Making sense of Asia’s sky-high spot LNG prices

Blistering prices more a function of limited liquidity than justifiable fundamentals

2 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

In April last year, I wrote an APAC Energy Buzz entitled ‘How low could Asian spot LNG prices fall this summer?’ It was a fair question. Lockdowns, recession and massive oversupply were all testing new floors for LNG prices. And while this was a tough time for the industry, I concluded on an optimistic note: “The hope for the LNG industry is that economic recovery will now drive stronger demand and support prices that reflect the true cost of supply.”

None of us could have foreseen what happened this winter. Cost of supply became an irrelevance as Asian spot LNG prices went into orbit. From lows of around US$2/mmbtu in April, the JKM price soared north of US$32/mmbtu last week, with media reports of Trafigura purchasing a cargo from Total at US$39.3/mmbtu. Forget the hyperbole around Bitcoin, Tesla or even oil, Asian spot LNG has been the ticket to ride.

During summer 2020, a Wood Mackenzie survey of Asian buyers showed the vast majority predicting LNG prices below US$5/mmbtu for the winter. How did the industry call the market so wrong? And what will be the impact on prices through the rest of 2021? To get to the bottom of Asian spot LNG’s extraordinary rebound, I spoke to Rob Sims, WoodMac’s Global Head of LNG Short-Term Analytics.

Have you ever seen anything like this before? Not really. We’ve seen periods of rapid price rises before, and occasions where Asian spot LNG prices have overshot the economic price ceiling of oil parity, but usually only by a dollar. A JKM price of US$32/mmbtu would represent an unprecedented US$22/mmbtu premium over current oil parity, which we estimate today to be about US$9.5/mmbtu.

What’s caused this spike?

There are several market and fundamental factors at play – cold temperatures in North Asia (and hence stronger gas demand), supply constraints, a tight chartering market and bottlenecks at the Panama Canal. On top of this, it’s essential to stress that we are also witnessing an LNG liquidity crunch, with most spot volume already sold and hardwired to end users. It’s a cliché, but this is a perfect storm.

