Six factors shaping the lithium market

Understanding lithium market nuances is vital to forecasting future demand, supply and pricing

4 minute read

Allan Pedersen

Research Director, Lithium

Allan Pedersen

Research Director, Lithium

Latest articles by Allan

-

Opinion

Lithium: too much of a good thing?

-

Opinion

Lithium: too much of a good thing?

-

Opinion

The strategic planning outlook for lithium | Video

-

Opinion

The strategic planning outlook for lithium | Video

-

Opinion

The strategic planning outlook for lithium | Video

-

Opinion

How will the lithium market rebalance?

Soaring demand from electric vehicle (EV) uptake saw lithium prices spike in 2022, before falling back at the start of 2023. But what can we expect from the lithium market in the future, and what factors will drive demand, supply and pricing?

Our recent Future Facing Commodities Forum focused on the short and long-term outlook for materials, including lithium, that are essential to building our electrified future. Missed the event, or want a recap? Fill out the form to access a replay of the panel session on lithium, cobalt and nickel supply and market developments. And read on for a brief overview of the key factors driving lithium market dynamics.

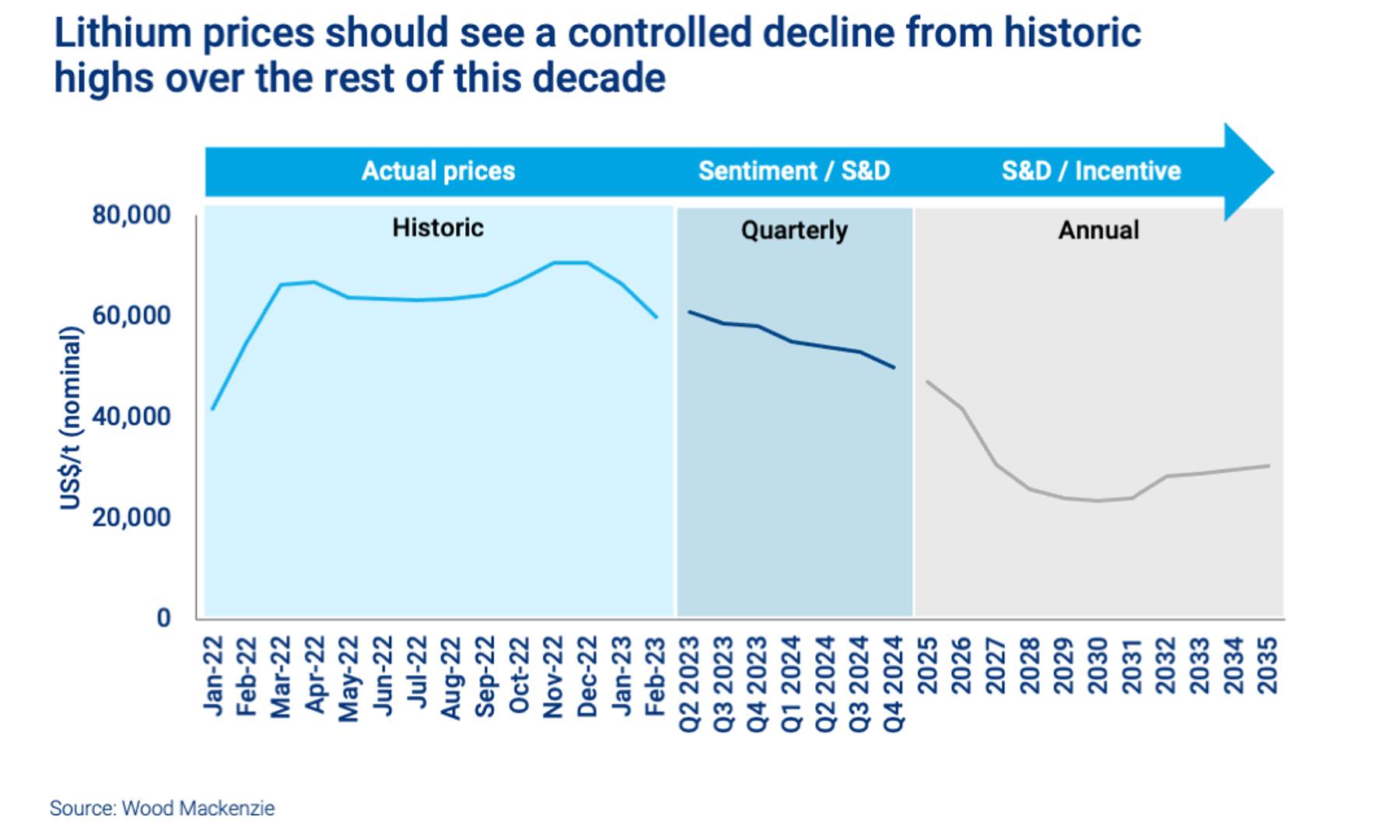

1. Strong growth is creating a ‘bumpy’ lithium market

Lithium strongly demonstrates the characteristics of an immature market, with the supply balance fluctuating between deficit and surplus. A single end use is rapidly coming to dominate the market, with rechargeable batteries now accounting for approximately 85% of global demand. As EV uptake took off through 2021 and 2022, demand surged.

However, infrastructure development in terms of both mines and refineries requires massive investment of both time and money. As a result, supply struggled to keep up.

This imbalance caused prices to soar in 2022, peaking above US$70,000 per tonne. However, demand growth has been slowing down somewhat as EV subsidies are reduced or removed and prices have fallen back in 2023. Going forward, we expect prices to enter a period of controlled decline, settling back to around US$20,000 per tonne by the end of the decade.

{kind=link}

2. Quality is an issue as batteries become the dominant market for lithium

While more and more lithium is being deployed to make rechargeable batteries, not all lithium is useable for this purpose. Battery-grade lithium products have to be of the highest quality and purity and are therefore the most complex to produce. New refineries will tend to start by producing lower quality, technical-grade lithium, which is not directly useable in batteries.

As new plant operators gain experience and fine-tune their operations, the purity of the refined product can be improved to the point where it becomes viable for batteries. Only at this point can the qualification process begin, which is something that each cathode maker does individually.

As a result, despite a high overall supply surplus battery-grade lithium products will see a tighter market, at least in the short term.

3. Lithium is not really a single product

Another complicating factor in assessing future lithium supply and demand is that the market actually comprises two different key products. Both lithium carbonate and lithium hydroxide are used in the production of rechargeable batteries for EVs and electronics. However, the use of one or the other is decided by the cathode chemistry used in the batteries.

