Benchmarking the Middle East NOCs against the supermajors

How do ADNOC, QatarEnergy and Saudi Aramco compare against BP, Chevron, ExxonMobil, Shell and TotalEnergies

3 minute read

Neivan Boroujerdi

Director, Corporate Research

Neivan Boroujerdi

Director, Corporate Research

Neivan leads Wood Mackenzie's global corporate NOC coverage.

Latest articles by Neivan

-

Opinion

Video | Venezuela in global portfolios: risk, restraint, and strategic optionality

-

The Edge

NOCs begin a new phase of upstream internationalisation

-

The Edge

The complexity of capital allocation for oil and gas companies

-

Opinion

Ten key considerations for oil & gas 2025 planning

-

Opinion

ADNOC doubles net hydrogen production through stake in ExxonMobil’s Baytown project

-

Opinion

ADNOC acquires stake in Rovuma LNG from Galp

ADNOC, Qatar Energy and Saudi Aramco, are increasingly talking – and acting – like integrated oil companies (IOCs). But how do these national oil companies (NOCs) compare against the biggest IOCs of them all, the supermajors?

In our latest report we leverage data from Wood Mackenzie’s new Corporate Strategy & Analytics Service to benchmark ADNOC, QatarEnergy and Saudi Aramco against their supermajor rivals. Fill out the form at the top of the page to download an extract from the report or read on for a quick overview of some of its findings.

