Are Japan’s upstream players heading for the exit?

Faced with competition from new sectors, upstream investment is under pressure

1 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

View Gavin Thompson's full profileJapan’s trading houses are re-thinking their long-term strategies around upstream investment. Last week, as Mitsui closed the sale of its BassGas stake in Australia, Sumitomo announced it will no longer participate in new oil projects. Sojitz had already announced a move away from upstream and Marubeni has kickstarted a process to sell off some of its upstream positions, including the UK North Sea. If 2020 was a year for the re-evaluation of future plans, then 2021 looks to be the year of implementation.

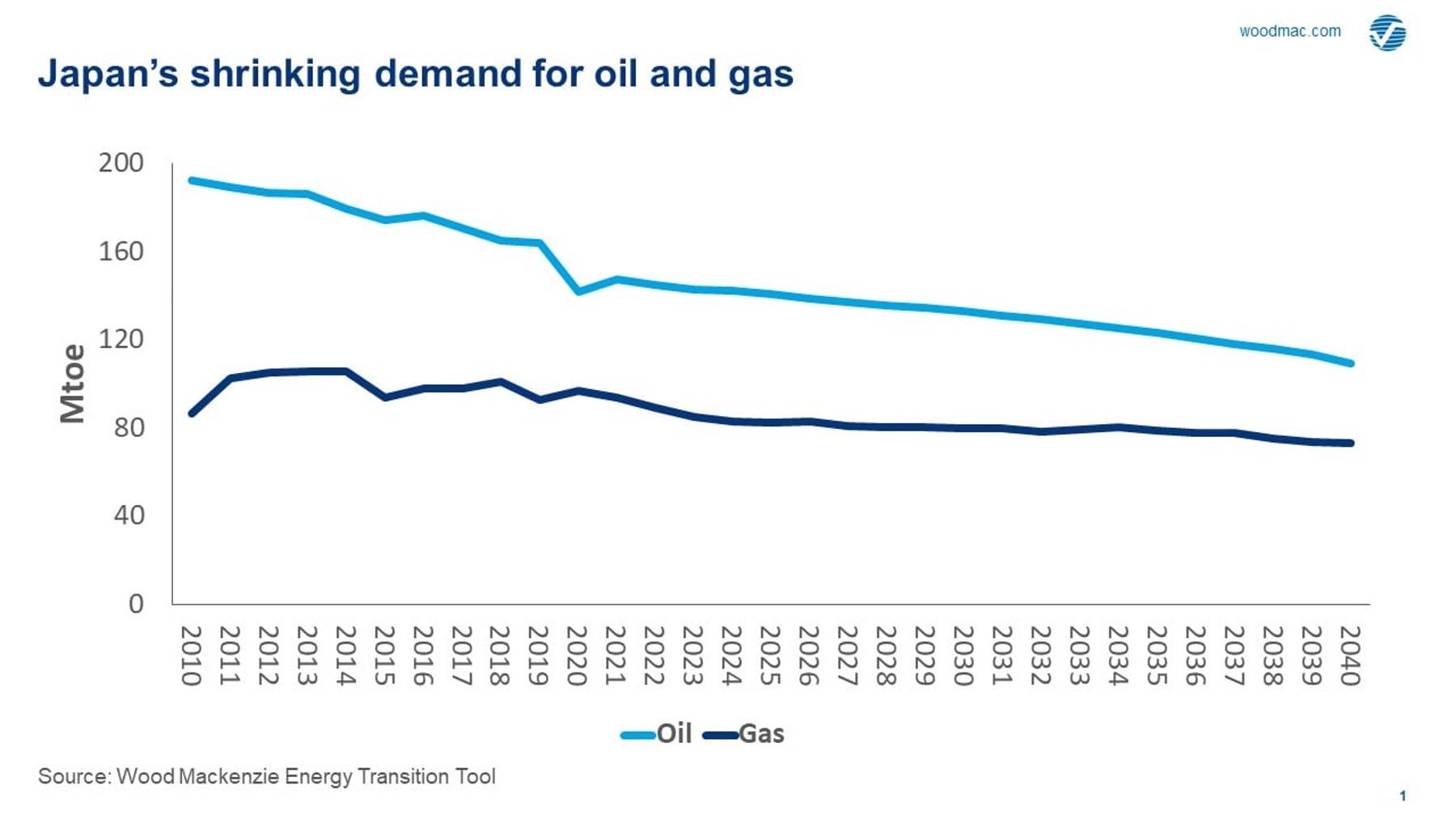

Moves by Japan’s trading houses to de-risk their upstream portfolios make sense. Faced with falling domestic oil and gas demand and an accelerating energy transition, future E&P investment is far less certain. Strategy reviews are switching focus to new growth areas - covering everything from fintech to pork bellies – with the increasingly diverse businesses of Japan’s trading houses challenging upstream for future capital.

