Get Ed Crooks' Energy Pulse in your inbox every week

OPEC+ plans to boost oil production

Leading members of the oil producers’ group aim to unwind some of the output cuts they announced last year. But increases will depend on robust growth in demand

10 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is the competitive power market model broken?

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

The US Strategic Petroleum Reserve (SPR) was not designed to turn a profit. It was established after the first oil shock of 1973-74 to protect the US economy from disruptions in oil supplies. But over the past couple of years, it has enabled some profitable speculation on the part of the US government.

Oil from the SPR was sold at an average price of US$95 a barrel in 2022, as Brent crude peaked at over US$125 a barrel in the aftermath of Russia’s invasion of Ukraine. Now the Department of Energy (DOE) is replacing some of the sold barrels at prices of US$79 or below. The reserve has been performing its intended role of countering disruptions in commercial supplies that could threaten the US economy. It is also, the DOE notes, “securing a good deal for taxpayers”.

The immediate reason for this opportunity to sell high and buy low is that crude prices have been tumbling, following the meetings of ministers of the OPEC+ group last week. There is a good reason to think that the markets over-reacted to the outcomes of those meetings, and the fall in Brent crude from a high of US$85 a barrel last week to about US$77 a barrel on Tuesday may have been overdone. But pressures building in the world economy mean the downward pressure on prices may persist. The US may have more opportunities for profitable purchases for the SPR in the future.

It had been clear in the run-up to the scheduled OPEC+ ministerial meeting that there could be changes ahead. The meeting had been signalled in advance as online only, but it then emerged that eight countries – Saudi Arabia, Russia, Iraq, the United Arab Emirates, Kuwait, Kazakhstan, Al geria and Oman – were holding a separate side meeting in person in Riyadh.

The significance of that group of eight countries is that they are the ones that announced additional voluntary production cuts, along with the agreed OPEC+ limits, in April and November of last year. These are the countries that, to varying degrees, have carried the burden of restricting output to support prices, and have the greatest interest in unwinding those cuts.

The agreement from the wider OPEC+ group was that their collective production cuts of 2 million barrels per day, which took effect in October 2022, would remain in place until the end of 2025.

The agreement among the smaller group of eight voluntary cutters was that their first round of reductions totalling 1.65 million barrels per day, announced in April 2023, would also remain in place until the end of next year. But the second round of cuts totalling 2.2 million b/d, announced last November, should be gradually phased out between October 2024 and September 2025.

A useful table provided by OPEC showed what that would mean for production from those eight countries: a total increase in output of about 2.46 million b/d between June to September of this year and October to December of 2025.

It is this strong projected increase in supply that alarmed the markets and sent prices tumbling this week. The reason to think that reaction may have been excessive was that the eight countries were very clear that these production increases “can be paused or reversed subject to market conditions”.

In a video briefing, the Saudi energy minister Prince Abdulaziz Bin Salman underlined the point. The scheduled increase in production would be delivered only if the supply-demand balance in world markets evolves in line with OPEC’s expectations, he said.

“We don’t know how these things will end up,” he explained. “That’s why we want to move diligently, carefully, in a very precautious way. But at least give it to us that we have a plan, and we have a way forward.”

In particular, he raised a cautionary note over OPEC’s oil demand forecast, which had been projecting a strong increase in global consumption this year.

“Unfortunately, there is nothing called rocket science when it comes to forecasting,” Prince Abdulaziz said. “There are moving things here and there. And, unfortunately, they do not relate to OPEC+: they relate to the world economy, to interest rates, to growth. And the jury is still out. For what I have been saying all along: I will believe it when I see it.”

Seen in the context of those remarks, the snap judgment that the OPEC+ group was committed to opening the floodgates and letting additional supply flow seems like a misunderstanding.

However, the global economic trends identified by Prince Abdulaziz clearly create downside risks for oil prices in the future. Wood Mackenzie is projecting only a modest slowdown in global economic growth this year, from 2.7% in 2023 to 2.5% in 2024. But particularly in the US, there have been a few pieces of disappointing economic news that suggest weaker outcomes are possible.

The European Central Bank on Thursday cut interest rates for the first time since 2019, supporting a tentative economic recovery. But in the US, Jerome Powell, chairman of the Federal Reserve, said last month that a rate cut would not be appropriate “until we have gained greater confidence that inflation is moving sustainably toward 2%. So far this year, the data have not given us that greater confidence.”

Gaining enough confidence to cut rates was likely to take longer than previously expected, he added.

Meanwhile in China, economic indicators have been generally quite healthy, but the property sector remains depressed. The government last month launched a bailout package for the property market, including US$41 billion worth of loans from the central bank, support for municipal governments to take unsold homes into public ownership, and a relaxation of restrictions on home-buying.

