Metals investment: the darkest hour is just before the dawn

As the world races towards 2030 and key decarbonisation targets approach, we look at how investment in metals and mining is central to achieving net zero

5 minute read

Julian Kettle

Vice Chairman of Metals and Mining

Julian Kettle

Vice Chairman of Metals and Mining

Latest articles by Julian

-

Opinion

Video | Data centres, copper and the power paradox

-

Opinion

Energy security shocks and coal’s role in a fragmented world

-

Opinion

Answering seven burning client questions on copper supply and demand

-

Opinion

Metals investment: the darkest hour is just before the dawn

-

Opinion

Ebook | How can the Super Region enable the energy transition?

-

The Edge

Can battery innovation accelerate the energy transition?

Things often seem at their worst just before they get better. In terms of meeting our net zero 2050 scenario, we’ve reached a watershed moment where the need for metals investment has become unquestionable. The challenge we face now is persuading investors, lenders, society and government that accelerated change is vital and the power for change is in their hands.

Complete the form at the top of the page to download your complimentary copy of the full presentation or read on for a summary of the key takeaways.

Low carbon power and sustainable transportation increase our exposure to metals

If we are to even come close to achieving global net zero targets, there needs to be a continued increase in renewable energy technologies and electric vehicles (EVs). But while governments continue to stimulate demand, it’s clear we’re falling way behind on targets. Incentives to improve new EV sales are critical to success and policies such as the USA’s tax credit system for buyers, or the purchase subsidies offered by Germany and France have created a positive upturn in sales. However, to meet the net zero 2050 scenario outlined in our energy transition outlook, the production of EVs needs to double by 2030. That means EVs need to represent around 60% of all cars by the same year.

These two factors present a distinctive challenge for the metals and mining industry. Without stable primary metals supply, simply put, there will be no energy transition. The drive to renewables is a huge draw on mine supply and whereas nuclear small modular reactors (SMRs) have the lowest physical and raw materials footprint for base load power, society is still wary about nuclear technology and buy-in remains low.

