Latin America upstream: opportunities and challenges

Wide-ranging opportunities mean expectations for the future of oil and gas in the region are sky-high. But can they be met?

4 minute read

Luiz Hayum

Upstream Research Principal Analyst, Latin America

Luiz Hayum

Upstream Research Principal Analyst, Latin America

Luiz's expertise lies in valuing upstream assets in Latin America.

Latest articles by Luiz

-

The Edge

Delaying deepwater decommissioning

-

Opinion

Deepwater decommissioning: three key things to know

-

Opinion

Latin America upstream: opportunities and challenges

-

Opinion

Can Brazil’s mature pre-salt oil fields continue stellar performances?

-

Opinion

Deepwater's Latin America comeback

Glauce Santos

Senior Analyst, Latin America Upstream

Glauce Santos

Senior Analyst, Latin America Upstream

Latest articles by Glauce

View Glauce Santos's full profileWith nearly 15 billion barrels worth of varied resources discovered in the region since the turn of the decade, the future looks bright for upstream oil and gas in Latin America. Opportunities of all kinds are fuelling stratospheric expectations for Majors, national oil companies (NOCs) and mid-caps alike. But is this the whole story?

In our recent webinar Fuelling the Future: Latin America's Upstream Opportunities & Challenges, we explored expected activity in the region and looked at what will be needed for the Latin American oil and gas sector to thrive. Fill out the form to download the webinar, or read on for a quick summary of the key themes.

What do future Latin American upstream production levels look like?

We expect strong upstream growth in Latin America this decade, with deepwater and unconventional oil and gas offsetting the decline from mature conventional plays.

Based on data from our proprietary Lens Upstream platform, the region will reach a new peak of 14 million barrels of oil equivalent per day (boe/d) in 2029 – that’s an increase of four million barrels compared to 2020.

Deepwater and ultra-deepwater fields will be the main drivers of growth, with established producer Brazil joined by new provinces including Suriname and Guyana. However, sector players will also be active in shallow waters and onshore, with Argentina’s expected 40% increase in production notable in this respect.

