Is natural gas more emissions intensive than coal?

We examine what we know about CO2 emissions along the value chains of both gas and coal

1 minute read

Gavin Law

Senior Vice President, Emissions & Low Carbon Fuels Consulting

Gavin Law

Senior Vice President, Emissions & Low Carbon Fuels Consulting

Latest articles by Gavin

-

Opinion

EU Methane Emissions Regulation Study: analysis of market impacts

-

Opinion

Shining a light on the “coal versus LNG emissions” debate

-

Opinion

Japan’s LNG decarbonisation challenge

-

Opinion

Is natural gas more emissions intensive than coal?

-

Opinion

Emissions intensity: portfolio composition is the key

Recent press articles have speculated that despite natural gas' clean credentials, direct emissions of methane (both accidental and deliberate) into the atmosphere may actually make natural gas more carbon intensive than coal on a full life cycle basis.

While there is ongoing debate around the actual levels of methane emissions along the gas value chain, we examine what we know about CO2 emissions along the value chains of both gas and coal and ask the question "what would you need to believe about methane losses for gas to be worse than coal from an emissions standpoint?"

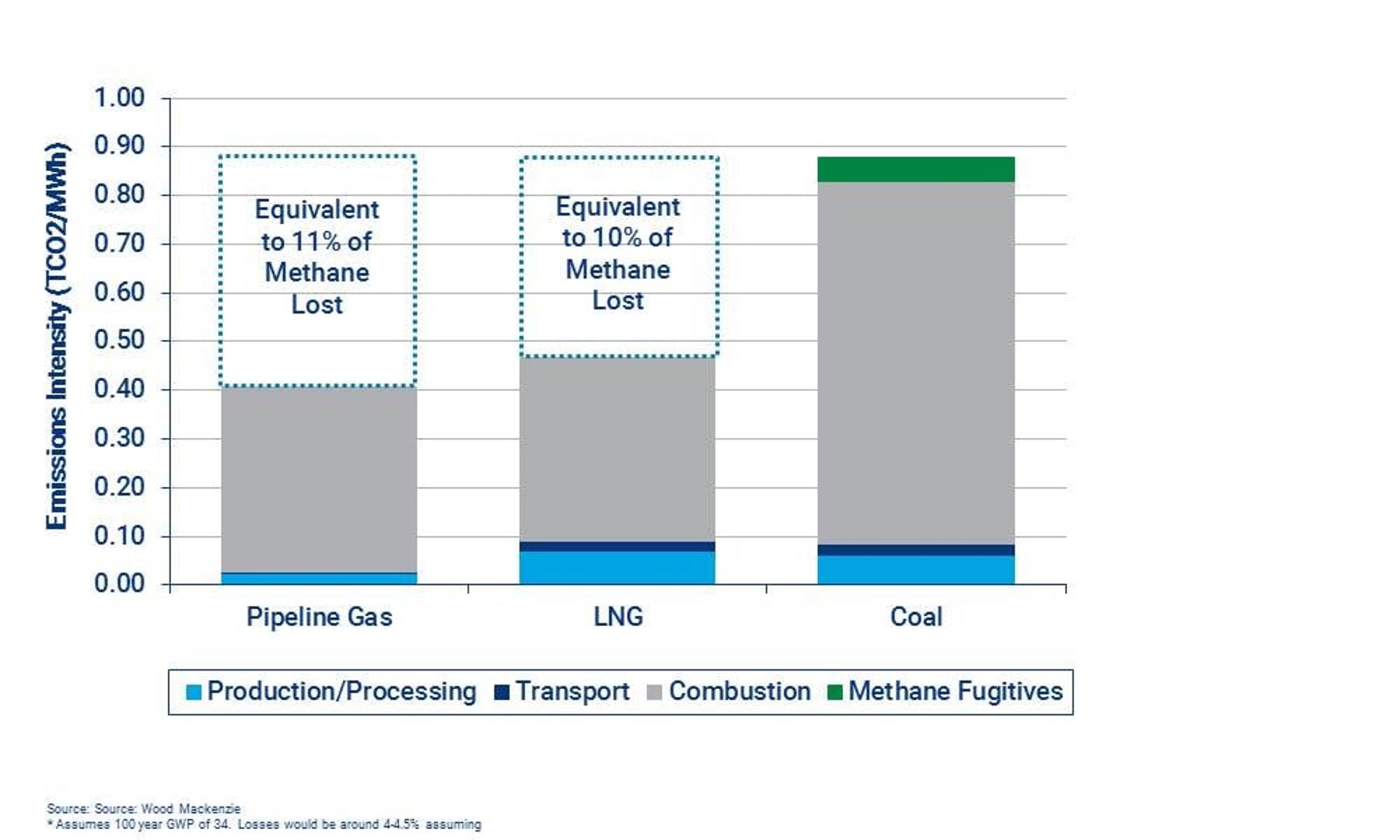

This analysis uses assumptions from our recently completed multi-client study, Positioning for the future: Benchmarking corporate upstream emissions and value at risk, and from Wood Mackenzie's power/renewables and coal research. The key assumptions are summarised at the end of the article. On this basis, the overall CO2 emissions from coal per MWh of power produced are about twice those associated with gas. In order for gas to be worse than coal, then, the difference between the two would need to be accounted for solely by methane emissions.

{kind=link}

For the calculation of methane on a CO2 equivalent basis, it is standard practice to use the “global warming potential” or GWP as a multiplier, thus allowing it to be combined with combustion CO2 emissions to produce a total CO2 equivalent figure. Since methane absorbs much more heat than CO2 in the atmosphere, but is significantly less stable, this conversion is relatively complex and depends upon the study timeframe. As quoted by the IEA, a tonne of methane is equivalent to between 28 and 36 tonnes of CO2 when considering its impact over a 100-year timeframe and between 84 and 87 tonnes over a 20-year timeframe (IEA: The environmental case for natural gas, October 2017).

For gas to have higher emissions than coal, we calculate that more than 10 -11% of the produced gas would need to be lost along the value chain assuming a 100 year GWP (4-4.5% using a 20 year GWP). Since we know that methane losses in shipping and regas are relatively low, it would be reasonable to assume that the majority of these losses would have to originate in the production/processing and pipeline transportation stages.

It should be noted that these losses of natural gas are associated with leakage into the atmosphere and should not be confused with gas that is consumed as fuel in the LNG plant, LNG tankers, gas compressors, etc. and subsequently emitted as CO2.

