Sign up today to get the best of our expert insight in your inbox

Making CCUS work in Asia Pacific

Regulatory, commercial, and technical alignment is essential for progress

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Carbon capture, utilisation and storage (CCUS) is red hot. Worldwide, the CCUS project pipeline for capturing carbon emissions from the use of fossil fuels in electricity generation and industrial processes is edging towards a billion tonnes of CO2 per annum. At the current rate of growth, CCUS capacity will come close to what’s needed in our 1.5 degree pathway to 2030.

But the global distribution of CCUS projects is uneven. North America accounts for over two thirds of capacity, with western oil and gas companies having led the march. Much of this has been underpinned by dedicated legislation: the US is the global leader in no small part due to its 45Q tax credit incentive for carbon sequestration at oil and gas projects, while Canadian CCUS is supported through high carbon taxes, low carbon fuel standards and tax credits for depreciation. Meanwhile in Europe, governments have introduced policies to support CCUS hubs, including development grants and the licensing and permitting of geological CO2 storage.

{kind=link}

Across most of Asia Pacific it is a different story. Despite a growing pipeline, only Australia and Japan have operational CCUS projects, and most governments are only now recognising that policy support is essential to drive investment.

What must governments across Asia Pacific do to ensure the ramp up in new projects, which countries are showing the most progress and what role can oil and gas companies play in delivering CCUS across the region?

The CCUS state of play in Asia Pacific

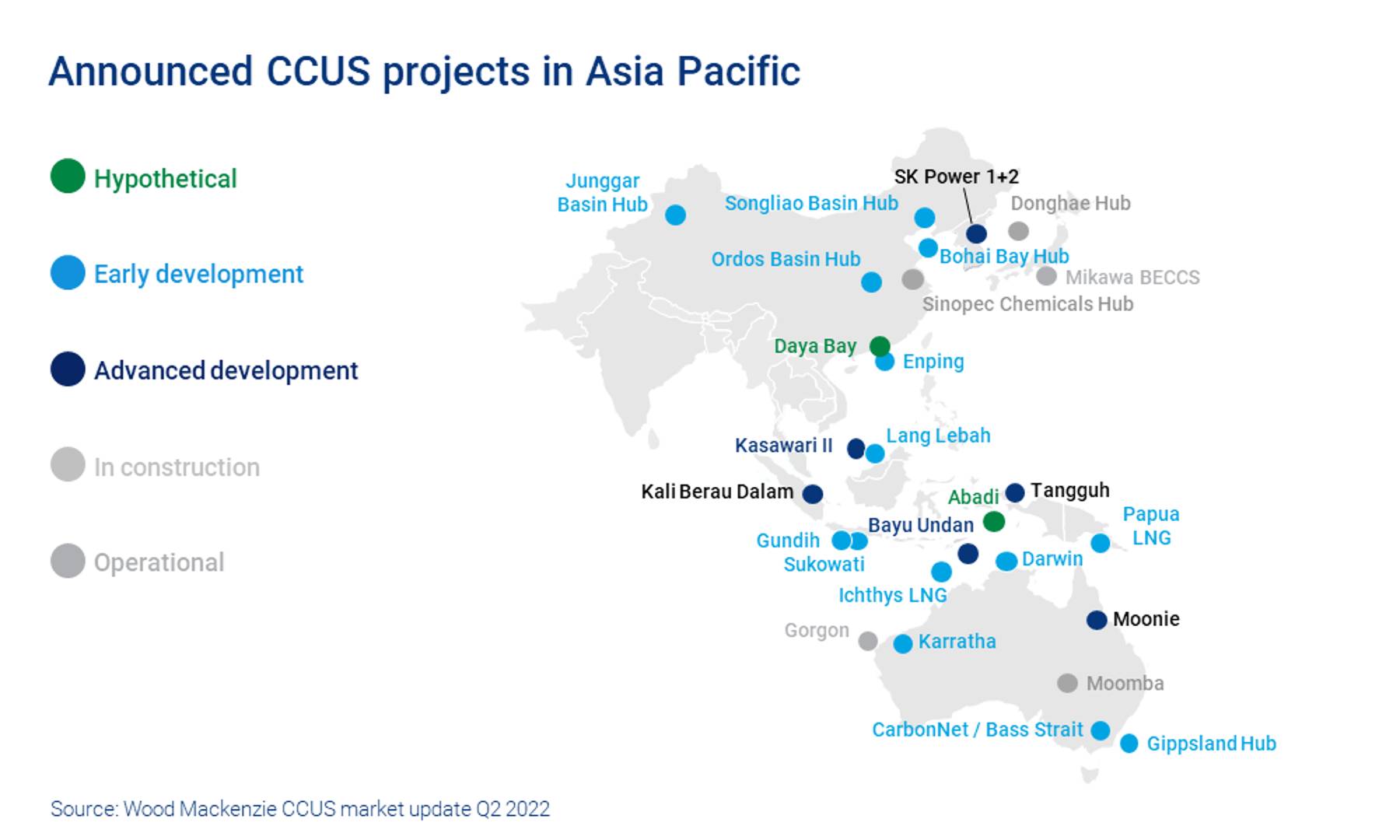

From a slow start, Asia Pacific’s CCUS project pipeline is growing. Cumulative capacity is expected to reach above 90 million tonnes by 2030, though many projects remain risked and will require further regulatory support.

