Find out how our Consulting team can help you and your organisation

Turning tide for offshore supply chain markets

1 minute read

Malcolm Forbes-Cable

Vice President, Upstream and Carbon Management Consulting

Malcolm Forbes-Cable

Vice President, Upstream and Carbon Management Consulting

Malcolm is an expert in strategy development, transaction support and the energy transition.

Latest articles by Malcolm

-

Opinion

Five key takeaways from our Gastech 2025 Leadership Roundtables

-

Opinion

The UK's critical role in Europe's integrated oil system

-

The Edge

No country for oil men (and women)

-

Opinion

The Norwegian emissions dilemma

-

Opinion

The case for developing UK's oil and gas resources: Rosebank and Cambo fields

-

Opinion

Scotland the brave: a Firth of Forth net zero hub for COP26?

In our recent perspective ‘The oilfield supply chain: the future isn’t what it used to be’ we identified 2017 as the bottom of the market: the supply chain was on its knees with no more to give. With oil prices rising on the back of tightening fundamentals and ratcheting geo-political tensions the oil market has turned a corner; however, whilst this news points to a sunnier future, the current reality for many supply chain companies is of low volume and cut throat pricing. But are there signs that this is starting to change? What evidence is there of a tightening market and a shift in pricing power from operators to suppliers?

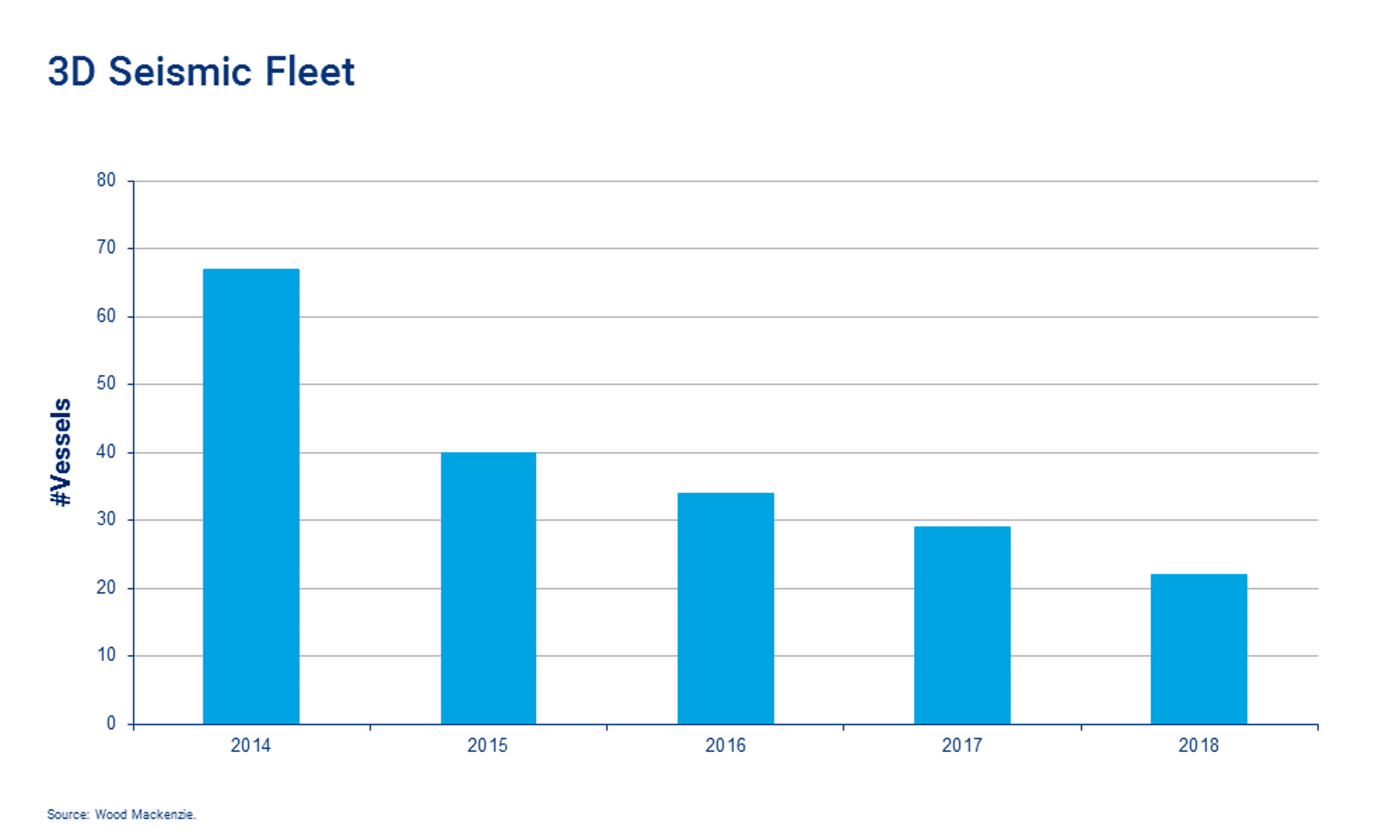

One of the first signs we have seen of a recovering offshore market and improving financial health has been in the harsh environment rig market. Benefitting from being more contained than other segments of the rig market we have seen day rates climb by 40-50% from the 2017 lows. Awilco’s new-build order has been an additional fillip for the sector. Less evident in rate terms but nicely poised is the 3D seismic fleet which has dramatically reduced supply since the 2013 peak. Pre-2014 there were in excess of 80 3D vessels active in the market. Last year this fell to ~29 and in 2018 there is an active fleet in the order of 22 vessels.

{kind=link}

By any measure this is a precipitous decline however, as we go into the Northern Hemisphere summer, it's worth noting that the fleet is fully contracted. There are some laid-up vessels that can enter the market in short order but others will require substantial investment to return to service. This investment is a material commercial hurdle that will only be met through significantly higher rates. The stage is therefore being set for a recovery and with rates at or near operating costs this correction will be welcome relief for the beleaguered 3D seismic players.

Furthermore recent exploration success has been concentrated in offshore frontier basins: since 1st January 2018 80% of the 3 bnboe discovered volumes were made in frontier acreage. A few more positive signals like this and we should expect to see increasing offshore seismic activity. Welcome wind in the sails.