Australia’s gas conundrum

LNG exports are likely to fall from around 2030

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

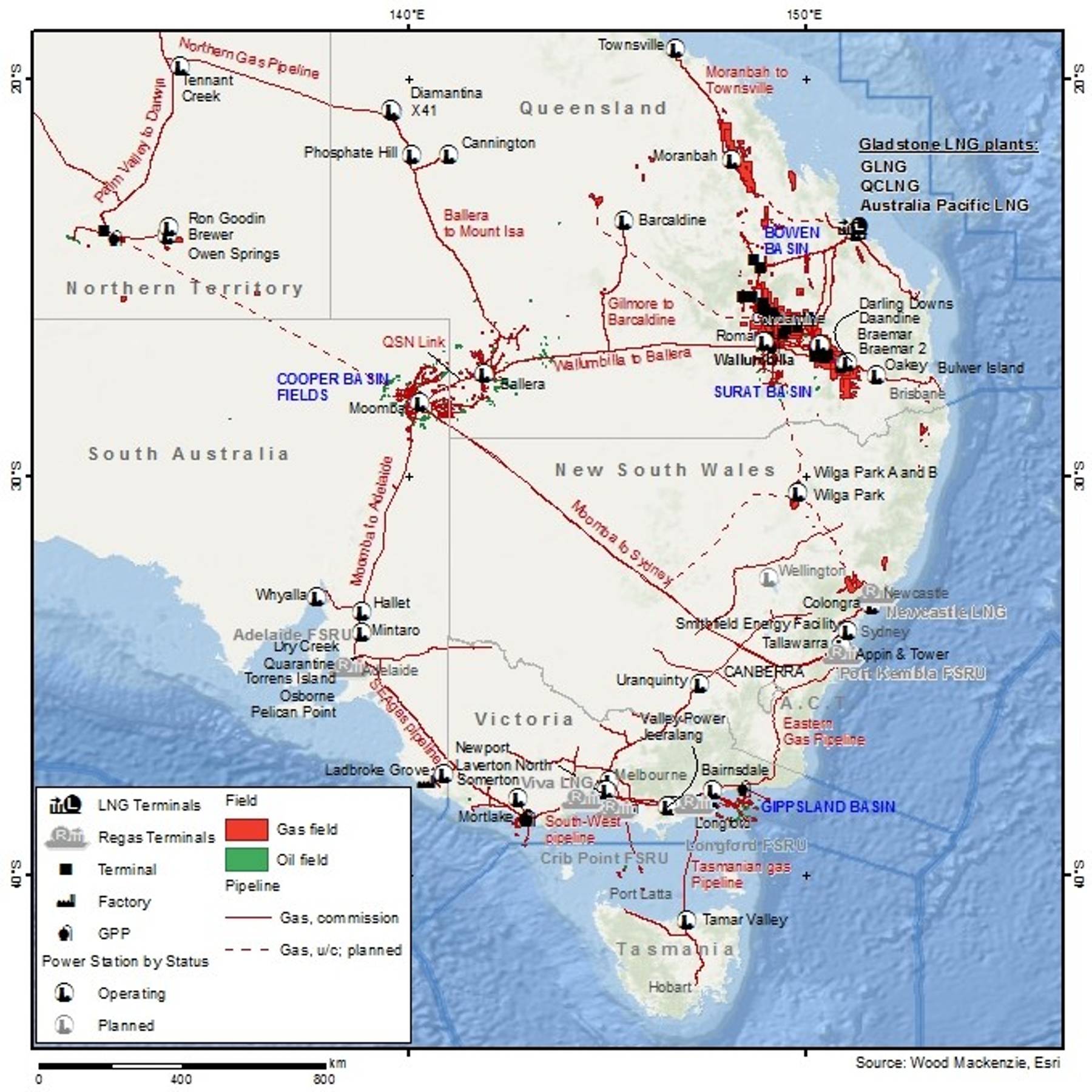

While it may well claim the crown of world’s largest LNG exporter in 2021, Australia faces rising problems with its gas. A combination of rising seasonal demand and maturing supply sources means that without significant new reserves coming onstream by the mid-2020s, the eastern and southern states of Queensland, New South Wales, Victoria and South Australia will be short of gas.

Further complicating matters, the domestic market is now in direct competition with the three Queensland LNG export projects, APLNG, QCLNG and GLNG, for east coast gas. With proposals for seven regas projects put forward in recent years, the door is now opening for LNG imports in just a few years’ time.

