Is the electric vehicle and battery supply chain charged for success?

Market dynamics for electric vehicles and energy storage to 2050 will be complex

4 minute read

The future of the battery supply chain for electric vehicles (EVs) and energy storage systems to 2050 will be decided by the complex interplay of a wide range of factors. To understand evolving market dynamics, it’s important to consider expected sales, production capacity and recycling levels, as well as the impact of regulation, cathode technologies and pricing.

So, what level of demand can be expected as the market evolves? Will supply be able to keep up? And what are the implications for each element of the supply chain?

Our report Electric vehicle & battery supply chain: strategic planning outlook to 2050 draws on insight from our Electric Vehicle and Battery Supply Chain Service. Fill in the form for a complimentary extract , or read on for a brief introduction to some of the key themes.

EVs: Asia Pacific will be key to growth

We expect steep sales growth for passenger plug-in EVs, reaching 39 million sales in 2030 thanks partly to the boost provided by recent US regulation. However, over the longer term, the Asia Pacific region will be the key driver of growth, and by 2050 will account for a large proportion of the market. This will help global sales continue to increase through to 2050, albeit at a slower rate.

China’s lead in plug-in EV penetration of both the passenger and commercial vehicle market will support development of the industry throughout Asia Pacific. With the Chinese market levelling off as it saturates, sales in the region excluding China will surpass China itself by the mid-2040s.

Regulations will increasingly require car manufacturers to build a growing proportion of EVs compared to internal combustion engine (ICE) vehicles. With consumer preferences shifting towards SUVs and larger cars, manufacturers will prioritise the C/SUV-C and D/SUV-D model segments to make sure they meet their targets.

More powerful and efficient battery packs will therefore be needed to give passenger EVs sufficient range to make them appealing.

