Find out how our Consulting team can help you and your organisation

Why upstream operators must accelerate cost reduction measures

It’s time for the rapier as well as the broadsword – and better visibility of third party spend may be vital

1 minute read

The markets are still reeling from collapse of the oil price, and the uncertain impact of the coronavirus outbreak. What is already clear though is that all operators all have one thing in common: costs need to be cut and cash preserved. The starkest number is from analysis by our Corporate Team, indicating that spending needs to be reduced by 41% year-on-year for companies to be cash flow neutral at US$35/bbl.

As a recent Insight from our Upstream Research team shows, the first item for the chop has been discretionary investment. FIDs of new projects will be extremely rare in 2020, exploration will be slashed and maintenance on existing assets will be deferred where safe.

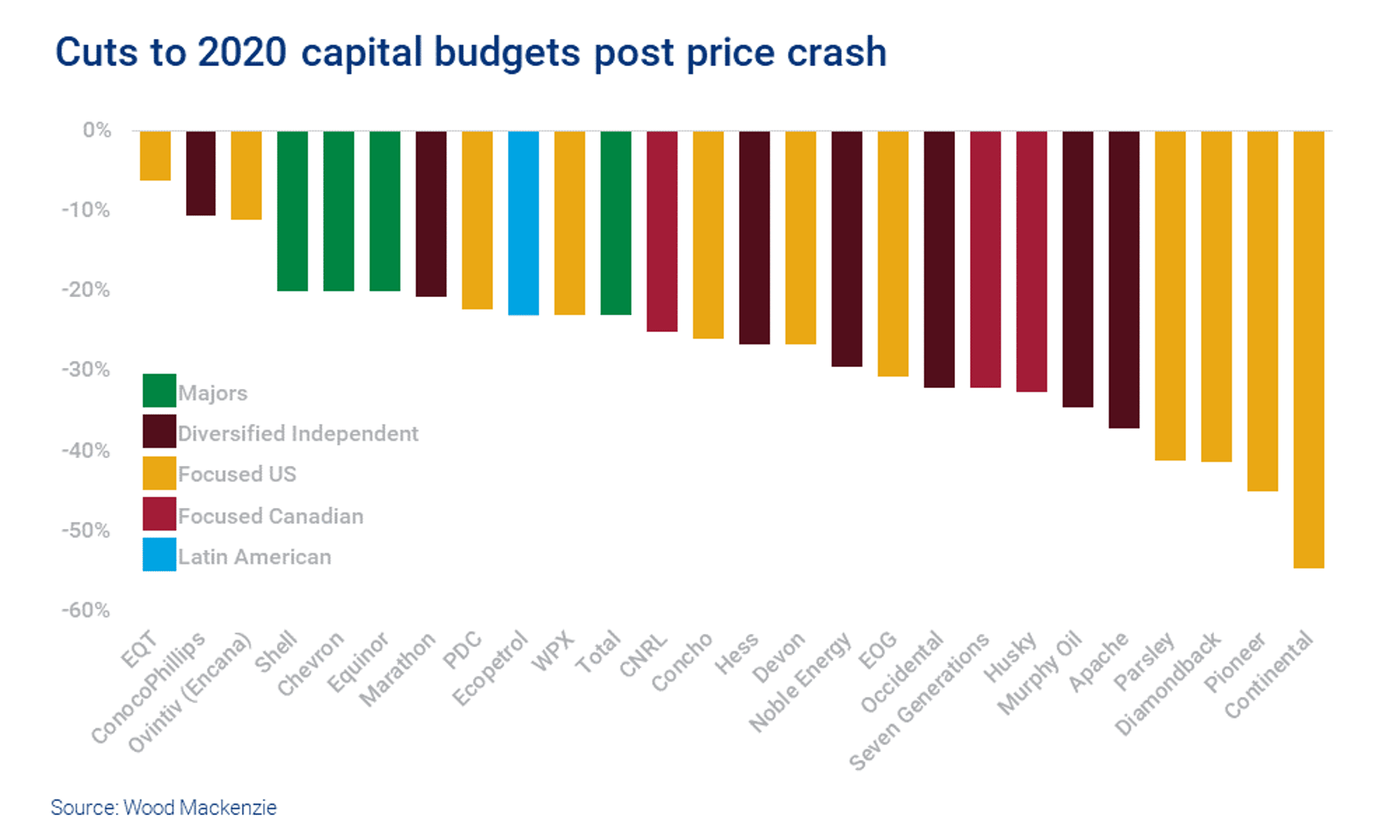

We are continuously tracking spending announcements by operators. As of 26 March, 24 operators have cut budgets by over 30%, with the deepest announced cuts coming from US tight oil players. Pioneer, for example, have cut their 2020 capex budget by 45%. The better financially positioned Majors have also been wielding the knife: Chevron, Shell and Equinor both recently cut their 2020 capex by 20%.

{kind=link}

We now estimate total global upstream development capex spend in 2020 to be 25% lower than originally forecast – a reduction of ~US$130 billion from ~US$490 billion to ~US$360 billion. This can only be a preliminary estimate and will be updated as more operators revise their spending guidance.

This will not be enough.

There is an urgent need to act on the cost base and we are already seeing efforts to push through priced-downs. Some operators have already issued targets to suppliers to reduce prices by 10-25%. This response is understandable but our experience is that there are a number of limitations on what this type of approach delivers:

- Suppliers often have multiple contracts, rate cards, product specifications and supply points providing opportunities to make headline concessions

- Discipline around preferred suppliers and catalogue items is often weak

- Many operators have less visibility on their actual trading history than a supplier.

The result is that the headline discounts often fail to materialise on the bottom line. A more surgical approach is needed.

The first step for procurement teams is to get full visibility into their third party spend. With this in place they can identify opportunities to:

- Manage demand more proactively (both volume and specification and service level)

- Focus spend on contacts with advantaged pricing or volume-related terms

- Develop more focused negotiation strategies, supported by analysis of movements in market pricing and the underlying commodity indices.

The reality is that many operators will have significant opportunities, within their own control or where current contracts provide a mechanism to reduce prices. Understanding third party spend in detail provides the route to access these opportunities.

Get in touch

Whether your needing to reduce costs, understand the supply chain risks or reassess your strategy, we can help. Get in touch today to discuss your current business needs.

For details on how your data is used and stored, see our Privacy Notice.

Andy Tidy, Global Head of Performance Improvement