The Netherlands' gridlock: a cautionary tale for the US

The Netherlands has halted all interconnections for non-residential loads and generation as its grid has reached capacity – can the US avoid a similar scenario?

5 minute read

Grid capacity and infrastructure modernisation have not kept pace with the energy transition. As a result, years-long electricity generation interconnection delays are becoming the new norm in many regions of the world. But the Netherlands has emerged as an extreme case – and a cautionary tale. Since November 2022, Dutch grid operators have put an indefinite pause on the interconnection of not only generation, but non-residential loads.

This article draws on insight from our Grid Edge Service to delve into how this situation came about – and what the US can learn from it.

Three factors behind the Netherlands’ interconnection gridlock

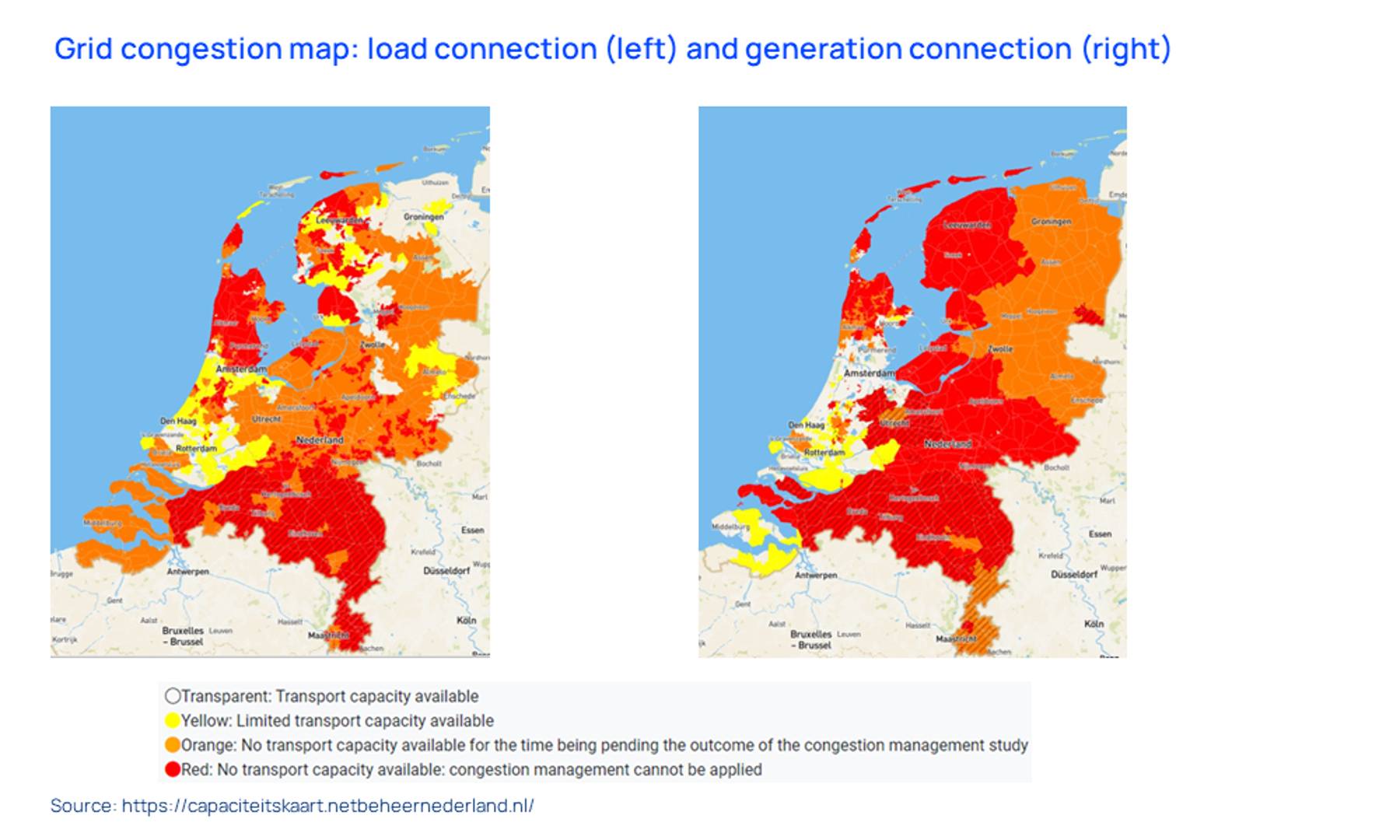

As of May 2023, more than 5,600 applications had accumulated in the load interconnection queue of Dutch network operators. 2,200 of these are new connection applications and the remainder are extensions to existing services.

Three main factors have led to the extreme gridlock that Dutch networks are facing:

1. Explosion in demand exceeded grid planners’ forecasts

The Netherlands’ aggressive sustainability targets, lucrative incentives for electrification and the EU’s ban on Russian natural gas have fueled a rapid increase in electricity demand. In 2022, the Dutch heat pump market passed one million installed units, with 57% year-over-year growth, as the country imposed a national ban on natural gas connections in new construction. Electric vehicle (EV) adoption has also tripled in the last 2.5 years.