Lithium carbonate is mainly driven by lithium iron-phosphate (LFP), which has been widely used in batteries in the Chinese market and is now making inroads in other regions. Lithium hydroxide is driven by high nickel cathode chemistries, which are increasingly favoured by the premium EV market due to their higher energy density. This has important implications for the pricing of the two different compounds.

4. Sources of lithium supply in the long term are unclear

Our knowledge of existing, planned and potential projects means we can project the trajectory of lithium supply until the end of the decade with reasonable accuracy. Mapping this against expected demand makes it possible to forecast price trajectories over the medium term with reasonable confidence.

From 2030 visibility becomes much less clear. At this point incentive pricing – the price at which it becomes attractive for companies and investors to commit to new projects – becomes an important factor. Assuming 1.5 million tonnes of supply, the fully allocated cost of lithium (C3), including operating costs, indirect costs and interest charges, would be around US$15,000 per tonne. Market pricing would therefore be somewhere north of this.

5. The lithium market is still relatively immature

Perhaps the biggest challenge in forecasting the future of the lithium market is that the industry is still essentially in its infancy. There are no globally accepted specifications for the product, and therefore no accepted anchors to ground pricing.

The need for unique and very precise specifications makes lithium products almost comparable to speciality chemicals in terms of pricing complexity. At the same time, the need to keep up with continued demand growth prevents the industry from taking a step back and assessing how to establish a more uniform and consistent approach. Greater standardisation is likely in the future, but it will take time to emerge.

6. Partnerships will be key to the lithium industry’s future

In 2022, 52% of lithium supply came from just five companies. However, we do not anticipate significant M&A activity in the industry and predict these companies’ share will decline to 36% by 2032 as smaller firms grow and new ventures emerge. But while horizontal integration will not be a big theme going forward, vertical integration certainly will be.

Partnerships between miners and refiners make sense, since they can share both the risk and the huge capital requirement involved in new projects. Working together, upstream and downstream operations can leverage each other’s expertise to improve margins and capture more market share. This sort of alliance is already happening; for example, Pilbara Minerals have partnered with POSCO in South Korea, while SQM and Wesfarmers have joined forces on a project in Western Australia. We expect similar partnerships to become prevalent in the industry in future.

Get a closer look at the future of lithium

Don’t forget to fill out the form to access the webinar replay. This includes forecasting of demand, supply and pricing, as well as a discussion of the impact tackling emissions could have on the lithium market.