Interested in learning more about our gas & LNG solutions?

How Europe’s energy crisis changes the LNG market

High prices, gas demand destruction and a global LNG supply boom

4 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Massive supply disruption in Europe and soaring global prices. No other commodity has faced the extreme challenges of global gas since Russia’s invasion of Ukraine. I caught up with Kateryna Filippenko, Director, Global Gas Research, to find out her team’s latest views on the market.

How does this winter in Europe look?

Better than we could have hoped for a few months ago in some respects, but it’s been at a severe cost. Extremely high prices throughout the year have stretched affordability for consumers and weakened the economy.

High prices have hit demand hard (down 22% for non-power sectors year-on-year July to October) and pulled in LNG supplies destined for Asia. This rebalancing, combined with warm weather in recent weeks, has kept storage 93% full – well up on the 80% ‘normal’ for early December. Cold weather is now the principal risk this winter, but we think there should be enough gas, barring an exceptionally long and cold winter.

That doesn’t mean Europe is out of the woods. Absent Russia gas, the market faces three more years of elevated prices and the repeat-cycle of refilling storage with alternative sources of imported pipe gas and LNG in the summer, managing demand through the year and hoping for the best each winter. It’s only in calendar 2026 that relief finally arrives with sizeable new supplies of LNG. Until then, there will be a compounding effect of high prices on consumers and economic growth.

Is there enough investment in new supply?