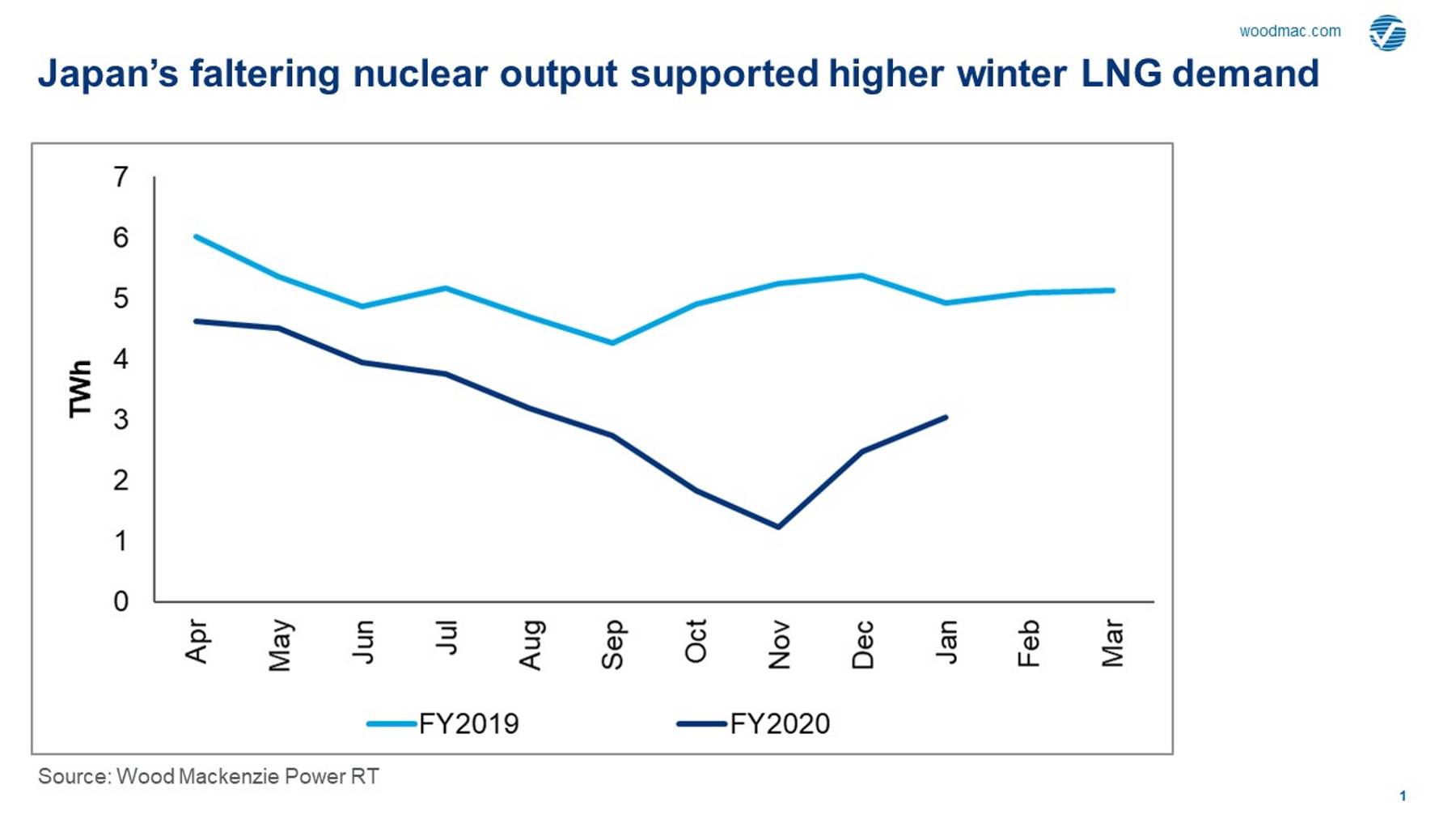

Temperatures across North Asia have been below average the past three weeks, spiking demand in the world’s biggest LNG markets – Japan, China and South Korea. All three had steadily run down stocks through late autumn and with early winter prices previously expected to remain soft, buyers were ill-prepared for the uptick in competition for cargoes that we saw from October onwards.

This created a demand surge for LNG cargoes ‘in the prompt’, that is, volume for immediate dispatch, or even already on the water. However, because of supply constraints at several liquefaction plants across Asia Pacific, this volume of spot simply was not available.

Why didn’t demand switch to other fuels?

Unfortunately for many generators, there are limits to available spare capacity. Part of the problem is that nuclear generation has been extremely poor in Japan through the compulsory shutdown of a number of units, while in South Korea, spare coal capacity has been reduced due to clean air policies. In both countries, oil generation has not been able to return fast enough to help with the demand spike.

{kind=link}

How are supply and shipping impacting price?

It hasn’t been plain sailing for suppliers, with an abnormally high number of disruptions in recent months. Enduring issues at Gorgon and Prelude FLNG combined with other outages in the Pacific and Middle East have reduced supply from projects close to major Asian demand centres. This has forced Asian buyers to source LNG further afield, with sellers diverting cargoes from Europe to benefit from soaring Asian prices.

US LNG neatly illustrates how shipping distances impact prices at the margin. US cargoes typically take around 20 days to reach North Asia via the Panama Canal. However, for vessels without pre-booked slots through the canal, we’ve seen an additional wait time of up to 10 days each way due to strong traffic and more stringent transit measures. As a result, many US cargoes are only reaching North Asia one month after loading – and taking longer to return to load the next cargo. Combined with little prompt supply availability for quick delivery to Asia, prices climb as buyers’ desperation increases. Economics 101.

But does this justify the prices we’ve seen?

Under normal circumstances, any price beyond oil party is difficult to justify. However, when the decision comes down to whether to keep the lights on, buyers have no choice but to absorb short-term losses. Current prices clearly reflect limited market liquidity and buyer desperation, and media reports of Kyushu Electric buying heel volumes left in tanks after vessels have discharged highlights this, as the utility scrambled for supplies to generate power as demand surged.

What role have traders played?

There is a lot of focus on the trading activity taking place in a period of such low liquidity. Through much of the past few weeks, only a single trader was active, bidding in the Platts MOC on consecutive days from the last cargo transacted at US$21.7/mmbtu on 6 January, until ultimately securing their cargo at US$39.3/mmbtu six days later, on 12 January. To illustrate the point further, another seller began offering a new cargo within a week at only US$20/mmbtu, which shows how low liquidity drives volatility. This will greatly impact the eventual monthly average JKM settled price, which is the basis of many paper trades used to hedge exposure for buyers and sellers in the market. Some may question how viable this paper trading mechanism is for hedging spot cargoes during periods of very low liquidity if the underlying commodity price can vary so much from one cargo to the next. However, perhaps the more salient point is that the trader was willing to pay that price for a cargo in order to fulfil its obligation to its customer, illustrating how the commodity traders are now in LNG for the long-haul.

Read also: Gas and LNG: why 2021 will be a defining year

Can these prices last?

Winter spot demand in Asia evaporates quickly in March-April, and forward prices are already falling quickly. It’s worth emphasising again that current prices are more a function of low liquidity, than of justifiable fundamentals, so volatility will remain until more cargoes are available in the spot market. At which point, prices will soften considerably and allow a reconnection firstly with Atlantic LNG prices, followed eventually by a relinking back to European TTF prices.

That said, low end-of-winter inventory levels will support prices through the coming shoulder period, reducing any risk of a price crash, and should continue to support prices through summer as storage is refilled across North Asia and Europe. At the same time, expectations of higher coal and European carbon prices, also partially driven by the current cold spell, provide headroom for higher European summer gas demand. What looked like a finely balanced summer market just a month ago, is looking increasingly tight.

What can we expect for LNG prices through the rest of 2021?

After the record lows of 2020, we’re going to see a stark difference over the next 12 months. We now expect Asian LNG spot to average US$7.6/mmbtu in 2021.

APAC Energy Buzz is a weekly blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.