

How much free cash flow?

Potentially a lot; how much depends on the oil price. At an average price of US$55/bbl Brent, the 40 Majors and Independents in our analysis will generate US$140 billion of free cash flow in 2021 before dividends, buy-backs and interest. And at US$70/bbl, it’s over US$200 billion. Both would be the highest this century, even beating what was achieved in years when Brent averaged over US$100/bbl a decade ago.

Any signs yet?

Companies are understandably cautious in the face of last year’s poor results. The oil price recovered through Q4, but Brent still only averaged US$44/bbl – upstream earnings were no great shakes. Cash flow numbers for the Majors were also held back in Q4 by ultra-weak refining margins. Write-downs added to headline losses for many companies as they drew a line under the year from hell.

We think a fall below US$55/bbl is unlikely this year with the global economy recovering and oil market fundamentals continuing to improve.

What could go wrong?

The biggest risk is the oil price falling back and the effect on upstream. But we think a fall below US$55/bbl is unlikely this year with the global economy recovering and oil market fundamentals continuing to improve. The rest of the value chain could be a drag for integrated companies. Refining is still suffering from chronic overcapacity and low margins will persist for some time yet. With mobility restricted, retail sales are still well below normal.

What will companies do with the extra cash?

Oil and gas companies are recidivists, quick to start investing in growth at the first glimmer of oil price recovery in any cyclical upturn. But this upcycle is different, in that the industry grasps why investors have been disenchanted. Companies are keenly aware they need to prove that they can deliver on returns and cash generation to win back investors’ confidence.

Most will use any spare cash flow after dividends to pay down debt and bolster financial resilience. Leverage blew out to 44% at the end of Q3 (excluding operating leases) from just 15% a decade ago and will be higher still at Q4 (some companies have yet to report). It’ll take over three years of organic cash flow at US$55/bbl to get leverage down to 20%, what we’d argue is a comfortable level, sooner at US$70/bbl.

A few companies are in a better financial position. Shell, Chevron, Pioneer, ConocoPhillips and EOG are among those that start 2021 with stronger finances and so have more options besides deleveraging.

Will investment increase?

We think most companies are determined to hold the line on E&P capital discipline for a time. We’ll have to wait to see how long. Latest company forecasts indicate planned spend for 2021 is 3.5% up on the lows of 2020, but still 28% (or US$53 billion) below pre-crisis levels.

There has been a modest pick-up in drilling activity in the price-sensitive US Lower 48 tight oil plays. But we won’t see a return to the boom years when the sector was spending way over cash flow. US independents are limiting spend to 70% to 80% of operating cash flow, and some even lower.

Buy-backs will make a comeback. Once debt is under control, we think many companies will look to reinforce their commitment to capital discipline and return cash to shareholders.

Will new energy attract more capital?

An upstream cash cow looks ideal for accelerating the development of a new energy business. But here, too, we expect companies to be circumspect. Management is trying to build credibility in the low-carbon value chain. As they have found in oil and gas, overspending and under-delivering on returns is the sure-fire way to lose investor support.

Will low investment in oil and gas lead to a supply shortfall

Yes – we think the world may be sleepwalking into a supply crunch in a few years’ time. It’s a new thing for IOCs to have access to cash but lack the appetite to invest. The longer investment stays low, the higher the probability we’ll see Brent above US$70/bbl in the next few years.

{kind=link}