Discuss your challenges with our solutions experts

Japan’s LNG decarbonisation challenge

Why should LNG emissions matter to Japanese buyers?

4 minute read

Gavin Law

Senior Vice President, Emissions & Low Carbon Fuels Consulting

Gavin Law

Senior Vice President, Emissions & Low Carbon Fuels Consulting

Latest articles by Gavin

-

Opinion

EU Methane Emissions Regulation Study: analysis of market impacts

-

Opinion

Shining a light on the “coal versus LNG emissions” debate

-

Opinion

Japan’s LNG decarbonisation challenge

-

Opinion

Is natural gas more emissions intensive than coal?

-

Opinion

Emissions intensity: portfolio composition is the key

Since the start of the war in Ukraine, and the subsequent decline in Russian piped gas supplies to Europe, the world has become considerably more focused on natural gas security of supply and affordability. The sustainability characteristics of LNG have become de-emphasised as buyers focus on the immediate supply challenges, and as such LNG-related emissions have perhaps dropped below the radar for many buyers. However, the issue of LNG emissions has definitely not gone away. It is widely expected that as supply security concerns ease later this decade following the ramp up of new supplies, the inevitable challenge of gas and LNG decarbonisation will come back into focus for governments, regulators and consumers, and this will feed through to LNG buyers. Buyers will also find themselves coming under increasing pressure to comply with mandatory climate disclosures in their country of origin.

