Power system flexibility key to Europe's net zero targets

Energy storage and gas peakers; what will be the winning flexibility asset?

1 minute read

Find out why flexibility and storage are key as Great Britain (GB), Germany, France, Italy and Spain transition to a Variable Renewable Energy System made up of wind and solar power. Get the key takeaways below, and fill out the form on this page for the Europe power system flexibility: The essential ingredient for decarbonisation (Part 2) report brochure.

A combination of wind and solar power, otherwise known as Variable Renewable Energy (VRE), could make up the largest share of power capacity throughout Europe’s major markets – The United Kingdom, Germany, France, Italy and Spain – as early as 2023.

This is the result of increased government subsidies, falling technology costs and reduced investment risk. Now the majority of VRE volumes are being deployed through government renewables auctions with an attractive risk/return profile, but with little or no value placed on flexibility. The priority is to push renewables into the system first, and deal with the consequences later.

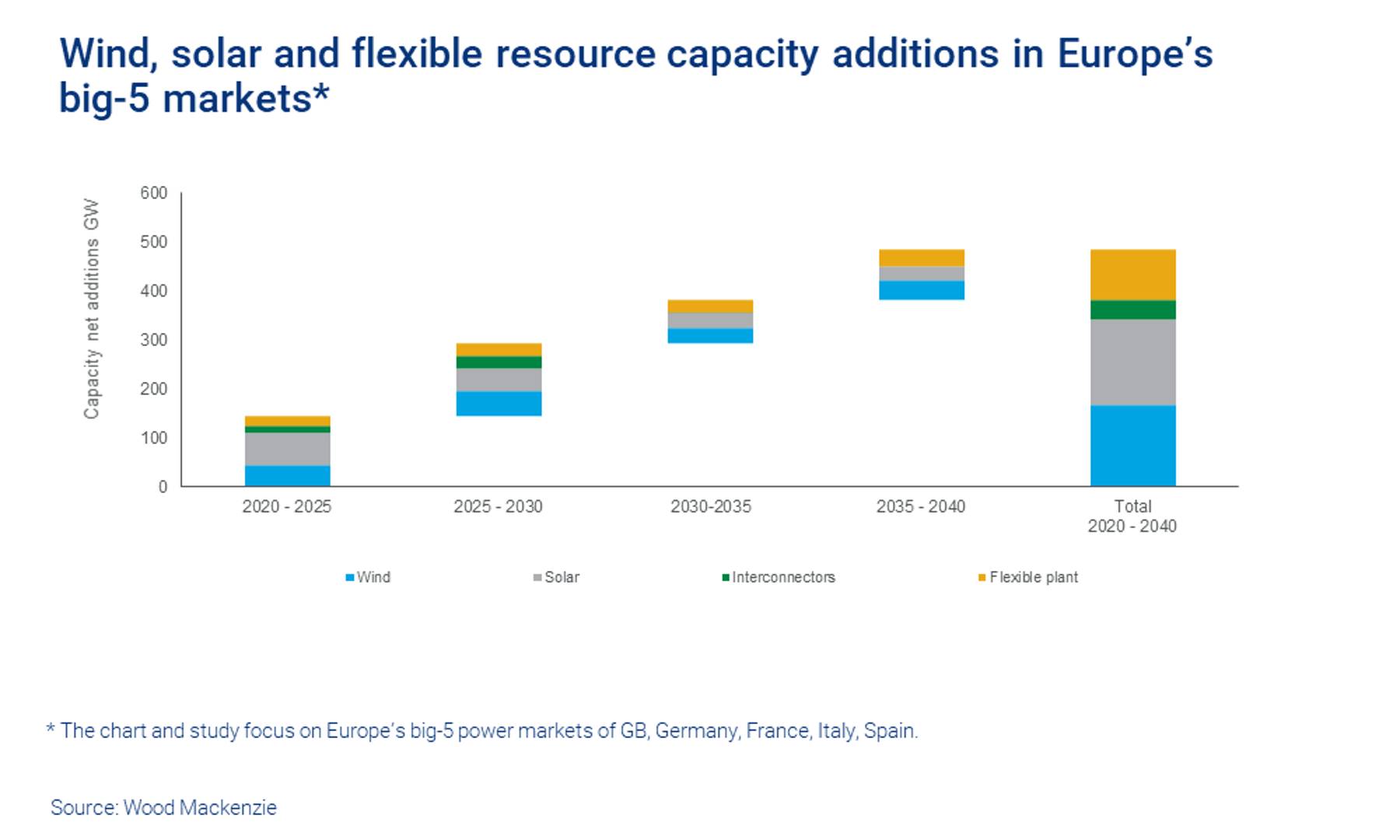

Auctions will continue to deliver strong VRE growth, with an increasing portion of merchant projects outside this, that will be more exposed to power market prices and therefore have more of an incentive to mitigate the risks inherent in a non-dispatchable fleet, with flexible resources. We expect the additional 169 GW of wind and 172 GW of solar to put unprecedented constraints on current system assets and market mechanisms.