Australia’s upstream and LNG producers are leading the field. Despite its challenges, Chevron’s Gorgon project remains the largest operational CCUS project worldwide with dedicated storage (several larger North American projects use CO2 for Enhanced Oil Recovery).

Many of Australia’s LNG projects face significant challenges to decarbonise. Ichthys, Prelude and Barossa/DLNG are among the most carbon intense of all integrated LNG projects globally, making CCUS investment essential alongside renewable energy, electrification and batteries to decarbonise LNG.

Australian CCUS investment is being underpinned by some of the strongest policy and regulatory support in the region. Since 2021, CCUS projects can earn Australian Carbon Credit Units (ACCUs) that can be either used to offset emissions or sold on. In addition, Australia this month awarded several offshore greenhouse gas assessment permits to assess storage potential in the Carnarvon and Bonaparte basins for potential CCUS hub projects.

But Australia will need to go further if it is to develop new sources of gas. We identify almost 90 tcf of undeveloped resource in Australia. Unlocking this resource is not just about high gas prices and partner alignment – decarbonising the value chain and CCUS is really the key.

China’s CCUS potential is now attracting investment from its NOCs and their international partners. CNPC is planning China’s first CCUS hub in the Junggar Basins that will allow the company to pool large volumes of CO2 from clusters of industrial processes and sequester these in depleted oil and gas reservoirs across the basin. Also in China, Shell, ExxonMobil and CNOOC announced an MoU in June to evaluate China’s first large scale offshore CCUS hub at Daya Bay.

In Wood Mackenzie’s AET-1.5 degree scenario, Asia Pacific accounts for some 50% of global CCUS capacity. Governments and companies across the region must act decisively to ensure this becomes a reality.

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

To date, both China’s national carbon emissions trading scheme and policy support for CCUS remain insufficient to support this type of investment on a major scale. But done right, the potential for both China’s NOCs to transform their legacy upstream basins into CCUS hubs is enormous.

In Southeast Asia, Malaysia and Indonesia were early movers in recognising the potential for CCUS. However, progress has since diverged. While PETRONAS has emerged as a regional leader, with the focus on its Kasawari project, Indonesia remains at the ‘white paper’ stage. The disappointing appraisal results on Repsol’s KBD block gas discovery looks set to be downgrade the project, and with it Indonesia’s flagship upstream CCUS project.

How can CCUS work in Asia?

With the ultimate success of CCUS projects in Asia Pacific dependent upon regulatory support and commercial attractiveness, much work is still to be done. Across most of the region, favourable fiscal terms, grants and tax credits, sufficient carbon prices and storage licensing are simply not yet in place. But progress is being made. Australia has introduced carbon credits and China has implemented an Emissions Trading System (ETS). Similar schemes are under development in Thailand, Vietnam, Malaysia and Indonesia.

A key question for developers is how much will CCUS cost? Without visibility on revenue and savings on emissions costs, projects will stall. In addition, supportive regulatory frameworks, including clarity on licensing processes, allocation of liabilities, and the impact on existing fiscal terms, must be unequivocal. Asian CCUS projects could also consider attracting Voluntary Carbon Market (VCM) credits from major corporates and funds looking to offset their emissions as regulation evolves.

Thinking big around Asian CCUS hubs

Governments and oil and gas producers in Asia Pacific typically view CCUS as a single project carbon emission solution. This is very different in scale and ambition to Europe and North America, where policy and investment is being directed towards bigger and more complex commercial CCUS hubs. This involves clusters of industrial sources of CO2 near basinwide storage, derisking development by enabling efficiencies of scale and shared cost. Today, hub projects account for over 80% of the planned CCUS pipeline, but only a fraction of this sits in Asia Pacific.

CCUS hubs must be made to work in Asia. Australia and China are now progressing hub concepts, but far more ambition is required. Shell, for example, is looking beyond local contaminated gas and is thinking about how depleted reservoirs (or aquifers) offshore Sarawak could help decarbonise bigger targets, such as nearby Singapore. This is exactly the ambition Asia Pacific needs, but this type of cross-border CCUS hub will require dedicated regulatory, commercial and technical support on a scale that has yet to be seen in region.

Outside of Australia, the pace of CCUS development across Asia Pacific will largely be dictated not by private companies, as in Europe and the North America, but by NOCS. This could have differing outcomes: in China, the weight of central planning behind NOC plans could act to accelerate approvals and project development. In other countries, the risk of NOC dominance may steer IOCs away from deeper involvement.

Putting Asia Pacific at the heart of CCUS

Despite momentum in Asia Pacific’s CCUS pipeline, much more progress is required to meet 2050 greenhouse gas targets. Upstream and LNG players can blaze the trail across the region, with CCUS not only decarbonising their projects but also opening the door to carbon capture for energy intensive industries beyond the oil and gas value chain.

In Wood Mackenzie’s AET-1.5 degree scenario, Asia Pacific accounts for some 50% of global CCUS capacity. Governments and companies across the region must now act decisively to ensure this becomes a reality.

APAC Energy Buzz is a weekly blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.