Sign up today to get the best of our expert insight in your inbox.

What will define LNG’s three phases of market growth?

Price cyclicality to continue through the next decade

3 minute read

Simon Flowers

Chairman, Chief Analyst and author of The Edge

Simon Flowers

Chairman, Chief Analyst and author of The Edge

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Unlocking the potential of white hydrogen

-

The Edge

Is it time for a global climate bank?

-

The Edge

Are voters turning their backs on the EU’s 2030 climate objectives?

-

The Edge

Artificial intelligence and the future of energy

-

The Edge

A window opens for OPEC+ oil

-

The Edge

Why higher tariffs on Chinese EVs are a double-edged sword

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Unlocking the potential of white hydrogen

-

The Edge

Is it time for a global climate bank?

-

The Edge

Are voters turning their backs on the EU’s 2030 climate objectives?

-

The Edge

What will define LNG’s three phases of market growth?

-

The Edge

The coming low carbon energy system disruptors

-

The Edge

Could US data centres and AI shake up the global LNG market?

Massimo Di Odoardo

Vice President, Gas and LNG Research

Massimo Di Odoardo

Vice President, Gas and LNG Research

Massimo brings extensive knowledge of the entire gas industry value chain to his role leading gas and LNG consulting.

Latest articles by Massimo

-

The Edge

What will define LNG’s three phases of market growth?

-

The Edge

Could US data centres and AI shake up the global LNG market?

-

The Edge

Can emissions taxes decarbonise the LNG industry?

-

Opinion

Global gas industry in the 2050 net zero world

-

Featured

Gas and LNG 2024 outlook

-

The Edge

WoodMac’s Gas, LNG & Future of Energy conference – five key takeaways

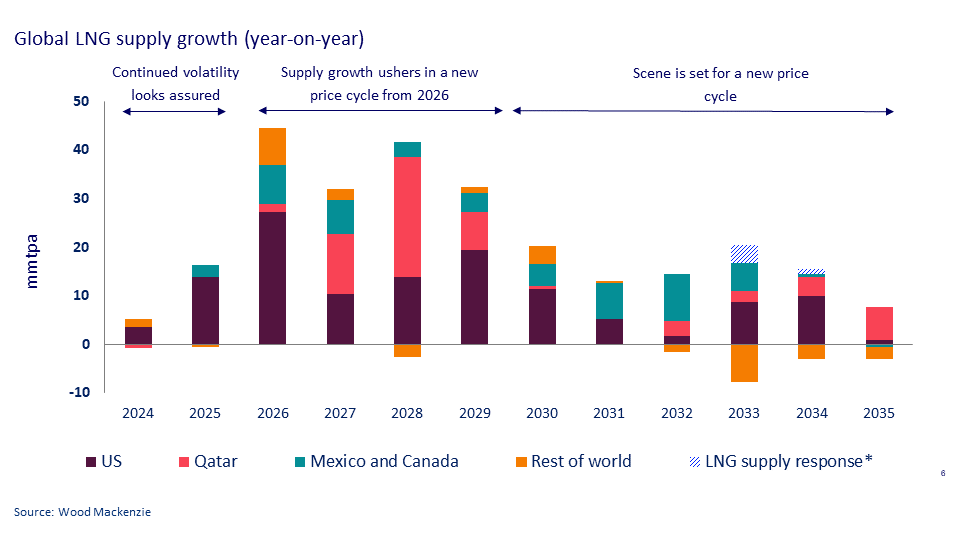

Our recently released Global gas strategic planning outlook (SPO) identifies three distinct phases of LNG market growth through the coming decade. First, continued market volatility over the next couple of years as limited supply growth amplifies risk. This is followed by a major wave of new supply, ushering in lower prices from 2026. Finally, as LNG supply growth slows, prices recover again before a new wave of LNG supply triggers another cycle of low prices in the early 2030s.

What are the drivers of each market cycle? How low will prices go? What are the risks to each phase of LNG market growth? The WoodMac team stress-tested our new outlook on the ground at this week’s Japan Energy Summit in Tokyo.

1. Continued short-term volatility looks assured

Softer prices since the start of this year have turbocharged demand in key Asian markets. China is the standout, with LNG imports rising 28% year to date. Consequently, TTF is up 40% over the past three months, trading close to US$11/mmbtu. As the market grapples with supply risks from Russia and maintenance at Norwegian fields, record European storage levels are keeping a lid on prices.

Looking ahead, rising prices are likely to provide some headwinds to near-term Asian demand growth, but the overall outlook remains positive, increasing competition between European and Asian buyers. Limited LNG supply growth and the loss of Russian pipeline imports into Europe via Ukraine set the scene for 2025 to be tighter still. The consensus is for price volatility.

What are the risks?

The pace of LNG supply growth and demand across Europe and Asia all provide upside and downside risks. Uncertainty over Russian gas and LNG exports further muddies the waters, making 2025 a difficult year to call.

2. Supply growth ushers in a new price cycle from 2026

The sheer volume of new LNG projects under construction will be cheered by buyers following the turbulence of the past few years. With supply growth expected to average above 38 mmtpa between 2026 and 2028, prices will undergo a structural shift as Europe is called upon to absorb more LNG than required, even with Asian demand shifting up through the gears. But with European prices still holding north of US$7/mmbtu – and Asian prices correspondingly above US$8/mmbtu – the coming supply wave is far from catastrophic for the market. Our view is the need for US cargo cancellations to balance the market remains limited.

What are the risks?

A muted demand response to lower prices across Asia would undoubtedly draw out the market imbalance. Conversely, supply risks can’t be ruled out. An anticipated escalation of Western sanctions on Russian LNG threatens to dent our overall supply growth story, increasing the potential for a stronger-for-longer market.

3. Asia sets the scene for a fresh price cycle in the 2030s.

Almost 200 mmtpa of LNG supply may be under construction, but demand from the emerging economies of Asia is only just getting started. We expect a pressing need for additional supply beyond the current wave.

The timing of this new supply now looks less assured. Delays in US LNG investments - due to the DOE’s pause in non-FTA approval - and the time required to develop projects elsewhere will result in supply growth slowing significantly beyond 2029. Markets will respond, with European prices once again above US$9/mmbtu in 2031.

This won’t last for long. A new round of investments through to 2027 across North America, the Middle East and elsewhere results in over 100 mmtpa of new FIDs, with this supply hitting the market in the first half of the 2030s. With European gas demand falling rapidly by this time and Chinese LNG demand peaking, weaker demand growth triggers another cycle of low prices.

What are the risks?

Much will ride on long-term Asian demand growth. Booming power demand and a push away from coal makes gas and renewables the obvious choice. But if LNG prices are too high, Asia's most price sensitive buyers could quickly return to coal. On the upside, delays or cancellations to the expansion of Central Asian and Russian pipeline gas into China would push Chinese LNG demand higher for longer.

Having spent the past week in Tokyo discussing the three phases of LNG market development, there’s broad consensus on the overall shape and duration of each. But the devil, as always, is in the detail. The timing of new supply, the scale of future Asian demand and the pace of the energy transition will each hold a casting vote.

{kind=link}

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.