Discuss your challenges with our solutions experts

North Sea Financial Flexibility Index: surviving – and thriving – in a volatile environment

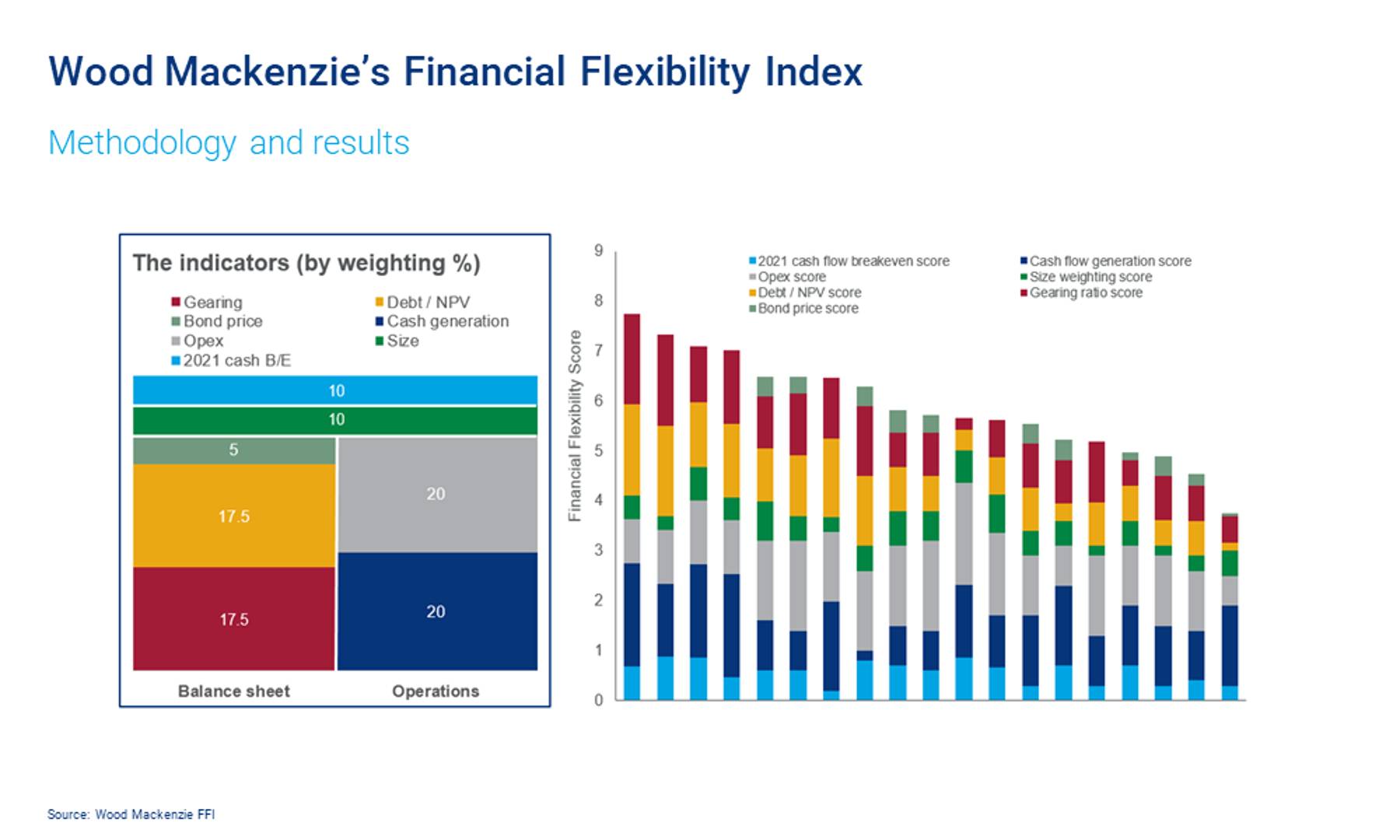

How we assess the financial flexibility of North Sea explorers and producers

1 minute read

Neivan Boroujerdi

Director, Corporate Research

Neivan Boroujerdi

Director, Corporate Research

Neivan leads Wood Mackenzie's global corporate NOC coverage.

Latest articles by Neivan

-

Opinion

Video | Venezuela in global portfolios: risk, restraint, and strategic optionality

-

The Edge

NOCs begin a new phase of upstream internationalisation

-

The Edge

The complexity of capital allocation for oil and gas companies

-

Opinion

Ten key considerations for oil & gas 2025 planning

-

Opinion

ADNOC doubles net hydrogen production through stake in ExxonMobil’s Baytown project

-

Opinion

ADNOC acquires stake in Rovuma LNG from Galp

With price volatility in the oil and gas industry looking increasingly endemic, financial flexibility is more crucial than ever. Wood Mackenzie has created its inaugural North Sea Financial Flexibility Index (FFI) to determine which companies are best placed to survive – and thrive – in the North Sea.

Our FFI ranks 19 North Sea-focused small and mid-caps and moves beyond the balance sheet to include Wood Mackenzie’s medium-term operational outlook. The analysis shows that financial flexibility varies widely across the region, ranging from cash-positive to deeply indebted. Overall, we were encouraged by the level of financial flexibility in the peer group.

Subscribers to Wood Mackenzie's North Sea upstream research can access the full 20-page report with detailed analysis of 19 E&Ps here.

Most companies can be self-funding in 2021, even if prices do not recover from current levels. The peer group requires oil prices just below US$40/bbl to cover cash spend but there are wide divergences in oil price leverage. Broadly, Norwegian players’ low costs protect against price downside but the UK’s lower taxes provide for better cash generation when prices are higher.

Companies with strong FFI scores are well-positioned to take advantage of the current dislocation in the M&A market, and some must do so to avert production and cash flow declines in the medium term. But not every company with a strong FFI score can act immediately: some face tighter cash flow as they invest in growth projects.

Timing in the investment cycle is always important and has a bearing on companies’ FFI score; but its importance should not be overplayed.

Those most highly ranked have typically made smart acquisition and divestiture decisions to achieve stability. Chrysaor has grown from very little to become the UK’s largest producer in three years through M&A. Buying high-margin production allowed rapid payback of debt. Cairn recently chose to monetise its Sangomar project in Senegal rather than leverage its balance sheet to fund the development.

And while there’s no one-size-fits-all solution for the North Sea’s independents, investment rates suggest consolidation could be the path toward a more balanced portfolio for the peer group.

{kind=link}

Talk to Neivan about our North Sea Financial Flexibility Index

Principal Upstream Analyst Neivan Boroujerdi is an expert in development costs, exploration and M&A. He’s a regular contributor of North Sea-focused corporate analysis content and is a co-author of the North Sea Financial Flexibility Index.

For details on how your data is used and stored, see our Privacy Notice.

Neivan Boroujerdi, Principal Analyst, North Sea Upstream