Discuss your challenges with our solutions experts

What investors want to know about energy and natural resources

The impact of Covid-19 on energy demand remains top of mind, but investors’ questions reveal a return to calm if not a return to “normal”

1 minute read

Martin Kelly

Global Head, Curated Service, Energy & Natural Resources Research

Martin Kelly

Global Head, Curated Service, Energy & Natural Resources Research

Martin oversees our Curated Service offering, working across our energy and natural resource coverage

Latest articles by Martin

-

Opinion

What investors want to know about energy and natural resources

-

Featured

Digitalisation: upstream's silver bullet?

-

Opinion

What is the current state of the upstream industry?

While investors appear to have dusted themselves off following a brutal Q1, they remain cautious; the risk of a second wave and the uncertainty about the outlook for global economic growth still weighs heavily.

Recent investor questions centre on the shape and duration of recovery, and the ways in which Covid-19 will change long-term energy and commodity demand. In short, investors are looking to understand downside risk as they seek out opportunities in the “new normal”.

Here are some of the topics we’ve addressed for investors in the past few weeks. Learn more about the proprietary region- and commodity-specific advice we provide to investors here.

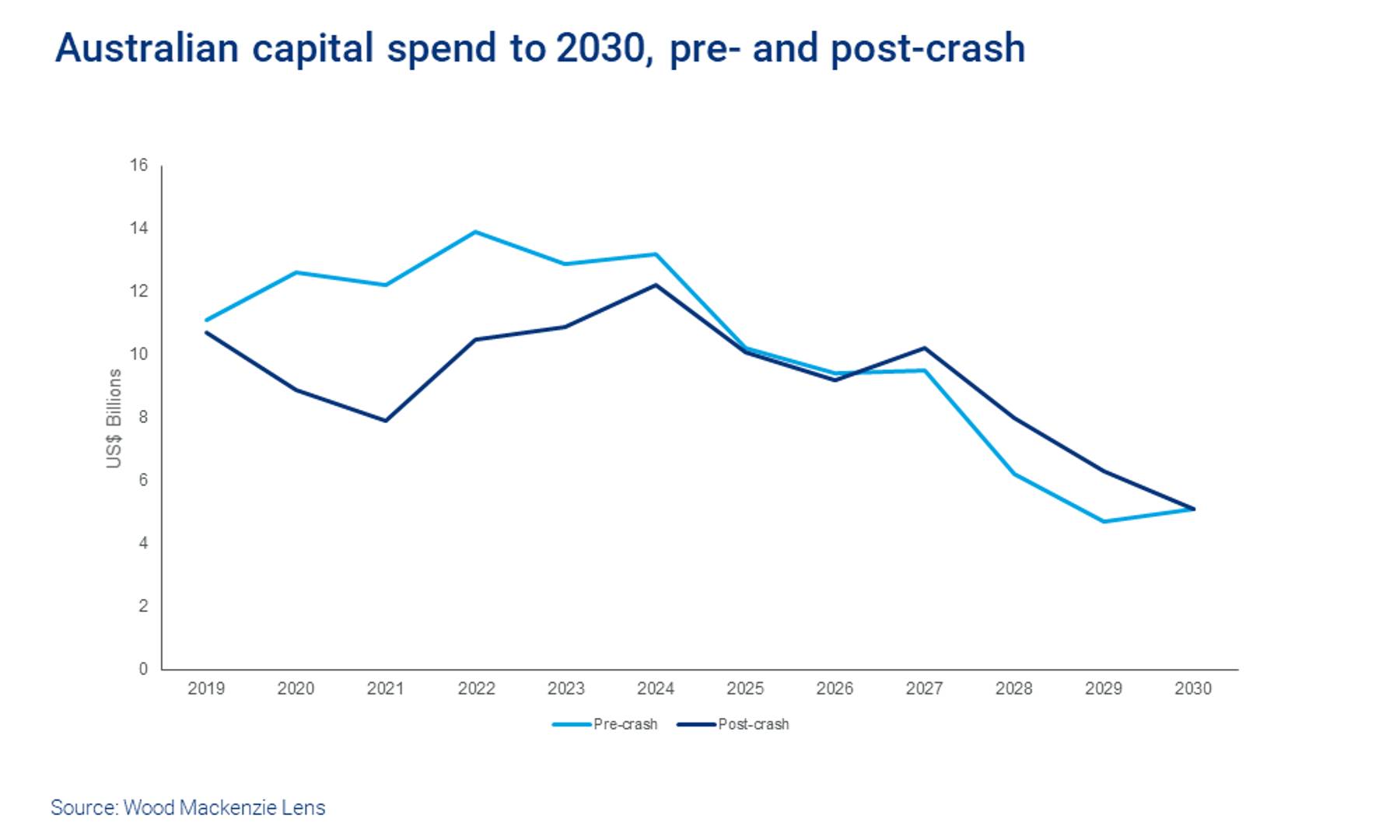

How have low oil prices changed the outlook for the Australasian upstream sector?

Operators around the world are reducing spend and delaying projects to preserve capital and maintain balance sheet strength. The drive for efficiency has intensified. Contractors are being squeezed, and dividends have been cut or even removed entirely.

The upstream sector in Australasia, which was set for a bumper year in 2020, is no exception. At the start of this year, we predicted a ramp-up of LNG supply, billions of dollars of new upstream investment, and plentiful growth opportunities via exploration and M&A. Then everything changed. The double impact of the coronavirus and the oil price crash has swept through the industry. Upstream operators are in a fight for survival.

We've adjusted the global upstream dataset in Lens to reflect the new normal, and we now see a US$4bn reduction in capital spend across 2020 and 2021, mostly due to large capital projects being deferred. Four of the most significant projects we expected to achieve FID in 2020 are on hold, which will have an impact on production in 2023 and beyond.

{kind=link}

{kind=link}

Woodside’s Scarborough project and associated Pluto expansion, and Santos’s Barossa project are still expected to be sanctioned in 2021. These two projects are of strategic importance, linked to the companies’ long-term growth targets. Other projects are less certain, and will slip into 2022 and beyond, depending on the pace of economic recovery.