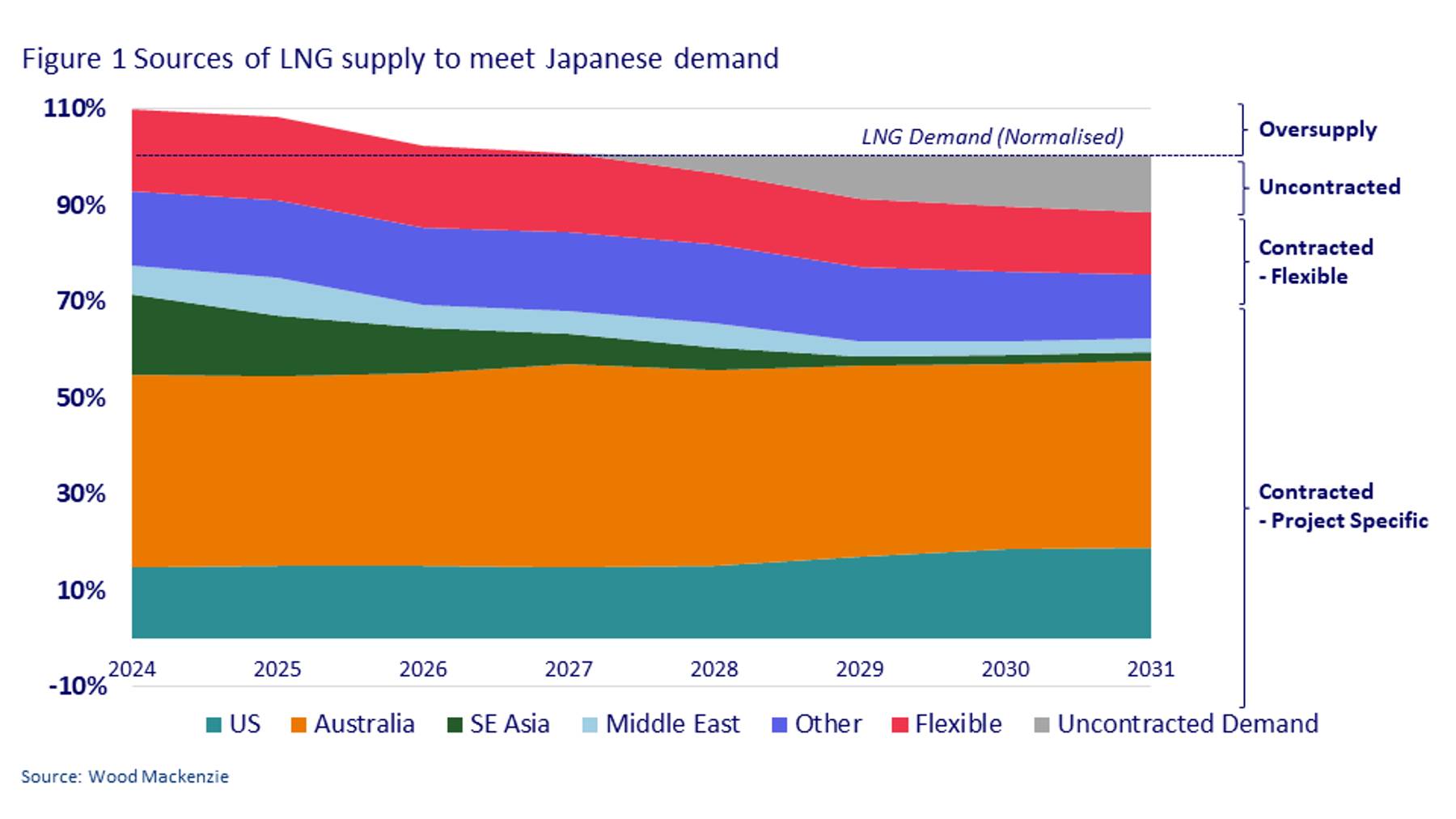

In Japan, LNG supply portfolios are evolving (Figure 1). In terms of supplies contracted from a specific project, with a decline in SE Asian and Middle Eastern supplies across the remainder of this decade, the market will be counter-balanced by a rising share of US and Australian LNG.

Flexible contracted supplies (which consist largely of contracts with international portfolio players such as Shell, BP, TotalEnergies, Woodside, Petronas, etc.), where the LNG is sourced from multiple supply projects (i.e. portfolio supply), remain relatively consistent across the period, meeting around 13-16% of demand.

While the Japanese market is currently over-contracted with excess volumes largely being traded into the international market, it is expected that by 2028 additional supplies will be required to meet domestic demand. This is despite the overall demand for LNG in Japan falling by around 7% between now and 2031.

What are the implications for the overall emissions intensity of Japanese LNG?