Conventional plants are on their way out

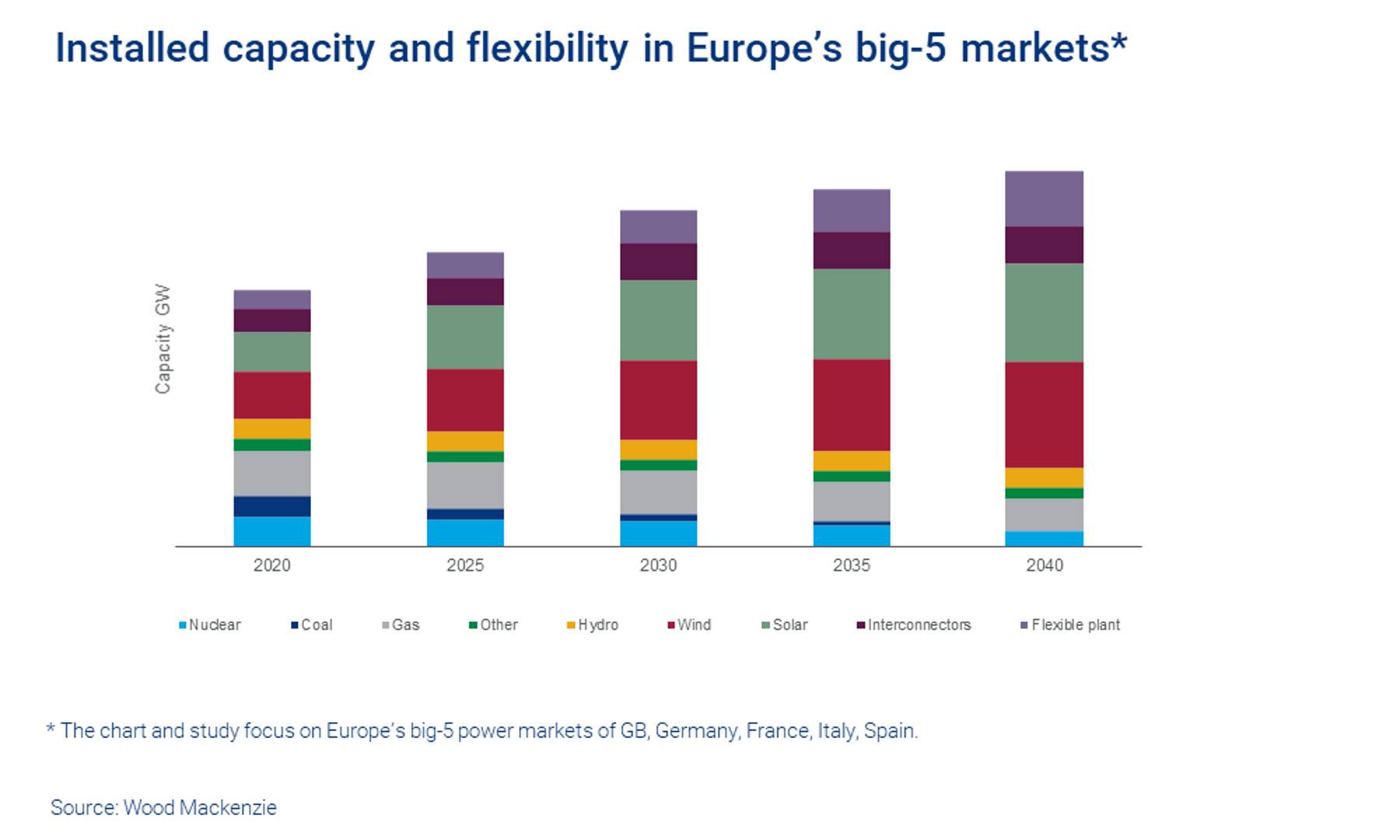

Coal is the biggest loser in this supply mix, only hanging on in Germany until 2038. The nuclear fleet shrinks in half by 2040, due to retirements and limited new build struggling with increasing costs, safety requirements and weakened government support. Large gas-fired capacity also declines – CCGT (Combined Cycle Gas Turbine Plant) fleet capacity falls from 87 GW in 2020 to 46 GW by 2040. Across our target markets, CCGTs utilisation factors are decimated, with a 60 % reduction by 2030. Some increases are expected in Germany and Italy in order to balance systems with along with other dispatchable options.