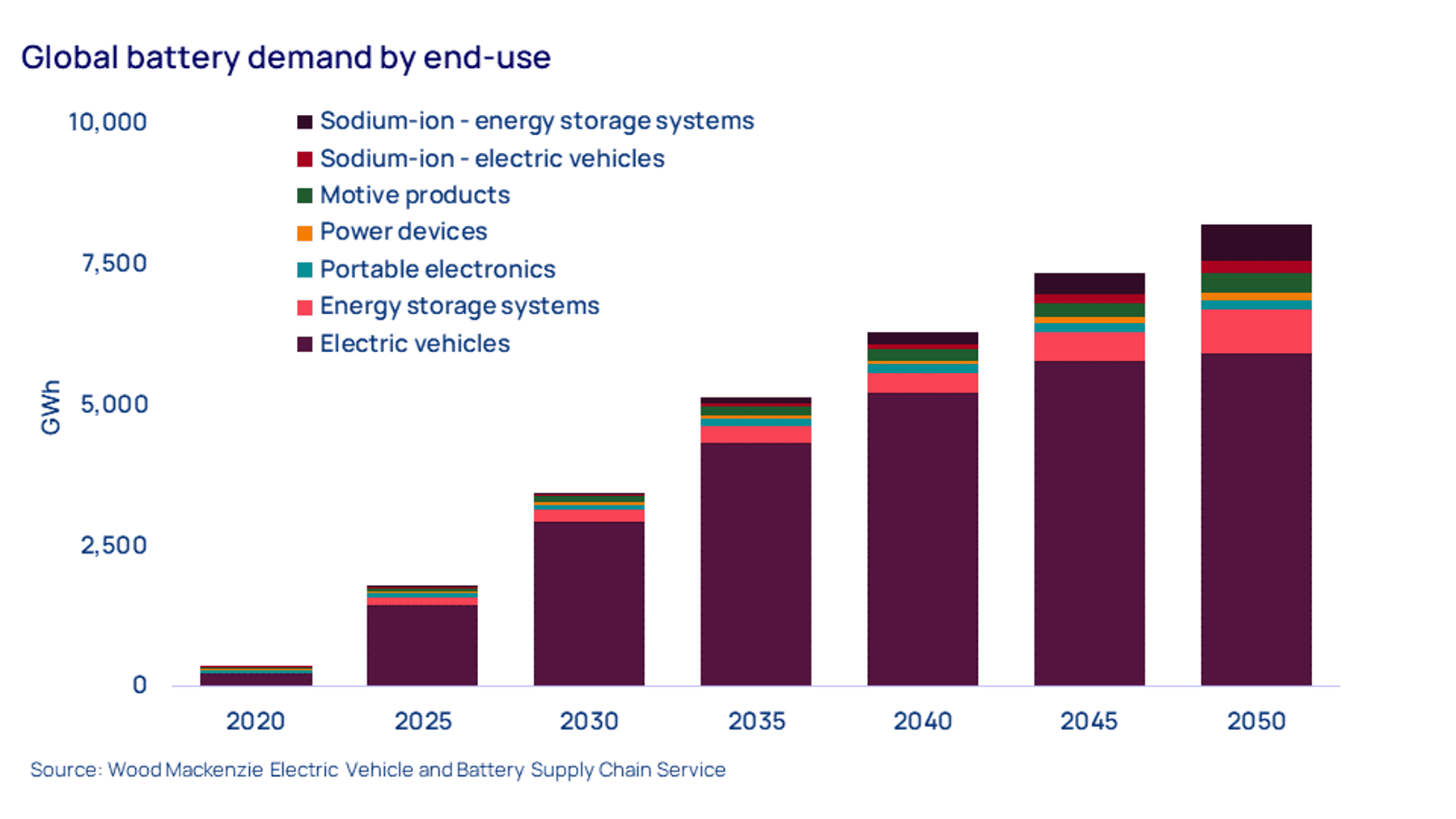

Battery demand: EVs will dominate

Annual global demand for batteries will increase at a compound annual growth rate of 26% until the end of the decade, rising to 3.4 terawatt hours (TWh) by 2030. Demand growth will slow to 3% in the 2040s, with demand reaching around 7.3 TWh in 2050.

EVs will account for the vast majority of demand, with energy storage systems (ESS), motive products, portable electronics and power devices making up the rest.

{kind=link}

Current announced battery production capacity is nearly 10 TWh, which is both ambitious and excessive in terms of expected demand. However, much of this we would describe as ‘probable’ capacity. Under our base case, capacity would be 3.4 TWh by 2030, in line with expected demand.

Technologies: key to battery raw material demand

Preferred cathode technologies for batteries will be a key factor in driving demand for raw materials. We expect the weighted average price of a battery pack to fall below US$100 per kilowatt hour from 2029, mainly thanks to a shift towards iron-based chemistries.

The use of lithium-ion battery technology will continue to grow. Production should reach 3.4 TWh by 2030 and 7.35 TWh by 2050, closely aligning with demand. By comparison, sodium-ion is just at the beginning of its ascendancy – we expect more capacity to be added to the 158 gigawatt hours (GWh) already announced.

Nickel-based cathode active materials are currently only produced in significant quantities in China, South Korea and Japan. By the end of the decade, production will have diversified to Germany, Canada, the US, Poland, Indonesia and Finland. However, the vast majority will still come from Asia Pacific.

Lithium iron phosphate (LFP) batteries account for nearly 70% of both production and installation in China – a switch in technology that has happened in just a few years. However, there are limited plans for production elsewhere and it is currently expected to level off in China by the end of this decade.

Battery raw materials: lithium and nickel in high demand

The continuing global preference for lithium-ion battery technology will be the main driver of a fivefold increase in the lithium market by 2050. Currently, nearly all mined lithium comes from Australia and China (mined lithium represents more than half of global supply, with the rest coming from brine sources). However, by 2030 Africa and North America will account for 30% of mined supply.

Further investment will be key to making sure supply of battery raw materials can meet rapidly growing demand.

Nickel markets will also see huge demand pressure (most lithium-ion batteries use nickel to improve energy density). In contrast to lithium, nickel supply for batteries will remain relatively concentrated in the Asia Pacific region. This will be the main risk to battery pack prices, particularly for batteries using nickel-based chemistries that require a high nickel content.

Overall, further investment will be key to making sure supply of battery raw materials can meet rapidly growing demand. Failing that, the price of those materials and the refined chemicals used in production will rise in the second half of the decade.

Recycling: circularity will increase as EVs reach end-of-life

As production hubs expand, we expect two million tonnes of black mass (shredded and processed battery waste) to be available for processing each year by 2030. That figure will swiftly increase in the 2030s as EVs built in the 2020s reach end-of-life. Only 157,000 tonnes of lithium carbonate equivalent will come from the recycling sector in 2030, meeting just 7% of overall demand. However, by 2050 nearly two million tonnes will be recycled annually.

The full report provides a wealth of data covering future demand, production capacity and pricing, as well as detailed analysis of contributing factors.

Fill out the form at the top of the page to download your complimentary extract, which includes charts on:

- EV sales by region

- Plug-in EV passenger penetration by region

- Announced OEM manufacturing investments to comply with IRA localisation requirements

- Lithium-ion and sodium-ion production capacity forecasts

- And more.