Need to know: European natural gas market Summer 2026

From natural gas production expectations to LNG production ramp-up and the impact of the Iran war on US LNG exports, the information you need as a trader

1 minute read

David Lewis

Senior Research Analyst, Gas & LNG

David Lewis

Senior Research Analyst, Gas & LNG

David Lewis breaks down Europe’s gas market volatility with deep insight into supply, demand and trading dynamics.

Latest articles by David

-

Opinion

Where global gas markets are mispricing risk

-

Opinion

Need to know: European natural gas market Summer 2026

-

Opinion

What defined gas trading in 2025: five moments that mattered

-

Opinion

European natural gas: your top seven questions answered

-

Opinion

European natural gas winter outlook 2025

-

Opinion

Dynamics shaping the European natural gas market

Lucas Schmitt

Principal Analyst, Short-Term LNG

Lucas Schmitt

Principal Analyst, Short-Term LNG

Lucas provides clients with data and insight on short-term gas and LNG markets.

Latest articles by Lucas

-

Opinion

Need to know: European natural gas market Summer 2026

-

Opinion

Gas and LNG in H2 2025: a commodity trader’s guide

-

Opinion

Gas and LNG in 2025: a commodity trader’s guide

-

Opinion

International Energy Week 2025: our key takeaways for oil & gas

-

Opinion

Will lower gas prices spark switching in Europe and Asia?

-

Editorial

Satellite tracking, remote sensing: how we monitor the LNG market

With Europe relying on imports for up to 90% of its natural gas needs, global supply and demand fluctuations can significantly impact the European market. So, what themes should traders be most aware of over the coming months?

Wood Mackenzie’s European gas and LNG experts have just presented our summer European natural gas outlook webinar, answering the questions that matter for the European market. Complete the form at the top of the page to access the presentation from that event, or read on for an overview of the themes covered.

How does the Middle East conflict impact LNG supply and demand?

