Get Ed Crooks' Energy Pulse in your inbox every week

US tech companies help clear a path for solar power

Corporate procurement plays a vital role in the growth of renewable energy in the US

8 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

-

Opinion

Carbon capture continues to grow, despite challenges

“When the modern corporation acquires power over markets, power in the community, power over the state and power over belief, it is a political instrument, different in degree but not in kind from the state itself.” John Kenneth Galbraith’s view of the power of corporations may not always hold true, but it is certainly relevant to the energy industry.

In the US, corporate decisions on energy purchases have been key factors driving the growth of renewables. Companies in a range of industries including technology, retailing, real estate and logistics have been signing contracts for wind and solar projects, either on-site at their own properties or off-site at separate locations. Wood Mackenzie data suggest that the significance of corporate purchases for the overall growth of renewable energy in the US is increasing.

A useful snapshot of corporate purchases of solar power in the US was provided last week by the Solar Energy Industries Association, in its latest annual Solar Means Business report. It shows that Meta, the owner of Facebook, has the most solar capacity installed of any US company, at about 3.6 gigawatts, followed by Amazon, Apple, Walmart and Microsoft.

On Wood Mackenzie’s data, corporate procurement accounts for 18% of all the utility-scale solar capacity installed in the US. Meta’s purchasing alone accounts for about 4% of installed US utility-scale solar.

Up until 2015, corporate solar purchases were almost entirely for on-site installations. Since then, there has been a surge in off-site projects, used to offset the company’s electricity purchases from the grid. Those projects can use a variety of models, including Virtual Net Metering, Physical or Virtual Power Purchase Agreements (PPAs), and green tariffs.

Over the past five years, on-site solar capacity in the US has been increasing at an average rate of 3% a year, but that has been far outpaced by the growth of off-site installations, and that pace did not slow during the pandemic. Almost 70% of all off-site corporate solar in the US has been brought online in the last two and a half years. Off-site projects accounted for about 75% of all the new commercial solar capacity installed in the US in 2021.

Companies have been pursuing these purchases for two main reasons: the falling cost of solar power, and their goals for emissions and other environmental metrics. The price for electricity from utility-scale off-site solar systems has dropped into the range $16 – $35 per megawatt hour, according to SEIA and Wood Mackenzie data, making them highly competitive with any other form of generation. While costs for solar power have increased in the past two years, the costs for fossil fuel generation have generally risen much further.

At the same time, growing numbers of companies have set environmental targets, including goals for having net zero greenhouse gas emissions or using renewables to meet 100% of their energy needs . Meta, for example, achieved its 2020 goal of reaching 100% renewable energy, including off-site wind and solar projects connected to the grids used by its data centres. It is now working towards net zero emissions, for its entire business including its supply chain and its customers’ use of its products, by 2030.

Other tech companies also have ambitious net zero emissions goals. Apple wants to be carbon neutral by 2030 and Microsoft is aiming to be carbon negative the same year, while Amazon is targeting net zero by 2040. In the SEIA’s list of the top 25 corporate purchasers of solar power, 18 have set goals for carbon neutrality or using 100% renewable energy.

This year there has been a sharp slowdown in solar installations in the US, hit by a series of problems including the Department of Commerce’s anti-dumping action on solar cells and modules, a surge in costs for both materials and labor, equipment availability issues and interconnection delays. A year ago, Wood Mackenzie projected that the US solar industry could add more than 20GW of capacity in 2022. It now looks likely to be only about 16 GW.

Over the course of the next 18 months or so, however, those problems will ease, and US solar installations are expected to start to rebound. By 2027, annual solar installations in the US could be running at about three times this year’s level, Wood Mackenzie forecasts.

The Inflation Reduction Act, signed into law in August, has given a huge boost to prospects for solar investment in the US. Wood Mackenzie projects that over the next five years, the expanded and extended tax credits in the act will increase on-site commercial solar deployment by 24%, relative to what would have happened if it had not passed, while utility-scale deployment will be 51% higher.