Above all, the global economy is shadowed by the possibility of trade and fiscal shocks. Trade tensions between the US, EU and China have been escalating again this year, and the political pressures created by elections in many leading economies could result in worsening disputes. Former President Donald Trump has raised the prospect of a wide-ranging new round of tariffs if he is elected in November.

In light of these uncertainties, Prince Abdulaziz “I’ll believe it when I see it” stance on demand growth makes sense. The OPEC+ group has had remarkable success in using production cuts to prop up oil prices since the pandemic, with Brent crude trading above US$75 a barrel for most of the past three years. But declaring victory and unwinding those cuts quickly would be premature.

Mexico elects an energy expert as its new president

Claudia Sheinbaum Pardo was elected as Mexico’s next president last weekend, opening what could be a new era for the country’s energy policy. Her election is a historic moment: she is not only the first woman, but also the first contributor to the Intergovernmental Panel on Climate Change, to serve as a head of government in North America. She has a doctorate in energy engineering, and spent four years working at the Lawrence Berkeley National Laboratory in California, studying energy consumption.

Under President Andrés Manuel López Obrador, popularly known as Amlo, the rhetoric around Mexico’s energy policy was focused on economic nationalism and increasing domestic self-sufficiency. He aimed to strengthen Pemex, the national oil company, and Comisión Federal de Electricidad (CFE), the state power utility. Oil and gas bid rounds and electricity auctions that had been open to foreign companies were halted, and regulatory uncertainty put a brake on investment decisions in renewable energy.

President-elect Sheinbaum is from Amlo’s Morena party, and was selected by him as his successor. In her election platform, she similarly supported the pre-eminence of Pemex and CFE. She is poised to have a qualified majority in Congress, which could give her the power to pass legislation favouring the state energy companies at the expense of the private operators and investors.

However, Mexico’s energy sector faces major challenges as demand grows strongly, and President-elect Sheinbaum will face pressure to re-assess the role of private investment to attract more capital. Recent power cuts have exposed the problems caused by years of under-investment in electricity supply.

Mexico is one of only two members of the Group of 20 leading economies to have not set a net zero goal for emissions, and under Amlo made its 2030 goal less demanding. President-elect Sheinbaum has said she wants to accelerate the development of low-carbon energy, setting a goal of a 50% share for renewables in electricity supply by the end of her term in 2030. If she is to achieve that objective, regulatory and policy frameworks will have to be in place to encourage private investment.

Adrian Lara, Wood Mackenzie’s principal analyst for Upstream Latin America, said he did not expect any immediate radical changes to the status quo in energy policy, for better or worse. However, he added, there are limits to the national energy companies’ ability to fund the infrastructure investment Mexico needs, and ultimately both public and private capital will be required.

In brief

India’s general election concluded with Prime Minister Narendra Modi securing a third term, but his BJP lost parliamentary seats and will have to govern with the support of coalition partners. The need to maintain parliamentary support from other parties could make it more difficult to take politically controversial decisions to advance the development of low-carbon energy.

Global investment in clean energy technologies and infrastructure is on track to be US$2 trillion this year, double the investment in fossil fuels, according to the International Energy Agency.

Climeworks, the direct air capture company, has unveiled a new technology that it says can cut the cost of capture per ton of carbon dioxide by 50% compared to its previous generation of equipment. It hopes to deploy the new technology at its Project Cypress in Louisiana, with a final investment decision scheduled by the end of 2025.

Governor Kathy Hochul of New York has suspended indefinitely the plan to introduce congestion pricing for vehicles in lower Manhattan, which was due to go into effect on 30 June, saying it “risks too many unintended consequences for New Yorkers at this time”. Polls showed a majority of people in New York state opposed the plan, which would have been the first congestion pricing system introduced in the US.

The Sunrise Movement, a climate-focused campaign group, will not back President Joe Biden in the US elections in November.

Other views

The US solar industry is off to a strong start in the first quarter – Michelle Davis and Zoe Gaston

The energy transition in the upstream oil & gas sector: a reality check? – Valentina Kretzschmar

Batteries: Frequently asked questions – Max Reid

Quote of the week

“We are playing Russian roulette with our planet. We need an exit ramp off the highway to climate hell… I call on leaders in the fossil fuel industry to understand that if you are not in the fast lane to clean energy transformation, you are driving your business into a dead end, and taking us all with you."

UN Secretary-General António Guterres warned that a steep decline in global greenhouse gas emissions would be needed this decade to limit global warming to 1.5 °C. In a speech in New York, Guterres called for urgent action over the next 18 months, and said the Group of Seven developed countries should commit to cutting their production and consumption of oil and gas by 60% by 2035.