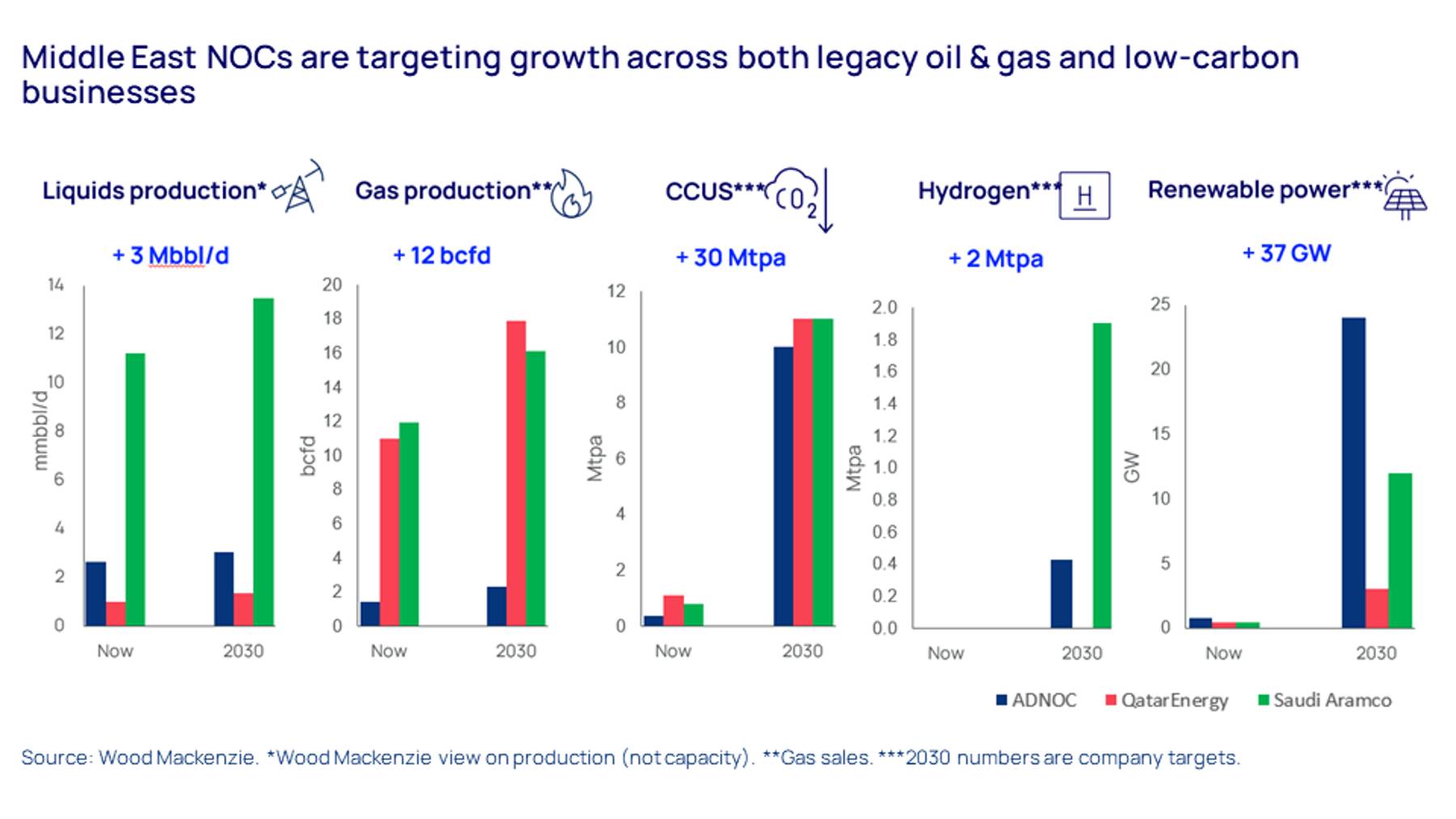

Middle East NOCs are progressing multiple growth strategies

ADNOC, QatarEnergy and Saudi Aramco continue to grow oil and gas production capacity but are also stepping out beyond their domestic asset base to expand and diversify their businesses. While capital allocation remains heavily concentrated towards oil and gas, all are looking to grow internationally in areas including exploration, LNG, downstream, CCUS, hydrogen and even renewables.

{kind=link}

Upstream businesses stand out for their size, quality and longevity

All three continue to grow oil and gas capacity and are accelerating the development of domestic resources. While the majors face a struggle to maintain upstream output in the medium to long term, production from this peer group will be higher in 2050 than it is today. In absolute terms, Saudi Aramco continues to be in a league of its own.

The quality of the three’s resources also stands out, with advantaged low-cost assets providing high-margin barrels and molecules. Based on our long-term price assumption of US$65 per barrel, combined upstream free cash flow will average over US$200 billion per year – that’s close to the market cap of Shell.

The group’s main ’weakness’ is that their portfolios are overwhelmingly focused on their home countries. While being concentrated within some of the world’s best basins is clearly a positive, all three are taking measures to diversify their portfolios; ADNOC and Saudi Aramco are targeting international gas, while QatarEnergy is growing globally via exploration.

Despite growth, downstream profits are lower than the supermajors

Compared to their impressive upstream portfolios, downstream is a relatively weak area for the three with cash margins typically lower than that of the supermajors. Saudi Aramco’s international M&A strategy has been focused on expanding its downstream portfolio, seeking to improve integration and secure offtake. Refining capacity for ADNOC and QatarEnergy is less of a priority, but both are still expanding into chemicals and speciality products.

ADNOC and Saudi Aramco lead the sector for emissions intensity

Decarbonisation – rather than diversification – has been the key focus for the Middle East NOCs’ energy transition strategies so far. ADNOC and Saudi Aramco boast peer-leading Scope 1 and 2 carbon emissions intensity, positioning them well to ‘outlast’ other producers.

By comparison, QatarEnergy’s LNG-weighted portfolio is far more carbon intensive but value at risk is low due to regional carbon price forecasts – in this respect, where you emit is more important than how much you emit.

In absolute terms ADNOC and Saudi Aramco’s low carbon spend ranks alongside energy transition leaders

The three Middle East NOCs have made less progress in developing their low-carbon portfolios but in absolute terms, ADNOC and Saudi Aramco are now investing as much as ‘transition leaders’ BP and TotalEnergies. An international growth strategy is advancing ADNOC’s capabilities whereas Aramco and QatarEnergy remain domestically focused.

CCUS capacity targets look within reach, but more business development will be needed to hit targets for renewables and hydrogen.

However, all three Middle East NOCs have the platform – and firepower – to step up their low-carbon strategies to meet the challenge.

Our new Corporate Strategy & Analytics Service provides clients including major Oil & Gas players with corporate-level strategic analysis and sector benchmarking to underpin board-level decisions. Get in touch to find out more about how it can help your business.

In the meantime, don’t forget to fill out the form to download your free extract from the full report.

Corporate Strategy & Analytics Service

Corporate-level strategic analysis and portfolio benchmarking of Oil & Gas, Power & Renewables and Metals & Mining sectors to underpin board-level decisions.

Explore CSAS