To put this in context, if we were to assume this level of methane emissions from natural gas production across the globe it would equate to around 35 bcfd, ie. almost three quarters of the demand for gas in Europe or nearly a half of that in the US. While the level of methane emissions in the gas value chain remains a point of debate within the industry, it seems highly unlikely that the global industry would be comfortable with losing this amount of product without taking immediate remedial action.

Indeed, we estimate that if natural gas losses were as high as this, then gas producers would be losing a huge amount of value on a daily basis. For example, it is estimated that with 10.5% losses of all natural gas production, Shell, one of the more gassy majors, would lose over $1 billion a year in profits and would forgo around $12.5 billion in corporate value. It is hard to imagine that such significant figures would not provide the financial incentive to address such a potentially solvable problem.

While there are numerous studies highlighting specific circumstances (particularly focussed around onshore US production) where the level of methane emissions (both fugitives and deliberate release) are shown to be significant and may be as high as 5-6%, it is important not to consider these as representative of the natural gas industry as a whole There will always be exceptional situations where methane emissions are particularly high (or indeed low) but it is important that these exceptions do not become seen as the rule and thus confuse the debate.

Although the oil and gas companies continue to improve their understanding of methane losses (and subsequently report this to investors), it is important to examine this issue in light of what we know now and what is reasonable to believe. It is perhaps unreasonable to believe that up to 35 bcfd of gas is lost to the atmosphere across the globe and to assume that a sector which is renowned for innovation and commercial discipline would be willing to allow the kind of value loss discussed above. It is therefore perhaps also unreasonable to assume that in general the level of methane emissions is high enough to make natural gas more emissions intensive than coal (even using a 20 year GWP). While there are undoubtedly specific examples where methane losses may in fact be large enough for coal to challenge gas, these are likely to be exceptional.

There is little doubt that reducing the level of methane losses will have a significant impact on overall carbon emissions. However, it is reasonable to assume that on average natural gas is significantly less emissions intensive than coal and still represents the logical fossil fuel to support the energy transition in the coming decades. To think differently, one would need to believe that global losses of gas are so great that they could satisfy demand in a small continent and that major oil and gas companies are happy to forgo billions of dollars of value rather than stem the losses.

As we transition into 2019, the mood in the LNG market is mixed. What will 2019 look like? Get our analysis here.

Global Gas and LNG: 6 things to watch for in 2019

Visit the store to find out more about this report