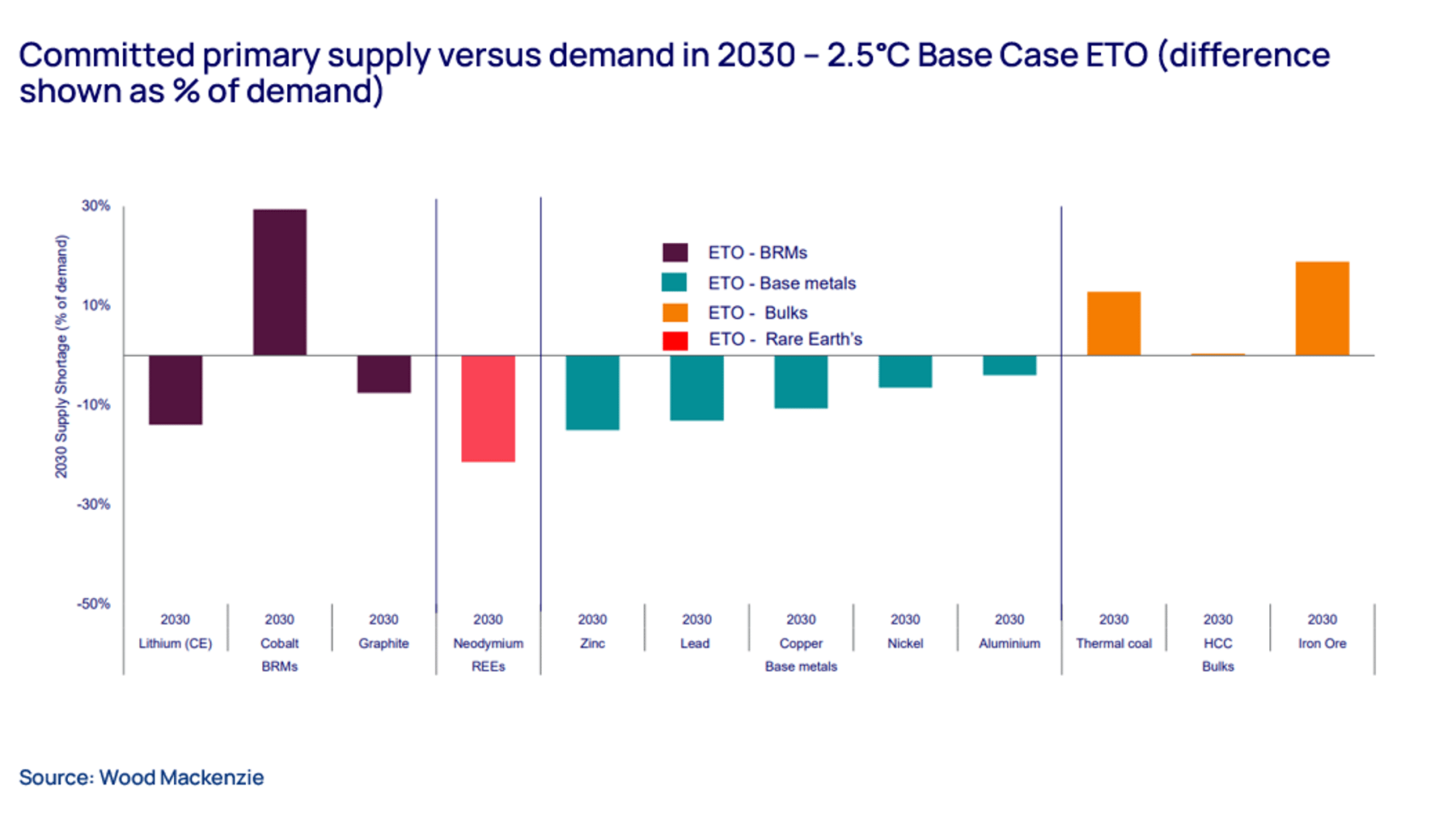

In fact, if we don’t see an investment of US$200bn in primary metals supply, demand destruction will likely occur. Lack of investment and slow lead times on metals development, together with a lag in the right skills and capabilities means that meeting our net zero 2050 scenario demand becomes an impossibility. Instead, it would take US$400bn of investment to turnaround the prediction that by 2030 committed primary supply versus demand will amount to our 2.5°C base case energy transition outlook (ETO).