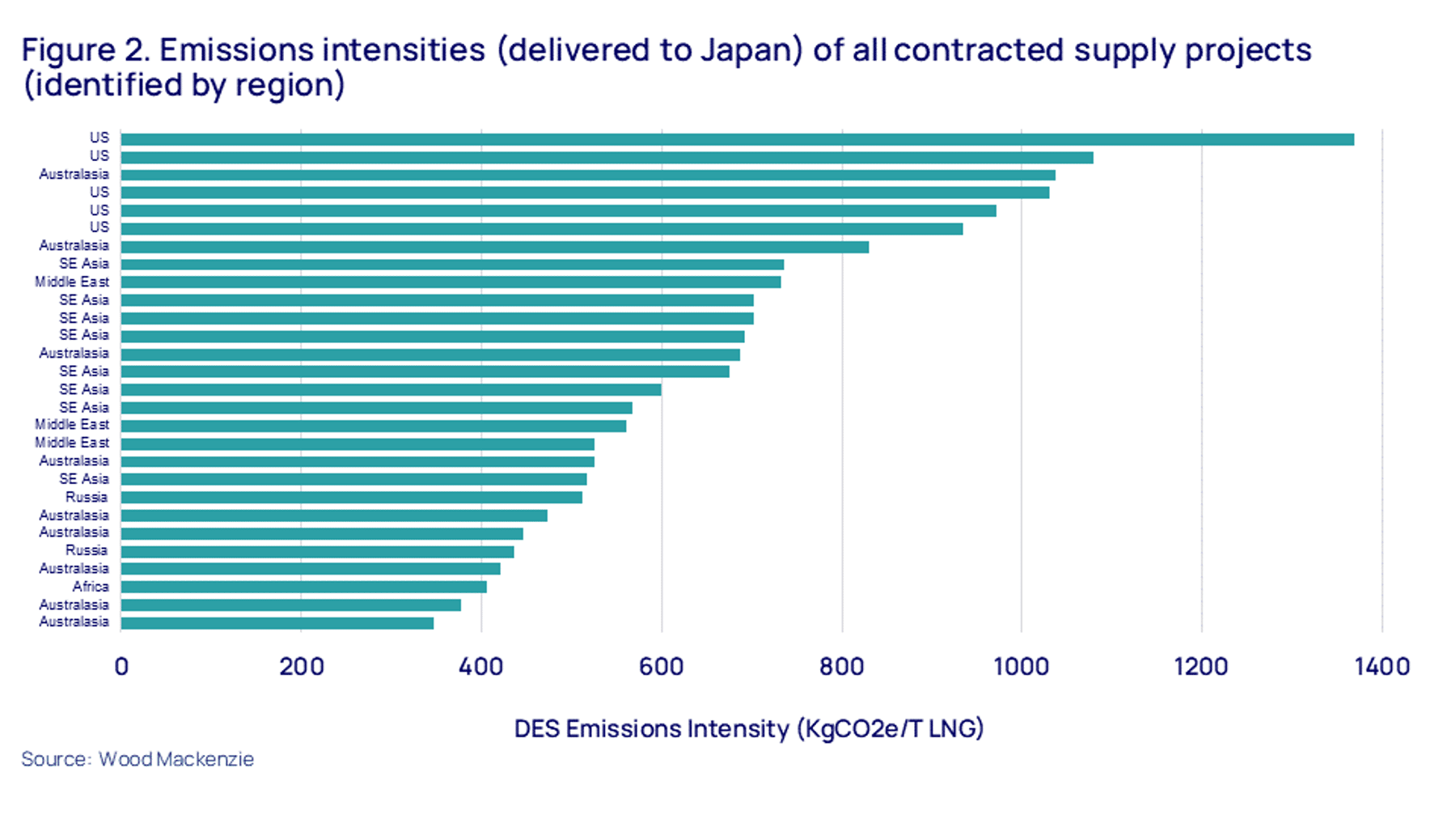

Japan currently has a wide range of LNG supply contracts; from very low emissions supply sources like PNG LNG to high emissions supplies from the US (Figure 2), and it is the balance of these different sources that dictates the overall intensity of the country’s supply portfolio.