2. Deadlock over nitrogen limits

To comply with EU regulations, the Netherlands must limit its nitrogen oxide (NOx) emissions. The country has one of the highest levels of NOx emissions in the EU, mainly driven by its expansive agriculture sector. As the country has hit its NOx limits, new construction projects – including those for grid expansion – have been unable to obtain permits due to their nitrogen emissions.

TenneT, the Dutch transmission operator, and three major distribution system operators (DSOs) – Alliander, Enexis and Stedin – had planned to invest €52 billion to double the size of the grid by 2030. However, 25% to 75% of the underlying projects are estimated to be paused indefinitely until the government negotiation with the agriculture sector over limiting NOx emission is settled.

3. An emphasis on rate reduction

Regulatory focus on efficiency and cost savings have eliminated financial incentives for grid operators to invest in grid infrastructure. When the regulator, Authority for Consumers and Markets (ACM), set the tariff for the 2017-2021 cycle, grid operators warned against insufficient investment in strengthening and expanding the grid. ACM rejected this plea, citing a lack of clear indication that the energy transition would impact the system within the regulatory period.

The grid capacity pressure has been growing for some time

While the impact on load interconnection is new, the limited headroom for generation interconnection has long been anticipated. In 2019, TenneT, along with Enexis (one of the Netherlands’ major DSOs), issued a warning on the very limited capacity for more solar in three northern provinces. Since then, congestion on the grid has spread to most other provinces.

According to our European Power Markets Outlook, renewable energy supply in the Netherlands rose 104% from 2019 to 2023, making up nearly 41% of total power production. Congestion charges – costs paid by the load that would not be paid if the transmission system was congestion-free – have increased 340% over this period.

{kind=link}

Is the US also at risk of gridlock?

The US is unlikely to face the extreme gridlock that the Netherlands has experienced. Although the drivers creating gridlock in the Netherlands have analogs in the US, there are important differences.

Like the Netherlands, congestion charges have been increasing across all regional transmission organisations in the US. Regions with the most additions of solar and wind generation have seen the largest increases. Mid-continent Independent System Operator (MISO), where renewable generation grew from 11% to 17% from 2019 to 2023, saw congestion costs rise by 293% over the same period. Renewables in MISO are expected to reach a similar share of net generation compared to the Netherlands’ grid by 2028, according to our forecasts.

On the demand growth, however, the US will see a more moderate rate from electrification than the Netherlands has experienced. States are still divided on banning natural gas connections in new buildings, and the widespread availability and low cost of natural gas lead to a modest forecasted annual growth of 7.1% in heat pump installations by 2030.

The number of EVs on the road in the US is expected to nearly quadruple approaching 2030, by contrast.

Properly designed rates and customer programs can alleviate local grid congestion issues while utilities work on a gradual increase of grid capacity.

Our latest outlook on the impact of electrification on US electricity demand predicts an average year-over-year growth in electrification demand of 21% from 2023 to 2030. This will threaten capacity inadequacy in states such as California, New York and Texas. The outlook shows how properly designed rates and customer programs can alleviate local grid congestion issues while utilities work on a gradual increase of grid capacity.

The US does not currently have constraints on NOx emissions from new construction projects. Nonetheless, obtaining siting permits, environmental studies and community hold-ups are imposing significant delays on grid infrastructure development. Permitting reforms underway in Congress are expected to mitigate this bottleneck, as is an expected FERC rule on regional transmission development. Fundamentally, however, permitting in the US remains a bottleneck, rather than the full-on blockade that it is in the Netherlands.

Finally, in diametric opposition to the Netherlands, utilities in the US are highly financially motivated to invest in grid infrastructure. The 7-12% rate of return on capital investment has been attractive enough for utilities to sell off unregulated assets, including high-quality renewable platforms, in order to plow more money into their regulated infrastructure.

Since 2018, 25 major investor-owned utilities have filed for a US$36.4 billion investment in the modernisation of their distribution grid with a 37% compound annual growth rate. The Department of Energy is also in the process of releasing US$13 billion from the Bipartisan Infrastructure Law to modernise and strengthen the physical infrastructure of the grid. This is expected to draw private investment of at least an equal amount.

Federal incentives, state commissions’ regulatory support and utilities’ use of capital to invest in grid infrastructure alleviate the risk of extreme gridlock in the US. Nevertheless, the Netherlands offers a cautionary tale. What begins as a generation interconnection bottleneck can morph into one that compromises one of the utilities’ core obligations: serving new load.

Interested in US grid edge developments?

A significant transformation is underway in the US distributed energy resource (DER) market. Our grid edge experts explored this topic in a recent webinar, delving into our five-year outlook.