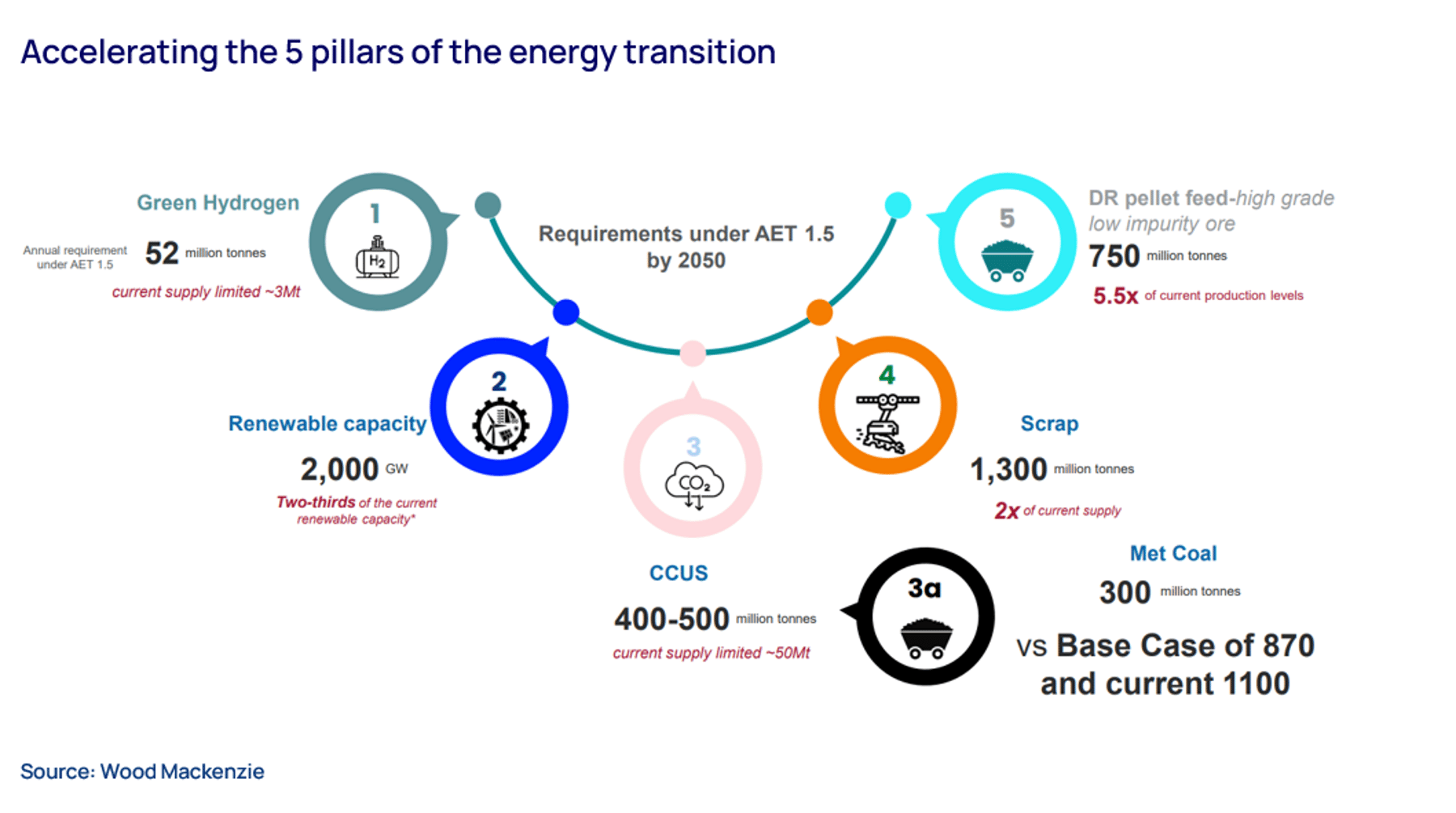

Accelerating the 5 pillars of the energy transition

Steel is an essential component for clean technologies such as EVs and wind turbines but is responsible for ~9% of global CO₂ and will cost US$1.5tn to decarbonise. To fully decarbonise the industry the output and deployment of renewables and scale carbon capture utilisation and storage (CCUS) will have to be vastly increased which, of course, requires more metals.

If we are going to achieve net zero, we need to align and boost momentum across the five pillars of the energy transition with a combined and concerted global effort.

- Policy: Whilst there are effective enablers, such as the COP framework, there are factors that are working against development. Carbon regimes are disparate and disjointed so we must see improved global alignment and a more consistent regulatory environment. The focus on critical minerals processing will diversify supply chains but restrict raw material availability leaving Europe and North America still reliant on imports over the next ten years.

- The circular economy: Societal attitudes to waste, a lower carbon footprint, and reduction in primary materials are all positive contributors, but issues with inefficient collection, degradation and recycling persist, as well as negative effects relating to costs, policy and society. Recycling will not materially change the need for essential primary investment in this or the next cycle.

- Technology: The demand for higher energy density is driving the utilisation of sodium-ion batteries that will be used in energy storage systems and also have the potential for use in affordable, low-range EVs. We can expect to see the rollout of smaller, lighter next generation-battery technology by some of the major players, like Samsung, Panasonic and CATL, around 2030.

- Primary supply: Current price signals do not support investment as some investors seek dividends over growth. However, demand growth is assured with more primary supply needed to account for grade decline and depletions and the lack of scrap material.

- Society: A paradigm shift from the societal assumption that mining and metals are a problem rather than a key contributor to achieving net zero is key. Industry successes should be widely promoted in order to mitigate misconceptions about minerals and metals extraction as well as instigate a reversal to the legacy of poor environmental performance.

Is copper the panacea for a successful energy transition?

We can’t argue that copper is fundamental to the energy transition in its role as the “metal of electrification”, but even though its place in renewable applications is integral, traditional uses for copper still currently dominate. However, even given its undisputed strong standing, copper is still vulnerable to the same high interest rates, higher yields and challenges presented by the macro environment that are limiting investment in other commodities.

The expectation for the industry to meet rising demand for copper is creating pressure to find a solution. Scrap copper will play a pivotal role in reducing the requirement for primary mine supply growth. Recycling copper from end-of-life clean energy technologies is expected to account for around 40% of total demand by 2033. We still need new supply to offset depletions, grade decline and demand growth but despite fairly high prices for copper, there are still possible and probable projects that are not being sanctioned, leaving significant capex requirements for primary mines to bridge the supply gap.

Final thoughts

To get to net zero, we must quickly scale-up resource extraction of metals and minerals to meet the growing demand for the clean technologies - EVs, batteries, solar PV panels, wind turbines - that will enable the energy transition; and that requires investment.

Learn more

Fill in the form at the top of the page to download your copy of the full presentation.

{kind=link}

{kind=link}