Sign up today to get the best of our expert insight in your inbox.

How quickly can Gulf oil exports recover?

The challenges of getting the oil value chain back to capacity

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Alan Gelder

SVP Refining, Chemicals & Oil Markets

Alan Gelder

SVP Refining, Chemicals & Oil Markets

Alan is responsible for formulating our research outlook and cross-sector perspectives on the global downstream sector.

Latest articles by Alan

-

The Edge

Oil and gas markets’ perilous dilemma

-

Opinion

The Hormuz shock: what the data reveals about global oil markets in 2026

-

The Edge

Has the oil price bubble burst?

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

UAE’s exit rattles OPEC’s grip on the oil market

Fraser McKay

Head of Upstream Analysis

Fraser McKay

Head of Upstream Analysis

As head of upstream research, Fraser maximises the quality and impact of our analysis of key global upstream themes.

Latest articles by Fraser

-

Featured

Upstream oil and gas 2026 outlook: half-time report

-

Opinion

Global upstream update: handpicked for small and mid-sized E&Ps

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

Ceasefire in the Middle East

-

Opinion

The biggest topics in global upstream

-

Opinion

Middle East conflict set to drive oil and LNG prices significantly higher

Alexandre Araman

Director, Middle East Upstream

Alexandre Araman

Director, Middle East Upstream

Alexandre has global experience in commercial research, upstream valuations and supply and demand analysis.

Latest articles by Alexandre

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

UAE’s exit rattles OPEC’s grip on the oil market

-

Opinion

Syria’s energy sector poised for historic revival

-

Opinion

The Middle East forges ahead in the race to dominate global gas supply

-

Opinion

Iraqi gas production increasing as flaring levels fall

-

Opinion

Can the Iraq-Turkey pipeline logjam be cleared?

Dalia Salem

Senior Research Analyst, Middle East Upstream

Dalia Salem

Senior Research Analyst, Middle East Upstream

Dalia is responsible for upstream research with a focus on UAE and Oman.

Latest articles by Dalia

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

UAE’s exit rattles OPEC’s grip on the oil market

-

Opinion

The Middle East forges ahead in the race to dominate global gas supply

-

Opinion

Can the Iraq-Turkey pipeline logjam be cleared?

-

Opinion

An ADNOC trilogy (part 3): big gas ambitions

-

Opinion

An ADNOC trilogy (part 2): building a gas nation

Douglas Thyne

Research Director, Oil Supply

Douglas Thyne

Research Director, Oil Supply

Douglas manages our global oil supply research and forecasts.

Latest articles by Douglas

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

UAE’s exit rattles OPEC’s grip on the oil market

-

The Edge

Boiling a frog – could oil prices test US$200/bbl?

-

The Edge

How Venezuela complicates the oil market’s delicate rebalancing

-

Opinion

Venezuela regime change: what it means for oil production, crude and product markets

-

The Edge

Oil’s resilience in the energy system

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

The now twice extended ceasefire between the US and Iran and ongoing talks towards peace give hope that the war ends soon. If a sustainable agreement is finally reached – and as we write it’s still a big if – it could lead swiftly to the reopening of the Strait of Hormuz, kick-starting the process of returning shut in oil supply to the global market which peaked in May at around 12 million b/d.

Our May Horizons scenarios mapped out the implications of the timing of the reopening on energy markets, oil and LNG prices and the global economy. Here our experts, Alan Gelder, Fraser McKay, Alexandre Araman, Dalia Salem, Ali Nabizadeh and Dougie Thyne assess what challenges lie ahead to get oil exports back to pre-war levels.

What’s the trajectory for oil production?