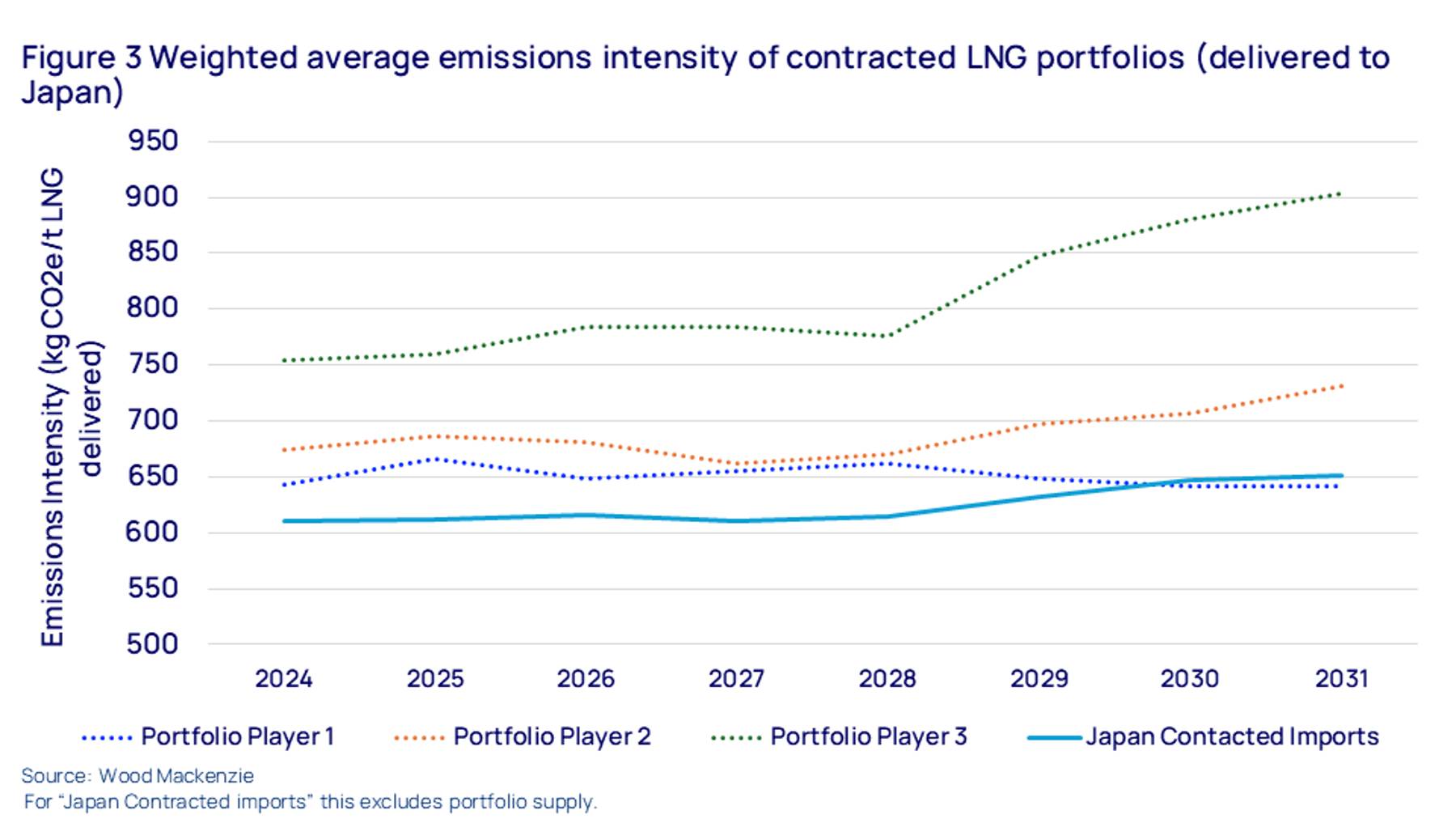

It is evident that while we expect an overall decline in demand for LNG over the next 7 years, the weighted average emissions intensity (“well to tank”) of the LNG supplies contracted from specific projects (as opposed to Flexible contracted supplies) will actually increase by around 7%, largely driven by the increasing share of US LNG in the supply mix (Figure 3). Also, with around 15% of Japan’s contracted supply coming from flexible sources, it is possible that this will further add to the emissions intensity of Japanese LNG, as most of the country’s largest portfolio suppliers of flexible volumes have portfolios which have higher weighted average intensities than Japan’s contracted imports from specific projects.

What can Japanese LNG buyers do?

The solutions to the challenge of Japan’s increasing LNG carbon intensity are limited. Existing contracts are largely fixed with little or no flexibility to change the supply source(s). Therefore, Japanese buyers must give careful consideration to the sources of any supply that they contract in the future, dedicated and portfolio, to avoid further escalations of the emissions intensity. This may involve more active negotiation of the sources that a seller can include in a portfolio (flexible) supply contract.