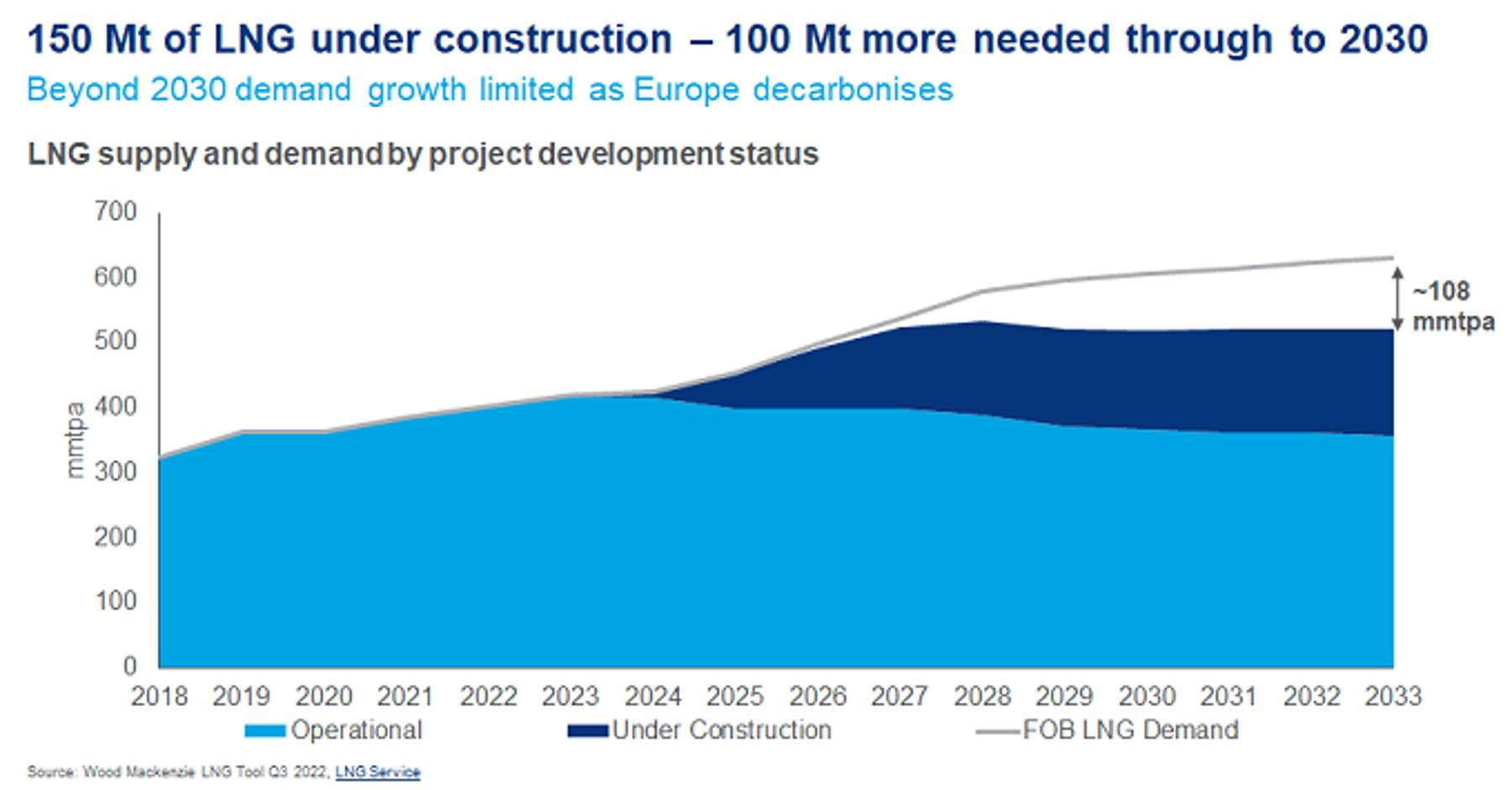

We’re at the early stages of an LNG boom cycle. We expect global supply to increase by 45% by 2030 (see chart). In the last two years, new projects that will deliver 78 mmtpa of supply have been sanctioned; and we expect another 90 mmtpa from 2023 to 2025

{kind=link}

Huge additional investment is required – around US$400 billion – on liquefaction, shipping and regasification alone (including projects already sanctioned) and multiples more on upstream gas. Two-thirds of the nearly US$200 billion liquefaction spend is destined for plants in North America.

Will the market get back to normal after 2025?

The new volumes will relieve the pressure on the system and bring prices down from today’s exceptional levels. There is even some risk of oversupply that could result in very weak prices temporarily as projects ramp up between 2027 and 2029.

The investment in gas infrastructure getting underway across Europe will be critical. New regas capacity and interconnectors should ease the bottlenecks exposed this year and help gas to flow to the right places at the right time.

With Europe increasingly dependent on imported LNG in gas and power markets, price volatility is here to stay. Europe will continue to compete with Asia for LNG supply at times of high demand.

We expect European gas prices (TTF) to settle around US$9 to US10/mmbtu, structurally higher than before the war, to reflect these factors.

Is LNG still a longer-term growth story?

Yes. We still think gas and LNG will play a critical role in achieving net zero by 2050 by displacing higher carbon-intensity coal in developing economies. But that will only happen if LNG is more affordable than it is today – gas prices must come down.

We expect LNG demand to grow by 200 mmtpa, or 50%, over the next 10 years. Asia accounts for two-thirds, much of it in China and India; as well as in Pakistan and Bangladesh where domestic gas supply is declining. In contrast, LNG imports to mature Asian gas markets such as Japan and South Korea are set to decline as they diversify their energy mix towards renewables and nuclear.

Europe is still a hot market with LNG demand jumping 60% in 2022 and set for a further 25% growth by 2028. After that though, in our latest view, demand declines quite steeply through the 2030s as the EU accelerates its push to low-carbon energy. There is further downside risk if the EU’s policy achieves its ambitious REPowerEU goals.

Will buyers sign long-term contracts?

There is still an appetite in some quarters as QatarEnergy’s recent 27-year deal to supply 4 mmtpa of LNG to China's Sinopec showed. And just this week, QatarEnergy and ConocoPhillips announced a deal to sell 2 mmtpa over 15 years to deliver into Germany.

While many independent LNG developers rely on long-term contracts to underpin financing for new projects, buyers are increasingly wary of committing to traditional long-term contracts because of the uncertainty around the resilience of gas demand beyond the mid-2030s. The trend is particularly acute in Europe with EU policy aiming to minimise gas consumption in the medium term. Utilities typically won’t want to commit to contracts longer than 15 years.

That’s an opportunity for LNG aggregators with a diversified international trading portfolio business. They can take the risk of the longer duration contracts and help finance the new projects. But for taking the risk, the aggregators will expect a return – higher-priced resale LNG.