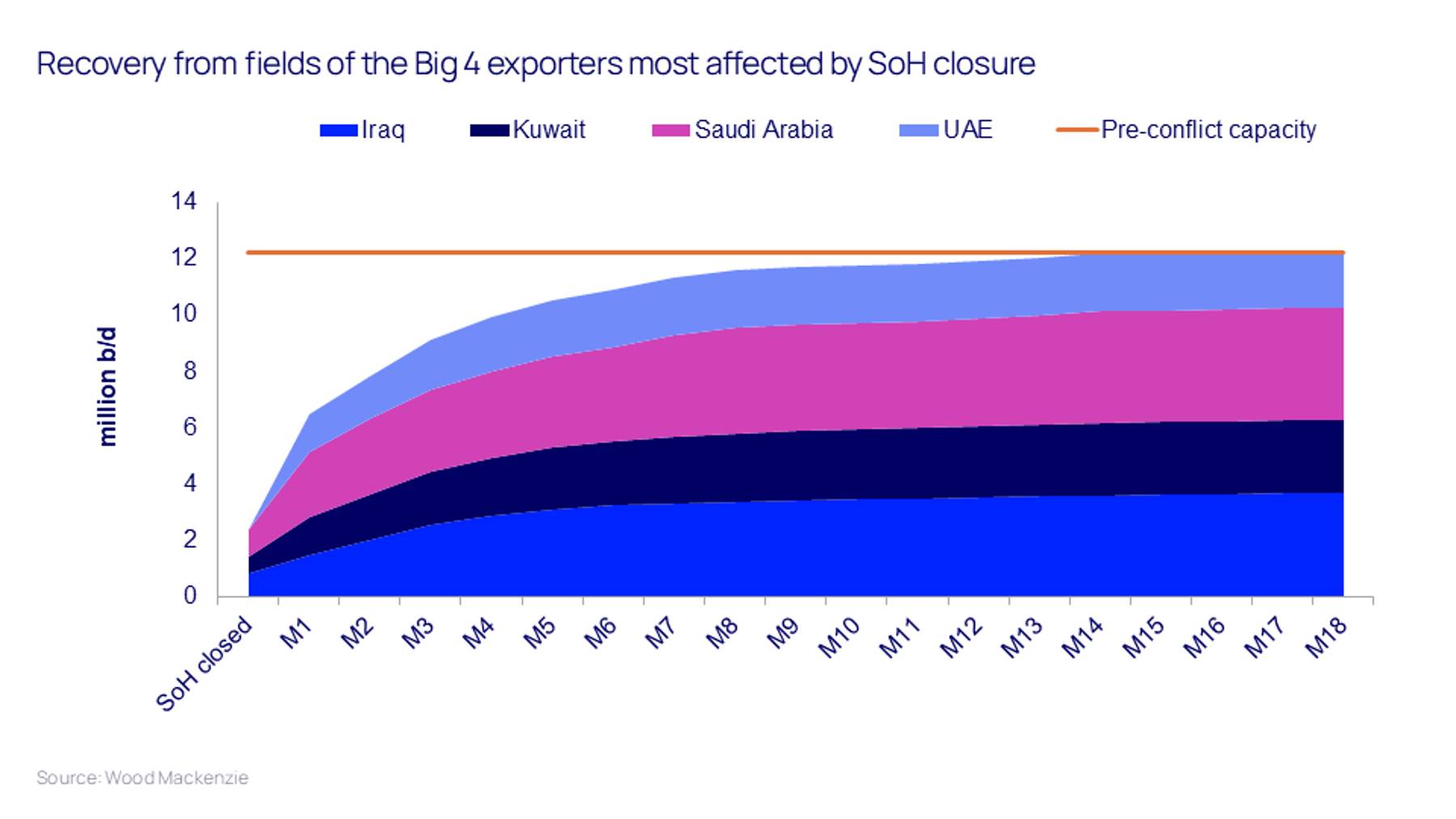

If the Strait reopens in the next few weeks, we believe much of the shut-in supply could be restored fairly quickly. Wood Mackenzie data indicates that Saudi Arabia and Iraq have been pre-emptively increasing supply in the last few days. In most instances, the main bottleneck will be the logistics of resuming export flows and safely managing field start-ups rather than subsurface deliverability.

Assuming operators choose a measured and controlled ramp-up, our analysis suggests the fields affected by the Strait’s closure could get back to 70% of prior production within three months and to 90% within six months. The last 1 million b/d or so will take considerably longer.

What factors drive the upstream recovery path?

There are a lot of subsurface variables. These include the age, maturity and size of the field, the proportion of production shut in, how long it’s been shut in and whether the shut-in process (in some cases done at speed and under duress), was well managed or not. The nature, quality and bubble point of the reservoirs, recovery mechanisms and technology being utilised, and water salinity are all critical factors.

Add to these, the above-ground challenges. Gas handling and water reinjection must be simultaneously restarted to avoid reservoir damage. The proportion of water in the produced fluids will be higher temporarily in many fields. Restarting and re-optimising these systems is a key risk.

Then there’s the coordination with the supply chain. Multiple factors could inhibit the pace or the quality of the restart such as deploying staff in the right places; mechanical or other issues with artificial lift; restarting remote power generation; and pipeline flow assurance and integrity issues. Some of the oldest, or trickiest wells, will likely never recover.

These issues will vary country-by-country and field-by-field. Focusing on the Big Four Gulf exporters, Saudi Arabia and UAE both have high quality reservoirs and, because they have export pipeline capacity circumventing the Strait, have the smallest proportion of total supply shut in. We expect production recovery in both countries will be at the faster end of the recovery range.

The ramp up for Kuwait and Iraq is likely to be slower. Neither has had alternative export options resulting in the forced shut-in of all production above volumes meeting local demand. Iraq will the slowest of the Big Four to return to pre-war levels, due to reservoir maturity, technical and operational complexity.

Could delay in reopening the Strait of Hormuz affect the recovery?

It’s highly likely that an extended closure will reduce the bouncebackability of production for some fields. The exact impact is hard to predict, but many of the issues outlined above are exacerbated by duration. More wells in more fields would need intervention to get back to full production, adding cost and slowing the recovery path.

What other obstacles could slow the return of oil to the market?

With the best will in the world fully restoring Gulf liquids exports to February levels is going to take months. Given the many hurdles, we’d identify four key stages.

- First, assurance of safe passage for marine traffic with no restrictions through the Strait in both directions – mariners, insurers and vessel owners will insist on nothing less.

- Second, getting vessels currently stuck in the Gulf on their way to market. We assume that by now all are fully loaded with crude or product and good to go.

- Third, restoring tanker loading protocol and logistics. Empty vessels sitting outside the Gulf will gain entry for loading from storage in ports, creating ullage to allow oil production to restart. Breaking the logjam requires rebooting tanker traffic flows – empty vessels need to be loaded and sent on their way. It will be many weeks before they return ready to refill, so in the meantime, other vessels need to relocate to enable sustained recovery in transit traffic and export flows.

- Fourth, cranking back up to capacity the pre-war value chains in each country – producing wells, pipeline infrastructure, refineries, petrochemical facilities, storage tanks and loading facilities.

Are there levers to pull if the production recovery stutters?

Restoring supply on this scale is wholly unprecedented and there will be pleasant surprises and but also setbacks. Saudi Arabia and UAE have some flexibility. They can use their spare production capacity and storage to smooth the ramp up of exports should there be hiccups in the recovery of production from individual fields.

{kind=link}

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.

Sign up today using the form at the top of the page.