How US shale and deepwater are reshaping Major upstream competitiveness

The biggest game in town

1 minute read

Ryan Duman

Director, Americas Upstream

Ryan Duman

Director, Americas Upstream

Ryan specialises in supply forecasting, basin characterisation, upstream decarbonisation and economic modeling.

Latest articles by Ryan

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

-

Opinion

How US shale and deepwater are reshaping Major upstream competitiveness

-

Opinion

US shale gas is back: new demand signals underpin upstream opportunity

-

Opinion

US shale gas is back: new demand signals underpin upstream opportunity

-

Opinion

Gas prices enter a bearish spring amid crude market volatility

-

The Edge

Three factors driving US liquids production to new heights

Miles Sasser

Senior Research Analyst, Upstream

Miles Sasser

Senior Research Analyst, Upstream

Latest articles by Miles

-

Opinion

How US shale and deepwater are reshaping Major upstream competitiveness

-

Opinion

Gulf of America upstream: our view on rig rates

-

Opinion

Energy policy shifts: navigating the One Big Beautiful Bill

-

Opinion

How badly did Hurricane Rafael hit oil & gas?

Matt Woodson

Principal Analyst, US Lower 48

Matt Woodson

Principal Analyst, US Lower 48

Matt works on the US Upstream research team with a focus on company asset modelling.

Latest articles by Matt

-

Opinion

How US shale and deepwater are reshaping Major upstream competitiveness

-

Opinion

US Lower 48: 4 things to look for in 2024

-

Opinion

The making of a Megamajor – ExxonMobil acquires Pioneer Natural Resources

-

Opinion

A new tight oil powerhouse: Permian Resources and Earthstone create a new large-cap US E&P

The United States is unarguably the world's most attractive upstream market, adding 2 million boed between 2020 and 2025. Stable regulation, unmatched shale resources and competitive Gulf of America deepwater returns are continuing to attract capital.

As global upstream opportunities narrow, US positioning has become increasingly important. Indeed, all global Majors are planning to maintain or expand their US exposure.

US size matters

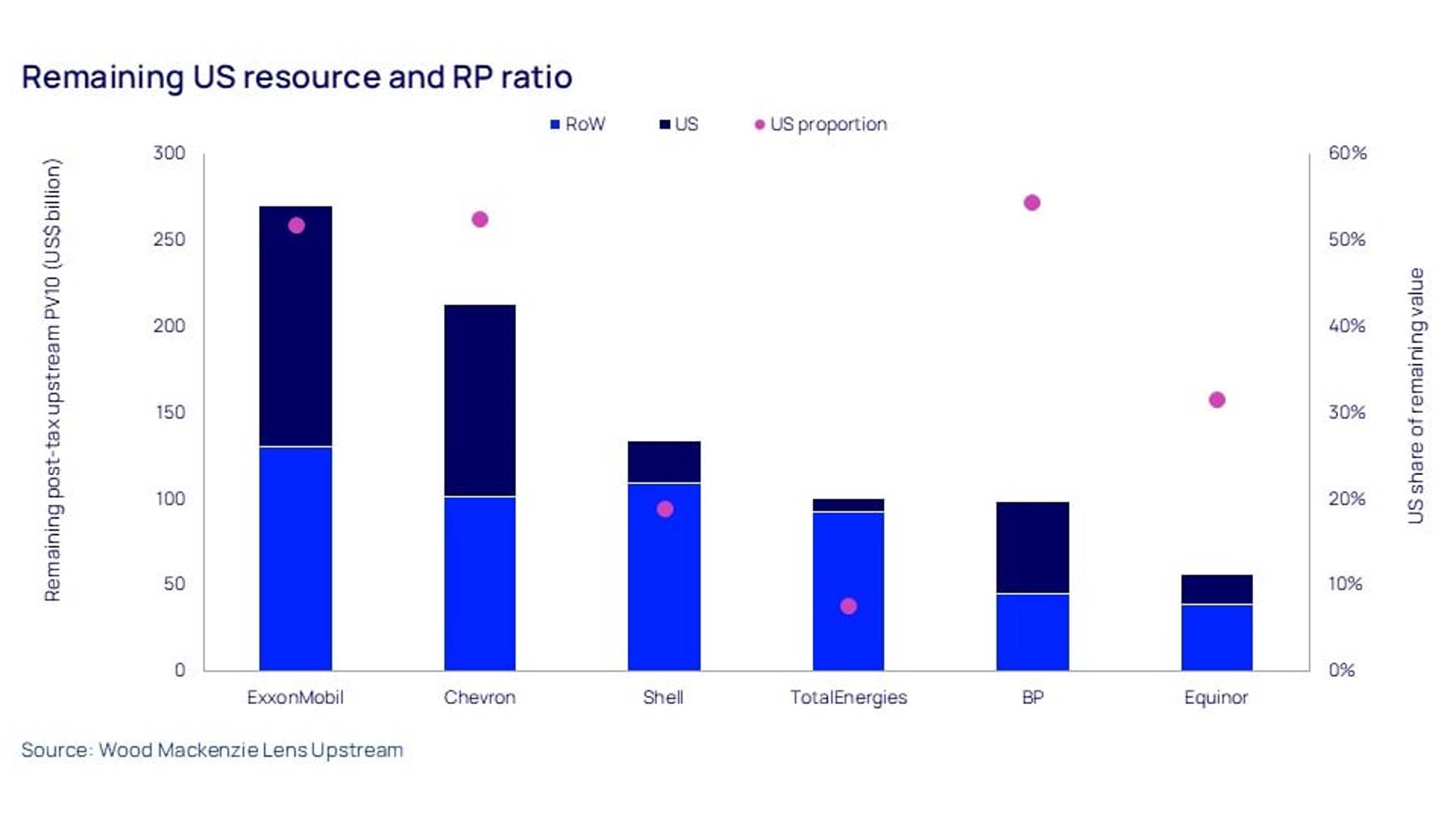

The US delivers more than 50% of upstream value for BP, ExxonMobil and Chevron, but only the latter two have the scale to match, dominating the resource base and capex, with competitive sub-US$35/bbl breakevens.

ExxonMobil dominates in terms of inventory, with 99% onshore resources and a 30-year reserve life, followed by Chevron (93% onshore, 20 years) and BP (80% onshore, 22 years). Shell, TotalEnergies and Equinor hold a fraction of the top-three inventory.

{kind=link}

BP’s 54% US value share reflects its growing reliance on the US as lower-margin global regions weigh on performance. Its reserve life will compress under its growth plans. Shell, meanwhile, faces a production decline without an onshore US buffer.

ExxonMobil, Chevron, Equinor, BP and others are all set to increase their US exposure over the next decade, be it through Permian growth, Gulf of America deepwater, or geographical concentration driven by a decline in international portfolios.

BP announced in February 2025 that it was channelling 75% of capex to upstream oil and gas, with bpx, its US onshore oil and gas business, targeting 650 kboed by 2030. It is eyeing 10 new projects by 2027, with US Paleogene in the Gulf of America to deliver one-third of its deepwater production by the 2030s.

TotalEnergies, meanwhile, has made three US gas acquisitions since 2024, feeding its position as the largest US LNG exporter. Equinor is targeting 50% of its international profits from the US, the highest-value production in its portfolio.

Fill out the form at the top of the page to read the rest of this article, which delves into their plans, how strategies are diverging, where potential success and failure may lie, and what this means for E&Ps .