This creates the supply and demand balancing challenge – the need for new system flexibility

A system need for new flexible resource will manifest itself in various forms, such as high levels of renewables curtailments, grid connection delays or uneconomical connections due to capacity shortages, low and negative power prices, power quality reduction or worse, risk to security of supply or ‘blackout risk’.

Markets will need new sources of flexibility at different rates, some sooner than others. GB for instance as an island with low levels of interconnection, an accelerated coal decommissioning programme and the biggest offshore wind fleet in Europe, needs flexibility sooner than its European neighbours who benefit from a mammoth, resilient and diverse fully interconnected power system.

The system need for flexible resource is already apparent. This becomes more apparent the further out we go.

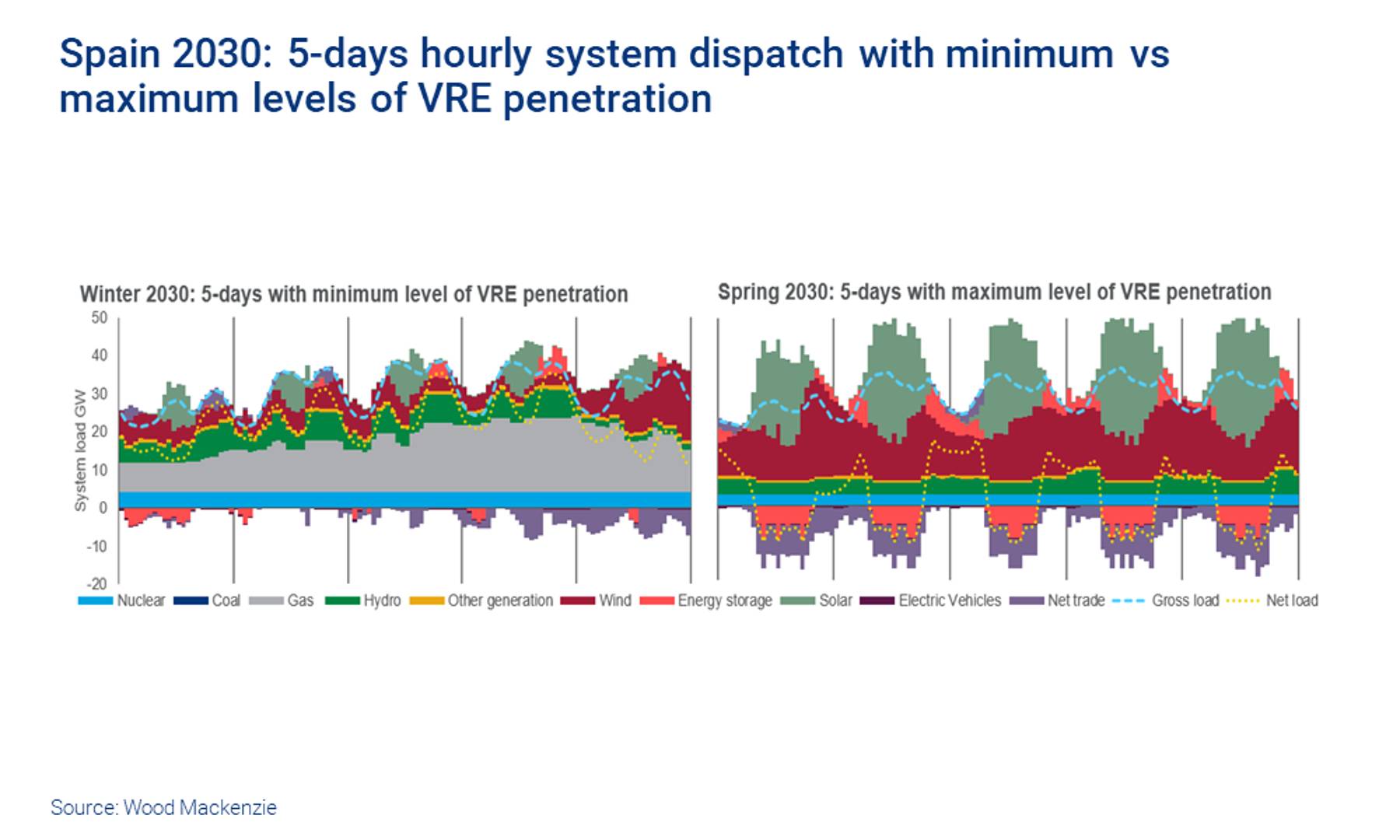

Look at the hourly power supply mix in Spain by 2030. On low VRE days the gas fleet continues to be the primary source of power, and it provides much needed flexibility. On high VRE days, with lots of wind and solar on the system, the net load (the dotted yellow line) is pushed into negative territory. That means there is more wind and solar being generated than system demand. This means you either curtail power from these resources, or use other sources of flexibility to manage the imbalance, such as exporting power through an interconnector to another power market, or charging a large, or lots of smaller batteries. It is also important to mention that at times of high VRE, with little conventional plant running i.e. huge volumes of spinning turbines on the system, the system loses inertia and becomes unstable.

With conventional assets in decline, and electrification taking hold throughout the economy, pump storage, interconnectors, gas peakers and energy storage become more critical. Without them, curtailment, network constraints, renewables ramping, low inertia, low and negative net load, and system critical issues that increasingly occur due to the VRE levels on the system by 2030 would become unmanageable. This flexibility asset mix grows from 122 GW in 2020 to 205 GW by 2030 and 265 GW by 2040.

{kind=link}

{kind=link}

{kind=link}

The flexible plant in this mix is made up of pump storage, gas peakers and energy storage

The sheer scale of capex required for new pump storage, against a fully merchant risk business model, and more stringent environmental planning legislation, means we do not see any new build unless a purpose-built revenue based and construction planning supporting policy is introduced. That leaves us with gas peakers and energy storage, which will fight for market share.

Gas peakers offer critical flexibility

Modern systems are being refined to meet the new flexibility challenge. They can ramp up from warm to full output in a couple of minutes, are increasingly efficient at part loading, not to mention they have unlimited duration where there’s a reliable gas supply.

