Can upstream deliver the oil and gas supply the world needs?

Assessing the risks in a strong investment upcycle

3 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Fraser McKay

Head of Upstream Analysis

Fraser McKay

Head of Upstream Analysis

As head of upstream research, Fraser maximises the quality and impact of our analysis of key global upstream themes.

View Fraser McKay's full profile

Ian Thom

Research Director, Upstream

Ian Thom

Research Director, Upstream

Ian brings 18 years of experience to his role as head of regional analysis for Europe, Russian, Caspian and Africa

Latest articles by Ian

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

The unstoppable rise of Africa’s upstream independents

-

Featured

Upstream-oil-gas-2026-outlook

-

Opinion

Video | Global upstream update: winter 2025

-

Opinion

Revitalisation meets frontier exploration in West Africa’s twin-track energy future

-

Opinion

Video | Lens Emissions: Africa’s oil – legacy fields vs low-carbon future

Upstream oil and gas is enjoying a new lease of life. But with investment spend well below past highs, is the industry investing enough to fulfil its critical role of delivering enough supply to meet the rise in demand we expect over the next decade? I asked our Upstream experts, Fraser McKay and Ian Thom, who addressed this very question in our July Horizons.

Where is upstream in the investment cycle?

In the third year of a new upcycle. Global development spend will be around US$490 billion in 2023, up from the 2020 low of US$370 billion (in 2023 terms). Recovering demand, firmer prices, availability of cash flow and a pent-up pipeline of opportunities that had been shelved or reworked during the pandemic are fuelling the rise. Even so, the level of investment today is only just over half the average of US$800 billion (in 2023 terms) spent each year from 2010 to 2014.

Which regions are attracting additional investment?

There are three main hot spots: the US Lower 48, where the rig count has more than doubled in three years; the Middle East, particularly in Saudi Arabia and Abu Dhabi where major developments are underway; and deepwater plays, mainly in Brazil, Guyana, West Africa and the East Mediterranean.

Is current spend enough?

Very nearly. WoodMac has never bought into the idea that the world is headed inevitably for an oil supply crunch later this decade. In fact, growth in global liquids supply has kept up with rising demand since the middle of the last decade despite structurally lower prices. The early 2010s’ peak inefficiency remains a poor reference point for spending requirements.

Non-OPEC liquids supply has increased by 5 million b/d, or 10%, since 2015, capturing the bulk of contestable demand in the process. We expect non-OPEC to maintain its market share for some years to come. Global gas supply, too, has continued to rise, driven by the US LNG export bonanza, with Canada and Australia also prominent.

How has supply grown despite lower spend?

The industry has drastically reduced costs. The emergence of low-cost conventional, tight oil and deepwater sources has been important, out-competing the more complex projects and higher-cost resource themes that were the industry’s focus earlier in the century.

But upstream essentially has re-invented itself since 2015. Then, the industry’s reflex response when the oil price crashed was to cut costs and spend to preserve cash. Through time came strategic repositioning: gold-plated developments rescoped into smaller, simpler or more modular projects with swifter execution; a focus on short-cycle, low-cost, low-carbon exploration prospects and projects; and strict capital discipline and portfolio management.