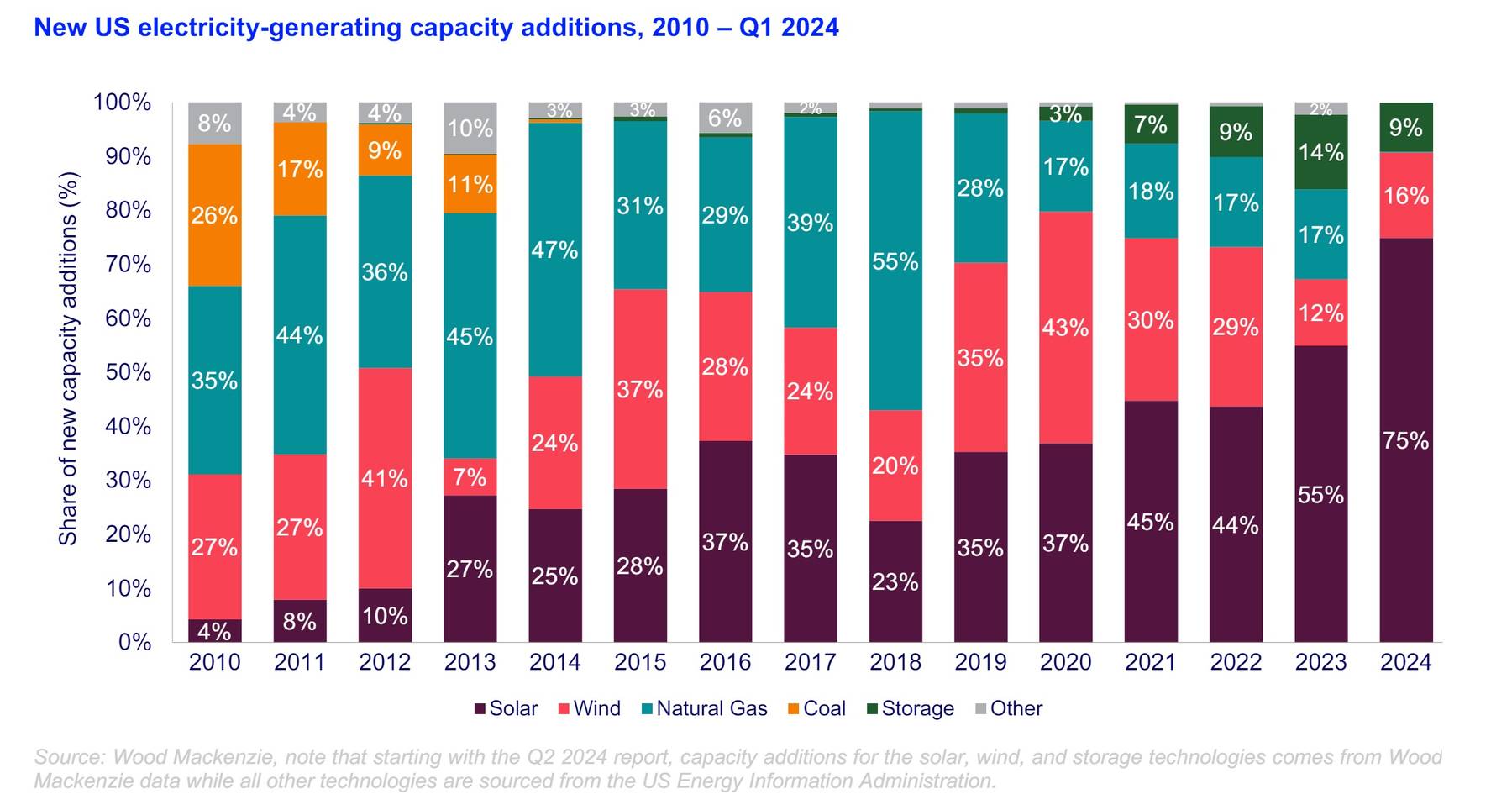

Chart of the week

This comes from the new Wood Mackenzie US Solar Market Insight for Q2 2024. It shows the truly amazing growth of solar to become the dominant technology for additions of new power generation capacity. In 2010, solar represented just 4% of all the new generation capacity added to the grid in the US. In the first quarter of 2024, it was 75%. The note is full of interesting charts and data, some of which I may well use for a “chart of the week” in the future, but you can take a look now at that link.

{kind=link}

Get The Inside Track

Ed Crooks’ Energy Pulse is featured in our weekly newsletter, alongside more news and views from our global energy and natural resources experts. Sign up today to ensure you don’t miss a thing.