Companies will play an increasingly influential role in that growth. Out of total solar capacity of about 103 GW contracted in the US for 2022-25, corporate procurement accounts for 27%. Over time, Amazon looks likely to regain top slot for solar capacity from Meta. It has about 7.2 GW of additional solar capacity contracted, compared to Meta’s 2.8 GW.

Sylvia Leyva Martinez, Wood Mackenzie’s senior analyst for North America utility-scale solar, highlights another trend that will help drive increased corporate purchasing of renewable power: the growing use of utilities as intermediaries. In regulated markets, where customers do not have a choice of electricity supplier and cannot sign contracts directly with renewable energy projects, they have to use a green tariff. Customers can agree to buy renewable power at a fixed price from the utility, which matches the sale with renewable generation from its own assets or from independent producers.

As Meta points out, “the process of creating green tariffs can be time intensive,” as new tariffs often take months to negotiate. But once the tariff structure is in place, it is available for any customers that want to make use of it. By acting as trailblazers, the big tech companies that are leading the way on corporate procurement of renewables are not only having a direct impact on the market, but also creating paths that other companies will follow.

(For a view on how corporate procurement is changing the electricity industry in Asia, this piece on “the power of the PPA” by Kyeongho Lee, our principal analyst for Asia Pacific power and renewables, is essential reading.)

In brief

Ministers from the OPEC+ countries held their regular online meeting on Sunday, and as expected agreed to leave their production limits unchanged. The decision reaffirmed the 2 million barrels per day output reduction announced in October, which provoked an outraged response in Washington.

The ministers tried to play down suggestions that the production cut, which took effect last month, had been intended to hurt Democrats in the US midterm elections on November 8. The official statement from Sunday’s meeting noted that the cut “was purely driven by market considerations and recognised in retrospect by the market participants to have been the necessary and the right course of action towards stabilising global oil markets.” The next full meeting of the OPEC+ group ministers will be on June 4 2023.

In the first few hours after the markets opened on Monday morning, oil was trading slightly higher, with Brent crude up about 60 cents at around $86.20. The $60 a barrel price cap on sales on Russian-origin crude agreed by the Group of 7 countries and their allies was scheduled to come into effect on Monday “or very soon thereafter”.

California is still debating proposed changes to its net metering rules for domestic solar systems, which would make their economics significantly less attractive. The California Public Utilities Commission last month released its revised Proposed Decision on the tariffs, commonly referred to as “NEM 3.0”. Michelle Davis, Wood Mackenzie’s principal analyst for US distributed solar, described the new proposal as “an undeniable improvement for the distributed solar industry.” However, she added: “Even as the industry adapts, it is undeniable that NEM 3.0 will cause some level of destruction.”

Other views

Simon Flowers — How Europe’s energy crisis changes the LNG market

Sarah O’Connor — Britain is two countries when it comes to energy

John Kemp — Is the US shale oil revolution over?

Émile P. Torres — What “longtermism” gets wrong about climate change

Jessica McKenzie — The geothermal moonshot

Quote of the week

“Ukraine’s nuclear power plants served three purposes… in the invasion plan: to function as reliable shelters for Russia’s troops and military personnel, equipment, command posts and ammunition depots; to gain control over Ukraine’s energy system, because nuclear power plants are responsible for generating more than 60% of Ukraine’s electricity; and to provide the option to obtain leverage for blackmailing European countries with the risk of radiation pollution as a result of possible accidents at nuclear power plants if they attempted to intervene.” — The authors of a Royal United Services Institute study on lessons from the first phase of Russia’s war in Ukraine explained the strategic significance of the country’s nuclear power plants.