1. Damage to existing LNG facilities

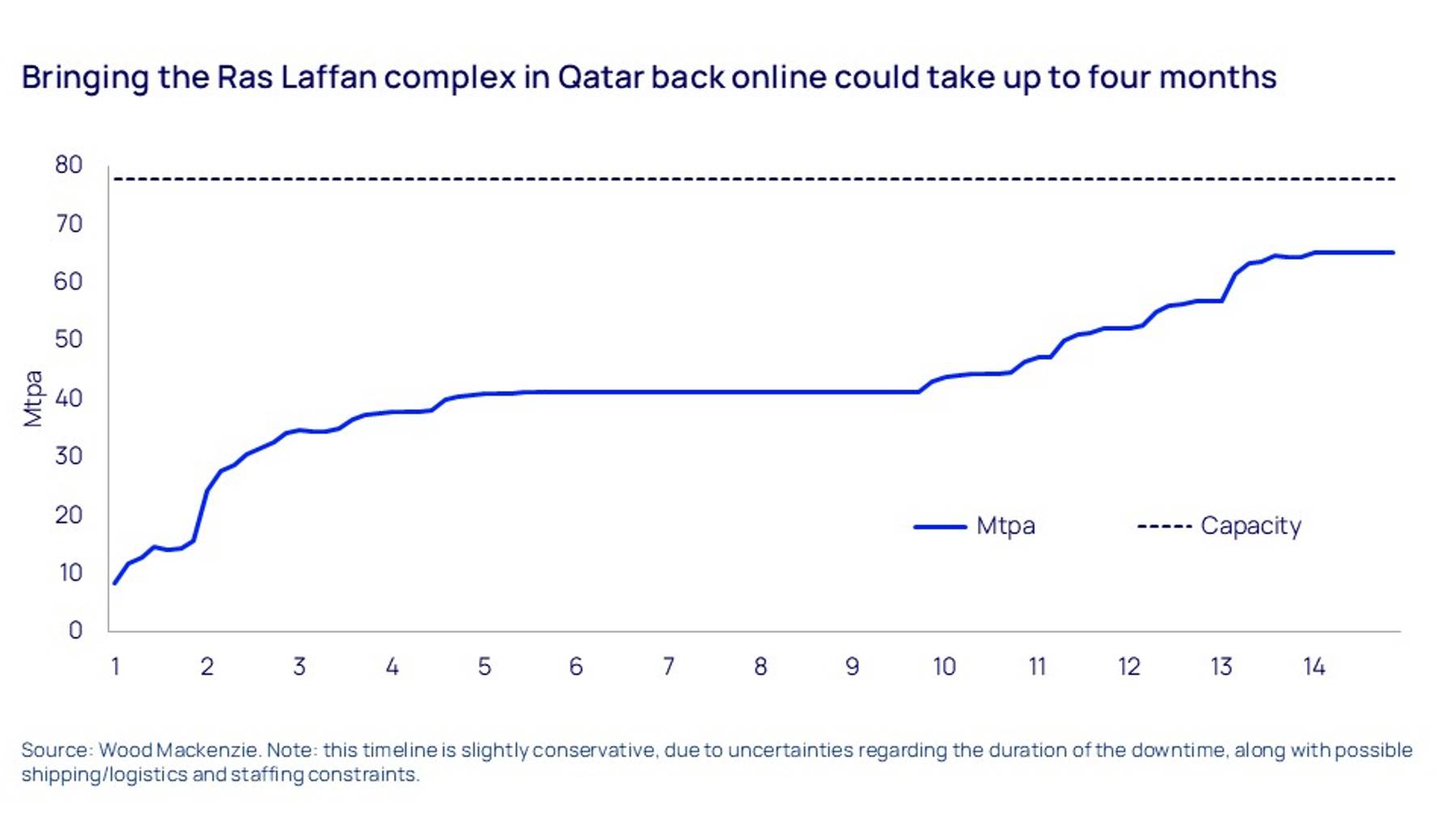

The interruption of cargo transit through the Strait of Hormuz has led to the shutdown of the major LNG export hub at Ras Laffan in Qatar.

Bringing such a large facility back online is a first. The restart will be a sequential, cluster-by-cluster procedure. We estimate upstream flows will be quick to restart, while it will take around a week to get offline trains back to operations. Some have remained partly operational at the Qatargas complex, which could speed up the restart procedure. However, the resumption of shipping through the Strait of Hormuz is the key risk for a successful and durable restart.

At the RasGas complex, high-resolution satellite imagery shows pipe rupture damage on the liquefaction process at Train 6. We expect the RasGas complex could see a delayed restart, allowing for additional technical and safety checks on non-damaged trains following the attacks.

{kind=link}

2. Delays to LNG projects under construction

Another impact of the war is delays to new projects - most significantly the Qatar North Field East facility, which was due to export its first cargo at the end of the year. Construction activity was reduced to a minimum and commissioning activity stopped; as a result, we now expect first cargo in late summer 2027, and a delay to subsequent trains. This could hold back 8 million tonnes of year-on-year supply growth from the global market in 2027, rising further in 2028.

What will be the impact on global LNG supply?

Additional projects, mostly in the US, will offset part of the Qatari disruption. However, even assuming Qatari exports can resume by August 2026, global LNG supply will drop at least 30 million tonnes per annum (mmtpa). Additional impact from delays to new projects will shift the softening of the market from 2026-27 to 2028-29.

Which countries will be most affected by supply disruption?

Before the crisis, 90% of Qatari and United Arab Emirates (UAE) cargoes went to Asia. China benefits from a diversified energy portfolio, with some flexibility and subdued demand, but South Asia (India, Pakistan and Bangladesh) all depend on Middle Eastern LNG for more than 50% of their supply.

Countries have used a range of measures to offset the drop in deliveries, including purchases on the spot market, using up LNG inventories, fuel switching and demand destruction. Overall, we expect Asian LNG demand to decline by over 10 million tonnes in 2026, for a second consecutive year. The scale of the demand reduction in Asia is the critical factor to balance the Middle East LNG disruption.

How is the European natural gas market reacting?

European gas prices have risen less than in Asia, thanks to lower dependency on Qatari and UAE LNG. However, despite falling after the ceasefire announcement on 8 April, at the time of writing they were around 40% higher than before the conflict. What’s more, we now expect European LNG imports to be 13% lower than expected pre-crisis due to cargoes being pulled away to Asia.

In the power sector, rather than any spike in coal generation, the reaction has been a fall in electricity demand from energy-intensive industries, along with a drop in load caused by milder-than-normal weather.

Looking ahead, we expect higher prices to curb gas generation and reduce industrial demand. However, residential and commercial demand should remain robust. Minor additional supply may be added through deferred maintenance in Norwegian production, while Italy may benefit from increased Algerian exports. However, other alternative sources of production are limited.

Remember to complete the form to download the full webinar presentation, which includes a range of charts and data along with our storage expectations for Europe.

You may also want to learn more about Wood Mackenzie connected intelligence across the pricing chain, including our Commodity Trading Analytics, Lens Gas & LNG and Power Trading Analytics products.