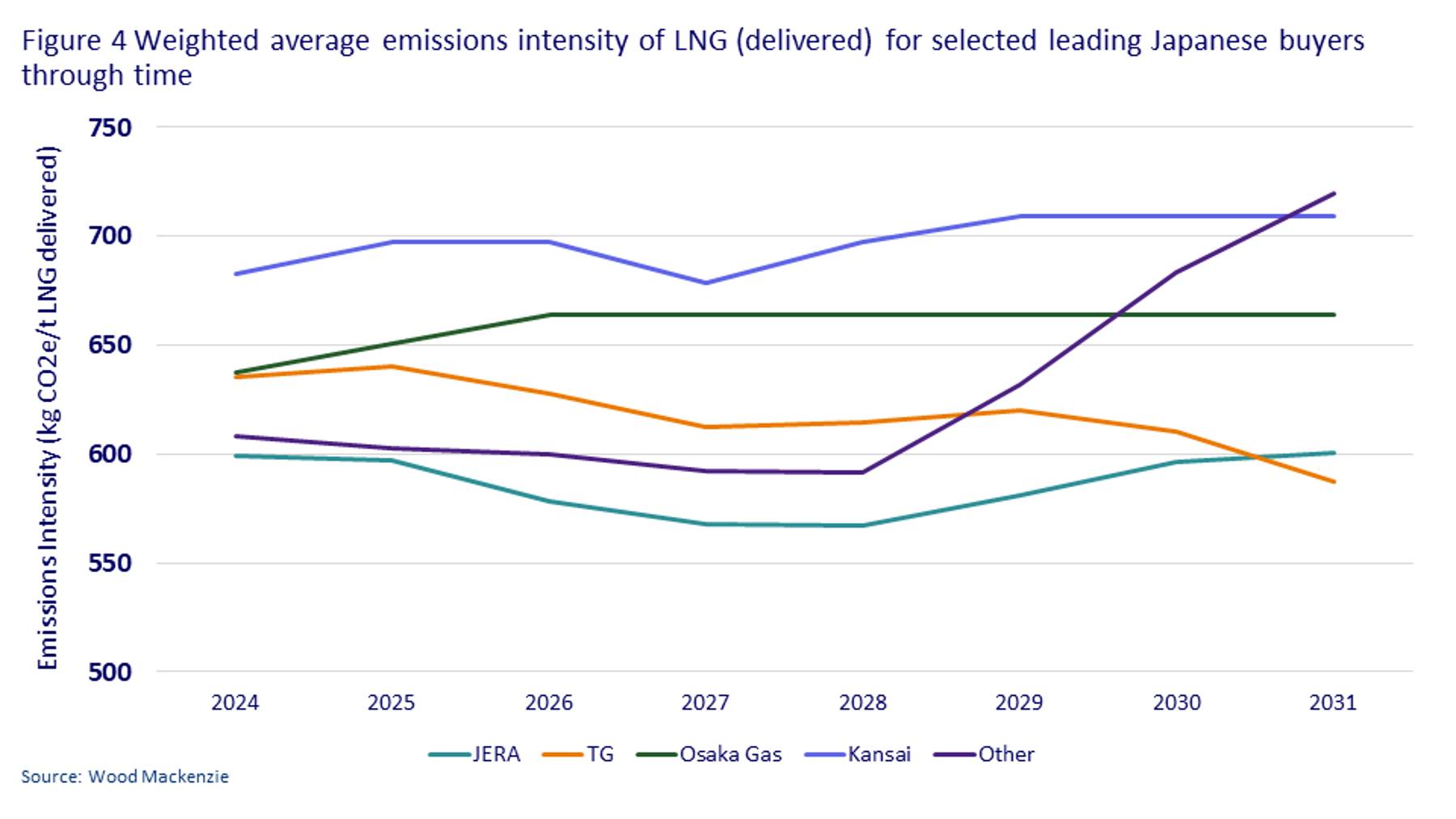

But not all Japanese buyers are in the same position (Figure 4). While the two largest importers, JERA and Tokyo Gas, demonstrate relatively stable or declining intensities across the time period, many of the medium to small buyers of LNG show increasing portfolio emissions intensities. This is largely related to the increasing proportions of US LNG and LNG from high CO2 venting projects such as Ichthys and Tangguh in their supply mix. In addition, for those buyers who have larger levels of flexible (portfolio) supply (eg. Tokyo Gas and some of the smaller buyers) there is potential for increased intensities if that portfolio supply is sourced from higher emissions sources such as the US.

For now, the emissions associated with LNG supplies are unlikely to be causing many Japanese buyers sleepless nights. But as security and pricing pressures ease, there will inevitably be a returning focus on sustainability. Buyers will likely feel increasing pressure from Government, regulators and customers to demonstrate a proactive approach to the decarbonisation of their LNG portfolios. Companies will need to bear this in mind as they make future decisions on the sources of flexible supply, as well as new contracted volumes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This analysis for this article was carried out using Wood Mackenzie’s new LNG Cargo Emissions Tool which provides an independent and transparent source of detailed “secondary” data of carbon emissions along the LNG value chain.

Got questions about how emissions affects your business?

Our Consulting team provides bespoke, independent advice that helps our clients navigate critical challenges. Find out more about how we can help you make decisions with confidence, or contact us via the form at the top of the page.

[1] “well to tank” emissions include all emissions up to the point of final combustion (upstream, pipeline, liquefaction, shipping and regas).