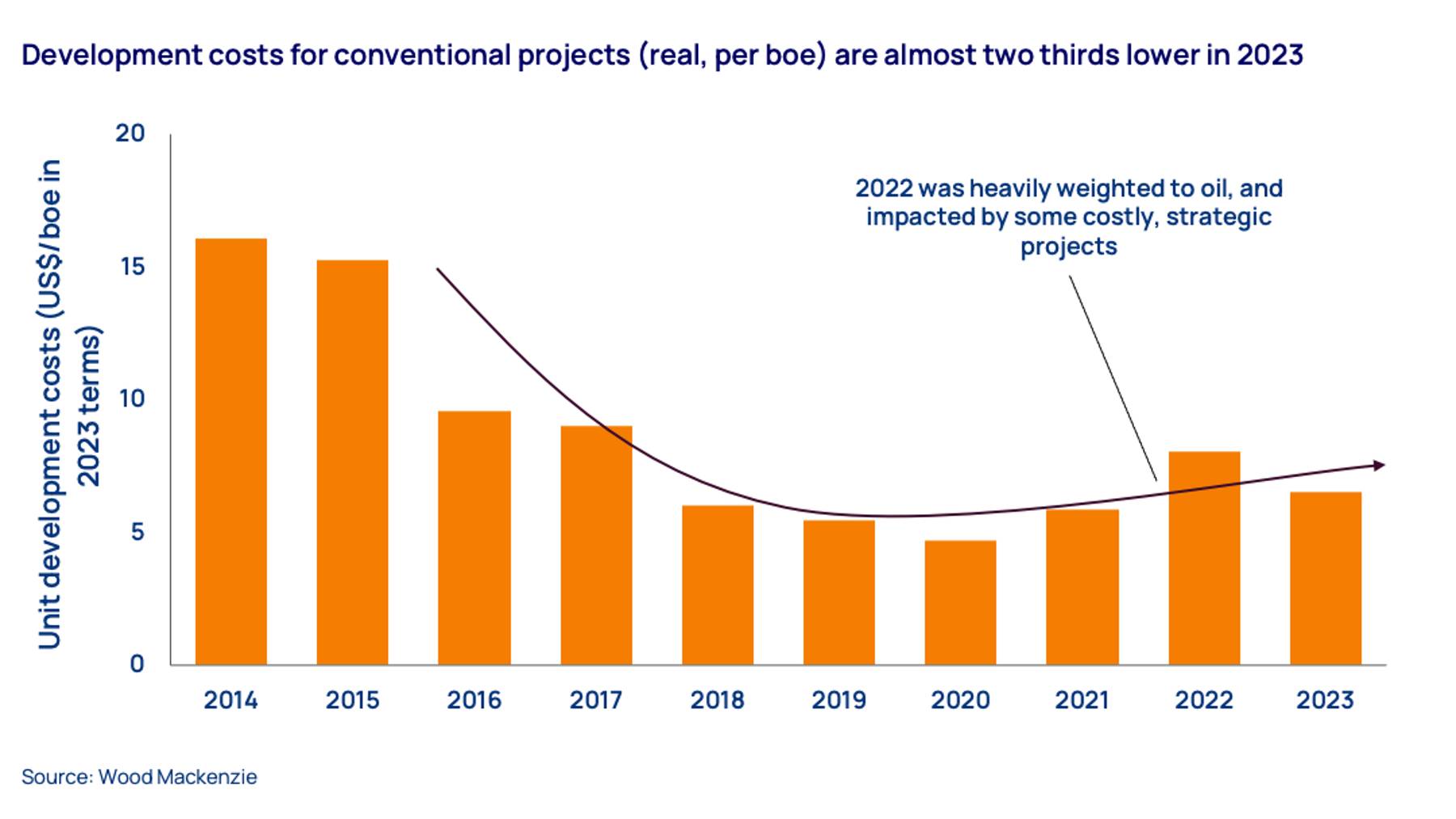

The result? Development costs are two-thirds lower than 2014 (in 2023 terms) on a per barrel of oil equivalent basis for new conventional projects, while tight oil wells are three times as productive per unit of capex. The industry is now more profitable and resilient as a result – and far better prepared for the challenges of the energy transition.

Will this cycle be boom then bust?

Never say never, but unlikely. We think this cycle is different. For one thing, the energy transition and the spectre of peak demand are all the incentives the industry needs to stay the course on capital discipline. Inflation is a challenge driving up costs, with hot spots geographically and along the value chain. But we are seeing operators moderate activity to take the heat out of the market. That’s evident in the US Lower 48 where the rig count is flattening off after doubling in three years. Internationally, operators are deferring conventional project sanctions rather than allowing higher costs to eat into returns.

Is the supply chain resilient?

We worry about the lack of spare capacity available to meet upstream’s needs through the cycle. The service sector is going through its own re-invention – companies have embraced capital discipline, focused on profitability and rebuilt balance sheets. Strategically, they are also trying to balance opportunities in the energy transition with the core oil and gas business. We expect companies to go for margin rather than market share; and upstream supply chain capacity to creep rather than leap, which has been the traditional response in an upcycle. That restraint could lead to a tighter supply chain than the industry has been used to. A new level of collaboration between the supply chain and operators will be required to avoid service cost volatility.

{kind=link}