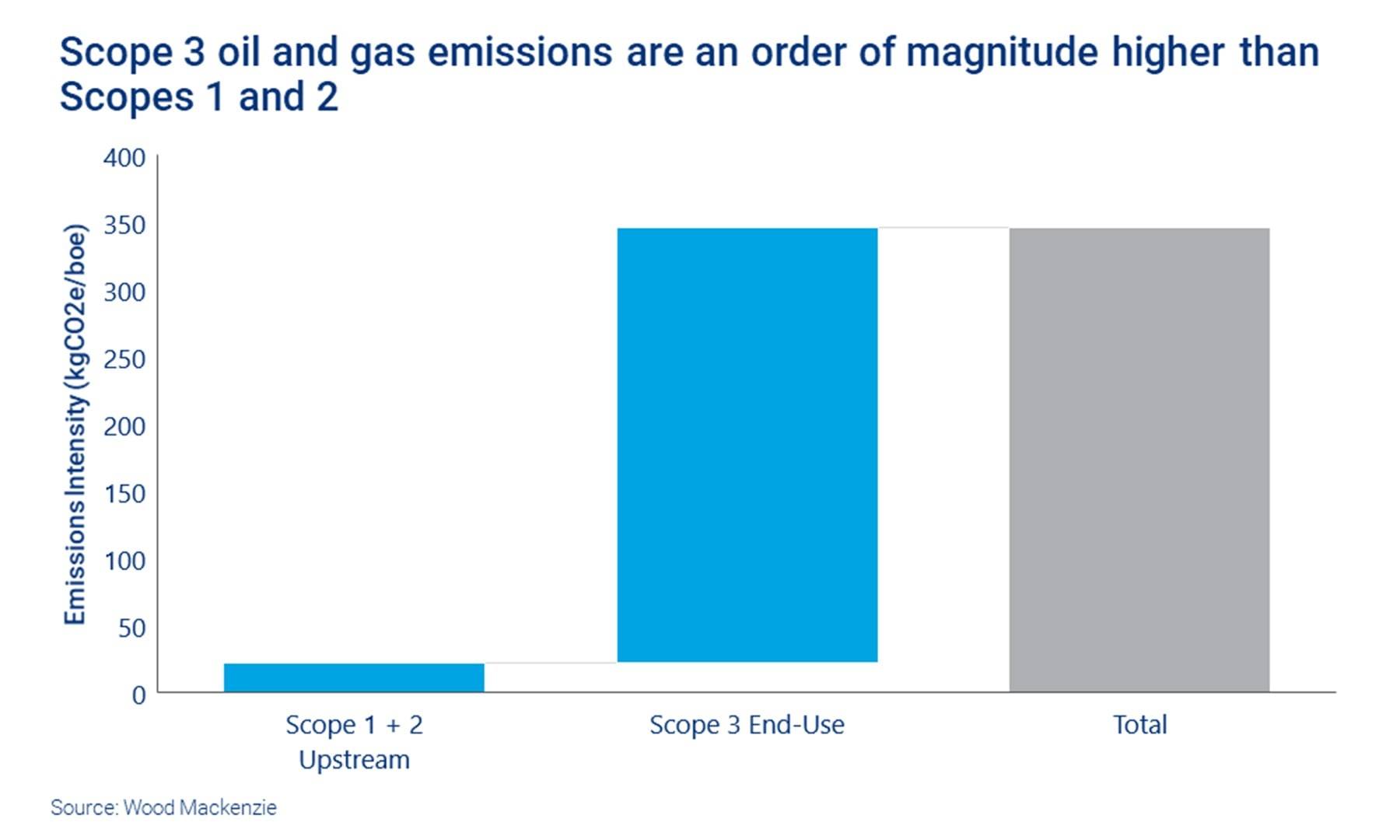

Chart of the week

This comes from an opinion column by Stewart Williams, our vice-president for carbon research, asking the question: Is gas the green choice? It shows a breakdown of the different types of emissions from the oil and gas industry: Scope 1, from the industry’s operations, Scope 2, from its purchased energy, and Scope 3, from its supply chain and the use of its products.

The message is very clear: Scope 1 and 2 emissions are smaller by an order of magnitude than Scope 3 emissions. That fact raises some challenging questions for the oil and gas industry. Scope 1 and 2 emissions are to a large degree under the companies’ control, and can be managed using a range of technologies such as renewable energy for power supplies and equipment to prevent methane leakage. Scope 3 emissions are more difficult. The main routes to reducing them are either simply producing and selling less oil and gas, or using carbon capture, including direct air capture and nature-based solutions such as reforestation, to cut emissions on a net basis. An important point about natural gas in this context is that its Scope 3 emissions can be much lower than for coal or liquid fuels.

{kind=link}