But the domestic gas demand outlook is increasingly being cooled by expectations of far stronger growth in renewable generation, while the prospects of gas supply availability into the east coast is now improving. With market dynamics potentially changing, how significant might eastern Australia’s gas shortfall be? How will it be filled? And what does it mean for Queensland’s LNG exporters? To understand more, I spoke with Dan Toleman from our APAC gas and LNG team.

East coast gas in good shape, for now

Australia’s east coast gas sector came into 2021 in rude health. LNG exports hit record levels last year, domestic gas availability improved, and average prices fell. But we can’t be complacent. The east coast supply-demand balance remains precarious, with brutal spending cuts of 2020 stalling the development of a significant chunk of much needed new supply. And declining production in the southern states inevitably makes Queensland supply even more critical, just as LNG export prices recover. Though now expected not to be as wide as anticipated just two years ago, a supply-demand gap is emerging and will continue to create opportunities for new domestic supply, LNG exporters and importers.

A narrower supply-demand gap

To understand this in more detail, we first need to consider the changing demand outlook. Looking at the Australian Energy Market Operator’s (AEMO) most recent forecasts out to 2039, the most significant change to the demand outlook comes from AEMO’s downward revision to gas demand in the power sector, driven primarily by stronger growth in renewables. AEMO also is more positive on the build-out of new transmission infrastructure to support renewables, as well as future investment in power system stability to support growth in wind and solar.

Next, we looked at supply, modelling all existing and potential supply into the domestic market and existing LNG export projects. The pandemic and the oil price crash have caused short-term delays to the development of new east coast supply, with APLNG announcing around US$250 million of capex cuts in 2020, Beach delaying the Otway development by a year and government approvals for Narrabri being delayed. Looking further out, we need to see exceptional exploration results if significant investment is to be made in the Beetaloo in the next five years.

But it wasn’t all bad news. Arrow’s FID on the Surat Gas Project FID in April last year was very welcome, meaning that the total east coast supply is now expected to increase from 2023 through to 2027, just when the market is expected to be shortest. We also now anticipate more volumes from APLNG over the same period. And while both the Otway Gas project development campaign and Narrabri have been delayed, each is now expected to produce more than previously anticipated.

As a result, the east coast gas shortfall now looks much less significant than previous outlooks. However, while we expect that through the 2020s the market will be more defined by seasonal gas shortages, longer-term challenges remain. Beyond 2030, eastern Australia’s gas shortfall would intensify, and although less severe than had been anticipated, without additional supply or imports, equity gas produced by the LNG JVs may be at risk of diversion to the domestic market.

Domestic gas prices increasingly set by Pacific spot LNG

With a more modest shortfall in the domestic market, we forecast a requirement for two LNG import terminals in the medium-term. LNG imports remain critical to balancing the market in the southern states, supporting the expected commissioning of an import terminal in 2023. The front runners are the Port Kembla FSRU in New South Wales and the Crib Point FSRU in Victoria.

{kind=link}

Netbacks to Asian spot prices continue to drive Queensland domestic gas prices, the alternative market for Queensland volumes. With winter peak prices in Australia coinciding with softer northern hemisphere summer prices, LNG imports should be competitive as early as the 2023 Australian winter as these will initially only be required to meet seasonal winter demand.

Once LNG imports begin, southern market gas prices will also be increasingly linked to Pacific LNG spot prices. In the absence of new domestic upstream supply, LNG imports into the southern states will increase and become the marginal supplier to the market, creating upward pressure on prices. As the global LNG market tightens beyond 2027, domestic prices will strengthen, potentially climbing north of A$10/GJ by the late 2020s.

Implications for Queensland’s LNG exporters

Australia’s LNG exports will increase off the back of new domestic supply. Meanwhile, LNG imports will not hit full capacity until the late-2020s, with the export projects the biggest beneficiaries of softer demand and increased supply, with exports potentially increasing above contracted levels between 2023-27. APLNG remains in the strongest position to meet nameplate capacity, while QCLNG has been strengthened by the Arrow FID.

By around 2030 however, export volumes begin to decline to below contract levels as more feedgas is required by the domestic market and supply declines. Unless additional feedgas can be monetised, Queensland’s LNG exporters will need to source alternative LNG to make up for the shortfall in their contracted volumes. Australia’s gas conundrum looks set to rumble on.

You might be interested in: Australian coal exports bounce back from China’s ban

APAC Energy Buzz is a weekly blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.