Top steps miners can take to reduce scope 3 emissions

Motivated by climate policy and climate change vulnerabilities, the major mining companies have embraced operational net zero targets by or before 2050. But when it comes to Scope 3, there is a lack of consensus on targets.

4 minute read

James Whiteside

Director, Head of Corporate Research - Metals & Mining

James Whiteside

Director, Head of Corporate Research - Metals & Mining

With 15 years of experience in the metals and mining industry, James leads our corperate coverage.

Latest articles by James

-

Featured

Metals & mining 2026 outlook

-

Opinion

The end of capital discipline in mining?

-

The Edge

Big Mining pivots to copper for growth

-

Featured

Metals & mining 2025 outlook

-

Opinion

Battery power play: countercyclical opportunities in raw materials

-

Opinion

Copper rush: A strategic analysis

Major mining companies’ scope 3 emissions make up 4% of global carbon emissions. Stakeholder pressures are mounting for a broader, more comprehensive scope 3 targets and the International Council on Mining and Metals is encouraging its members to align on scope 3 targets by the end of 2023.

In our recent whitepaper, ‘Unearthing a pathway to supply chain net zero’, we used data from our Emissions Benchmarking Tool to explore how mining companies can select the optimal strategies for tackling scope 3 emissions based on transition dynamics.

You can find out more the other strategies being used to reduce scope 3 emissions by filling out the form on the right, or read on for a short summary of some of our recent whitepaper's key points.

What progress has been made so far in reducing scope 3 mining emissions?

Today, all the major mining companies have operational net zero targets by or before 2050, with interim targets that aim to be ‘Paris-aligned’. While most have been publishing scope 3 assessments since the middle of the last decade, there is still no alignment in approach to scope 3 emissions reductions amongst the majors. While some companies have extended their net zero ambitions to scope 3, others only believe it is possible to target medium term reductions.

Additionally, many have made a conscious decision to resist pressure from some quarters to assume accountability for customers emissions.

Where do mining’s scope 3 emissions come from?

Downstream scope 3 emissions are the majority of carbon emissions for most miners. Product use dominates the scope 3 emissions associated with coal production, while product processing is huge for companies selling iron ore, bauxite and alumina. Recognising this difference helps determine transition risk.

It’s also worth noting that transportation (predominantly downstream) emissions are relatively small for major mining companies, yet together the transportation scope 3 emissions of the 8 miners are 39.9 million tonnes of carbon equivalent emissions each year.

Setting targets to reduce scope 3 emissions: the opportunities and the challenges

To bring down these emissions, we suggest that scope 3 targets can be different for commodities with variable outlooks. For example, technological and collaborative barriers specific to each commodity play a role in shaping the pace of decarbonisation for scope 3 emissions.

Understanding and navigating these challenges is crucial for mining companies and investors in establishing ambitious targets and fostering effective collaboration within their value chain.

While some companies have extended their net zero ambitions to scope 3, others see a workable path to reduce scope 3 emissions in the medium term.

Several broad scope 3 strategies have emerged in metals and mining

Industry leaders are making moves to tackle scope 3 emissions and four overarching strategies have emerged. Companies must find the best combination of strategies to achieve scope 3 ambitions that fit their unique market positions and business goal.

For example, technology development is gaining momentum. The number of technology-related JVs entered into by the miners has picked up in recent years. Companies are developing low-carbon technologies to accelerate scope 3 reduction and to influence product demand.

Another development in the technology front is the role of venture capital funding that has enabled mining companies to pursue a broad range of decarbonisation technology. Companies are collaborating with material science startups to discover novel applications for their metals, seeking growth in new industries as they pivot.

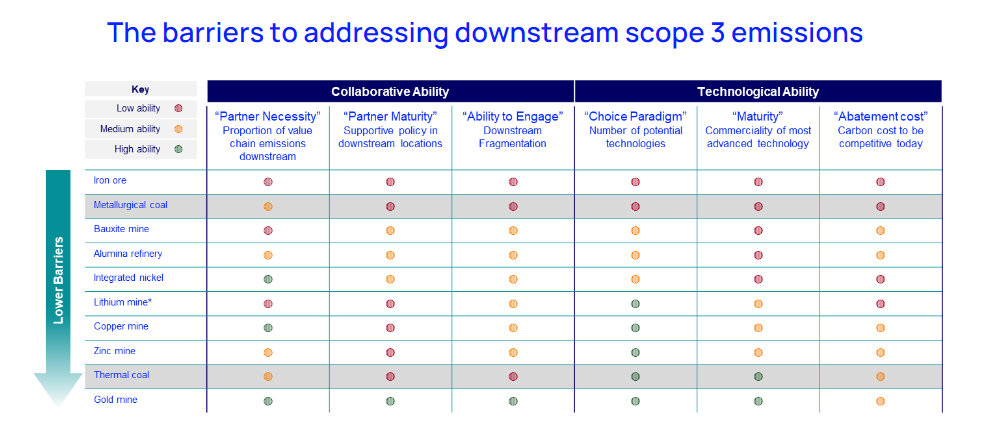

Collaborative and technological barriers require a varied pace of ambition. Assessing the collaborative barriers existing within each industry can guide the timeline for scope 3 targets. The table below provides an analysis of barriers to addressing downstream Scope 3 emissions:

To evaluate the appropriate pace for downstream emissions reduction in each commodity, we propose a framework that categorises barriers into collaborative and technological dimensions. Three technological factors are considered:

- Choice paradigm: The challenge of selecting a specific decarbonisation technology from the numerous potential options available in an industry.

- Maturity assessment: Evaluating the commercial viability and advancement of the most sophisticated technology accessible to downstream industries.

- Abatement cost: Quantifying the carbon expenses associated with implementing the average technology required for commercial viability.

This assessment highlights the challenges facing some companies in tackling scope 3 emissions.

Collaborative barriers also encompass three factors:

- Evaluating the extent to which downstream partners contribute to the overall carbon footprint of the product.

- Considering the geographical locations of downstream partners and the strength of carbon policies in those regions.

- Assessing the feasibility of engaging with downstream partners, taking into account the number of potential partners within the industry.

By employing this framework, companies can not only guide the pace of their ambition but also direct attention to areas requiring focused efforts and determine the most effective approach for collaboration within their value chain.

Mining companies and investors have demonstrated commitment to climate ambition by embracing operational net zero targets by or before 2050. It is imperative for mining companies to meet scope 3 pressures and ensure their role in a net zero future.

By driving innovation and optimising supply chains, mining companies can contribute significantly to global decarbonisation efforts, but this requires a strategic focus on transition dynamics and a combination of targeted strategies.

To find out more about the other strategies being used to reduce scope 3 emissions, fill out the form at the top of the page to download a free extract from ‘Unearthing a pathway to supply chain net zero’.

LME Forum 2023

Securing metals supply in a rapidly changing landscape | 11 October, in London

Register now