Until recent years, it was expected that gas peakers would dominate this new flexible asset base, but with the arrival of energy storage, the future for new peaker plants is more uncertain.

Energy storage is coming to a market near you

Europe has been a lot slower to embrace storage (basically lithium-ion battery energy storage systems) than its North American and APAC counterparts. This is partly down to the region’s reluctance to invest in new technology, especially with a glut of conventional capacity already on the system. A key reason is that a regulatory regime that completely unbundles the power market value chain. For instance, generation and network ownership and operation are treated separately, for good reason. This makes it overly complex for an asset which relies on revenues from all parts of this value chain, compared to other less unbundled markets such as those in the US.

More generally, policymakers and industry stakeholders have not seen the urgency of the flexibility issue, which could be problematic. This is set to change. With a push from the European Commission, now on the road to net-zero emissions, storage technology costs plummeting and VRE taking over the system, storage across all segments will finally take off. How much energy storage can be deployed?

Pitted against gas peakers, energy storage is duration-limited, a major downfall. In Europe, most energy storage systems being deployed on the grid are one-hour systems. Compare this to a peaker, which has unlimited duration potential.

Energy storage could hold the key as it can import power when it is extremely low, or better still, negative. This is bolstered with rapid technology cost declines, similar to what we have seen in the wind and solar industry. Compare this to gas peakers, which face increasing carbon and fuel costs, limited potential for system cost reduction and the general net-zero trajectory. Gas peakers will certainly have their work cut out.

Gas peakers peak by 2030, as energy storage takes over the flexible asset build-out

Given these dynamics, we expect gas peakers and energy storage to compete head to head over the next decade, but by 2030, energy storage will be so competitive on cost, so complimentary to a power system that will be primarily renewables-based, that it takes over flexible asset build. Energy storage doesn’t just win out against peakers, but against pump storage and interconnectors too. We expect energy storage in these five markets alone could grow from 3 GW today, to 26 GW in 2030, and 89 GW by 2040

It would be advisable for policymakers, market participants and investors to embrace energy storage today to enable a smooth transition to this new flexible friend.

The speed at which policymakers wish to decarbonise the power market will determine how quickly the energy storage transition will take.

We have carried out detailed system cost analysis and hourly power dispatch modelling out to 2040 to show how this energy storage and gas peaker story pans out. Fill in the form on the page to learn more.