To understand this changing outlook and the implications for the sector, I caught up with Angus Rodger, APAC Upstream Research Director.

Global upstream’s quiet investors

Japan is one of the great industrial economies, despite its extremely limited natural resources. Energy of course is critical to this, with the country having invested hundreds of billions of dollars worldwide to ensure the secure supply of coal, oil and LNG.

This hasn’t been limited to procurement contracts and multilateral financing. Collectively, and with little fanfare, Japanese companies – from pure-play E&Ps and integrated oil and gas companies, to gas and power utilities and trading houses – have built material upstream portfolios. Today, the upstream assets of ‘Japan Inc’ are valued at over US$70 billion, producing around 1.6 million boe/d. Trading houses making up almost 30% of this total. But with domestic oil and gas demand falling, the driver for Japanese firms to go out and secure international resources is weakening.

Read also: Global upstream oil and gas: new challenges ahead in 2021

Winds of change blowing across Japan’s upstream sector

The upstream businesses of Japanese trading houses have reached a critical juncture. For some, upstream is already looks non-core, seen by management and shareholders as a high-risk and capital-intensive sector, originally pursued in response to Japan’s lack of indigenous resources but increasingly non-critical to future growth. In addition, Japan’s trading houses typically hold small equity stakes in large, long-life LNG and oil projects. This has created portfolios with longevity, but little control or operator experience and lacking exposure to key global growth themes, such as deepwater and unconventionals.

As their businesses diversify across energy and non-energy sectors, upstream is feeling the pinch. Japan’s recently announced 2050 net zero target has piled on the pressure.

{kind=link}

The response is an increased focus on upstream portfolio rationalisation, and we expect the divestment of non-operated stakes in smaller oil and other non-core assets to gather pace. For several companies, beyond existing positions in LNG that are likely to remain intact, everything else may go. This is the sharp end of the energy transition.

Not all trading houses are equal

Mitsubishi and Mitsui account for over 80% of upstream portfolio value among Japan’s trading houses. And while oil assets may be increasingly peripheral, both have strong medium-term production and cash flow metrics as LNG projects in Mozambique, Russia and Canada come onstream. Others are in less fortunate positions.

But regardless of size, all trading houses face challenging longer-term growth outlooks due to mature portfolios, a lack of new development assets, and executive management teams increasingly reluctant to allocate precious capital to upstream investments. At the same time, many are also facing an increasing call on cash flow from upstream projects to support new energy investments. As a part of last week’s announcement that it will no longer invest in new oil projects, Sumitomo also revealed it will shift its focus to renewable energy investment. A similar narrative is being heard across the trading houses, referencing solar, wind, hydrogen and other new energy technologies.

Can Japan’s trading houses successfully divest?

Those trading houses looking to divest assets face headwinds. Equity positions are typically small, and some come wrapped up in complex Japanese JVs (Tangguh LNG, for example), potentially limiting buyer interest. Another increasing issue will be perceived ESG risk. Japanese upstream investments in oil sands, US Lower 48 (fracking) and the Arctic will be scrutinised by investors and financial institutions, particularly European banks looking to limit exposure to companies and projects in these areas.

On the plus side, we are increasingly positive around future M&A market activity. There are encouraging signs that debt markets are improving, with potential buyers accessing capital easier than in 2020, supported by stronger oil and gas prices and a weaker US dollar. There are buyers out there, but lots of sellers too – last week, South Korea’s KNOC also announced it was putting its North Sea portfolio up for sale, suggesting the ‘upstream question’ is not just being asked in Tokyo. More asset sales and company restructuring can be expected.

Implications for the wider Japanese E&P sector

Despite recent announcements, it’s important to point out that changing strategies do not necessarily signal a wholesale rush to the exit by Japan’s E&P companies. In many ways, they are getting ahead of the curve. Indeed, many will also be looking to take advantage of a buyer’s market, with numerous geographical and thematic options opening as IOCs expand divestment campaigns. There are well-priced opportunities out there, as evidenced this week by PTTEP’s deal to buy a stake in BP’s Omani Khazzan field.

Bigger players like INPEX have ambitious future production targets and will look to leverage a strengthening balance sheet to acquire undervalued upstream assets and diversify growth themes. For those small and medium-sized Japanese players, nimbleness is key as they look to target specialised capabilities, such as JXTG focusing on CO2 and EOR opportunities. And ongoing US shale gas purchases hint at a more counter-cyclical, integrated strategy from LNG players Tokyo Gas and Osaka Gas.

But there’s no doubt that for all Japanese E&P players, the strategic choices look hard. But Japan Inc won’t be disappearing from global upstream anytime soon. The potential for the Japanese government to play a role in facilitating upstream asset swaps or sectoral consolidation, allowing focused players to gain upstream scale while allowing others a route to exit, could hold the key to the future.

Read also: How far will upstream M&A activity rebound in 2021?

APAC Energy Buzz is a weekly blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.