Listen to this webinar to learn more about how the investment outlook has changed, what the reset of pre-FID project timelines means, and whether low prices present opportunities for M&A.

Which independent European refiners are most challenged by Covid-19?

There are very few truly independent refiners in Europe; most are just a small part of an integrated corporation. The financing position of large integrated energy companies reflects their role across the broader value chain but is primarily focused on from the cash-generating upstream assets.

For the small number of companies where refining forms a major part of their business, the Covid-19 pandemic has been particularly challenging to their earnings and their overall liquidity position. Government lockdowns to control the spread of the virus have constrained personal mobility, reducing the demand for transport fuels and directly impacting refinery throughputs. April 2020 was the lowest month for European oil demand, and the period when refining operations were most underused.

As the lockdowns are eased, demand for transport fuels is increasing and refiners can lift crude throughputs. Product inventories are high and the OPEC+ group response of curtailing oil production has supported its price, squeezing refining margins.

We’ve analysed the impact on refinery earnings using our short-term forecasts for 2020 and 2021, capturing any major investments completed since our most recent annual analysis that details 2018 performance. Aside from major refiners in Scandinavia, the annual earnings of many European refiners will be hit hard by the impact of Covid-19, which will challenge their debt service capabilities.

Contact us if you’d like to receive the data on European refinery earnings from 2018 to 2021. Fill in the form at the top of this page.

How is coronavirus affecting bulk commodity prices?

As the pullback in the Newcastle benchmark thermal coal price from its July 2018 peak approaches its second anniversary, institutional investors are looking at the prospect of an even more prolonged downturn. Indeed, depending on the benchmark, prices are down as much as 50% in the past two years as a variety of issues have conspired to undermine prices.

The drop in met coal prices is newer, but the Queensland benchmark is down almost 40% from one year ago. Investors are also asking whether this is structural, or if met coal is just a victim of the coronavirus outbreak and that prices will recover when it’s resolved.

At the other end of the spectrum amongst bulks is iron ore. Investors began the year thinking we’d finally see weakness with plateauing Chinese steel production, Brazil returning to the seaborne market and Australia continuing to expand exports. But even as the virus has persisted, China’s blast furnaces have ramped back up, and iron ore prices remain very strong.