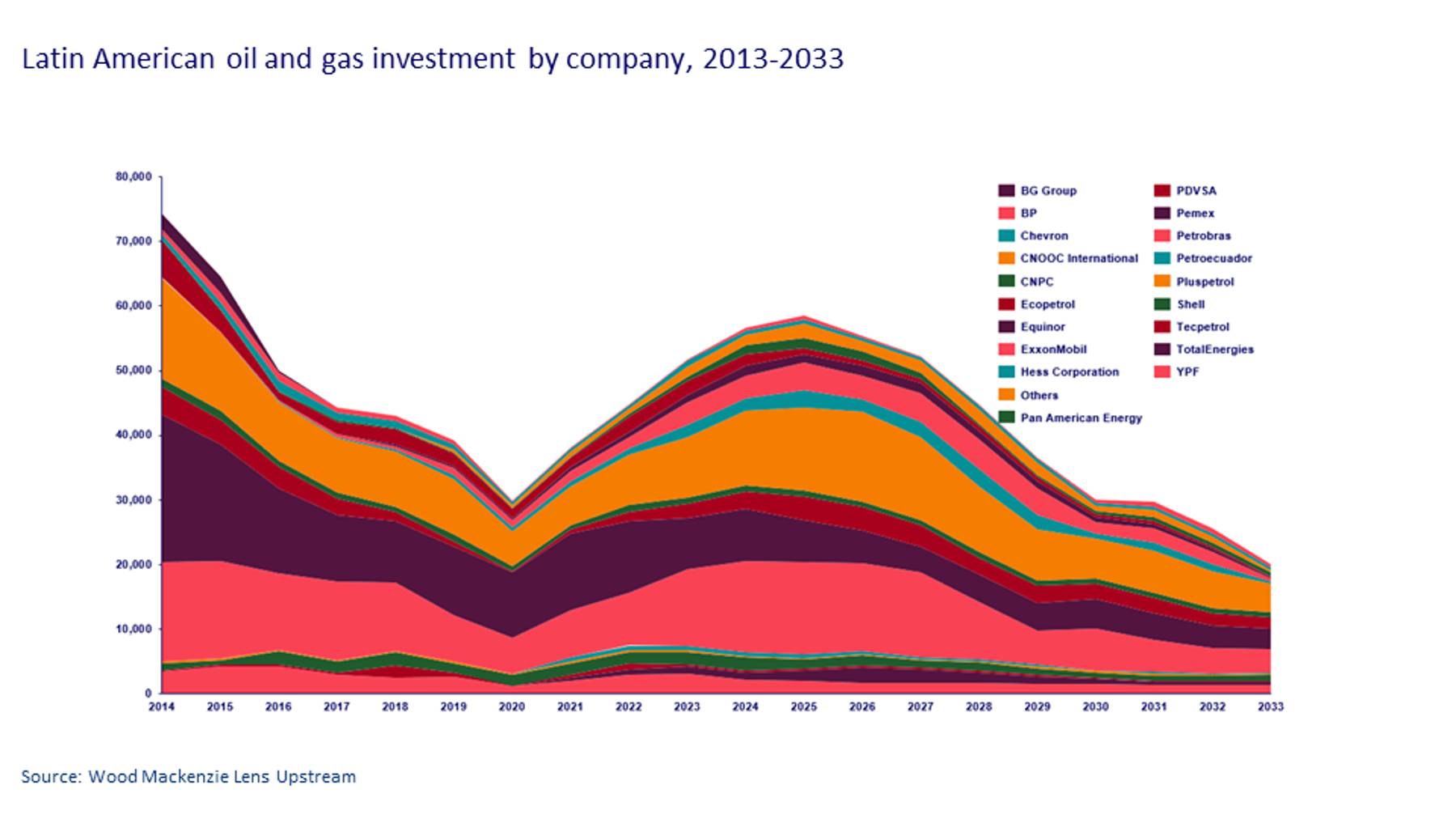

What is the capex outlook for upstream in the region?

At its lowest, investment in Latin American upstream dropped to US$30 billion in 2020, before rebounding post-COVID. We expect capex for the region to peak at US$60 billion in 2025, with investment largely following the same country and thematic trends as production. Deepwater will lead growth and unconventional themes should also recover to pre-pandemic levels. But even heavy oil, conventional onshore and LNG show signs of recovery in the short term.

The region offers opportunities for companies of all sizes. NOCs will dominate investment, with the majors also contributing strongly to deepwater and unconventional plays, while local juniors and midcaps will work to mitigate the decline in productivity from conventional resources.

{kind=link}

{kind=link}

Can Latin Atlantic oil and gas be categorised as advantaged resource?

Talking about exploration opportunities in Latin America means talking about the potential for discoveries in the frontier deepwater areas known as the Upper Cretaceous play. The quantity of prospective resources in these areas is impressive, but what about the quality?

To be categorised as advantaged, we require a project to be resilient, sustainable, timely, and predictable. Resilience is characterised by low costs, strong reservoir performance and high fluid quality, while projects must enjoy good access to infrastructure. To be sustainable, a project must generate minimal emissions, so investment in technology such as clean power sources and carbon sequestration is important. In terms of timeliness, we expect payback for oil to come within 8-12 years, which requires ready market access and workable regulation. And finally, predictability is about ensuring minimal risk, so government support and fiscal stability is important, along with good subsurface intelligence.

Our calculations suggest that the Guyana basin, for example, should achieve payback in less than ten years at an oil price of US$60-80. However, all the key growth opportunities are to be found in very deep water, raising the complexity level – and hence the risk.

Could offshore gas be a gamechanger for Colombia?

The past two years have been particularly eventful for the oil and gas sector in Colombia. A new government has set an agenda to pivot away from the country’s heavy reliance on fossil fuel exports and towards alternative energy. First came fiscal reform, followed in January this year by the announcement of a halt to any new oil and gas exploration contracts, as part of a commitment to combat climate change.

Despite, this decisive move, Colombia hasn’t abandoned fossil fuels; a key element of the government’s plan for long-term energy security is for the country to become self-sufficient in gas. To make this happen, investment in new projects will be needed, since if current fields continue their current level of decline, a supply gap for domestic gas will open up before the end of the decade. New offshore developments will need to be highly productive and cost effective to be profitable, and significant infrastructure investment will be required.

To find out more about the broader outlook for upstream oil and gas in Colombia, sign up for our Colombia research series.

What are the challenges to upstream growth in Latin America?

Overall, there is no doubt that Latin America offers diverse opportunities for oil and gas companies of all stripes. However, the sector must address a series of challenges to ensure success.

Efficient technology and effective project execution will continue to be critical to add production rapidly and maximise the productivity of wells. Infrastructure investment will also be crucial since pipeline takeaway capacity is currently a key limitation to production growth. Meanwhile, mitigating decline in mature countries will also be essential, to avoid falling supply from mature fields hampering the steep overall production growth required. The lifting of US sanctions on Venezuela should contribute to production recovery there and would be a positive signal in that respect.

Remember to complete the form at the top of the page to download the webinar recording. This includes deeper analysis of which countries and resource themes in the region are best positioned to thrive, as well as discussion of promising areas for exploration and a look at the next bid round opportunities.