What a second wave of lockdowns would mean for Asia’s oil and gas markets

Asia’s import-dependent energy markets would benefit from lower prices, but at the cost of weaker economic growth

1 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

As countries have gradually re-emerged from lockdown, a second wave of Covid-19 infections remains a major worry. Over the past month, governments from Europe to Japan, Australia to India have moved swiftly to contain any localised re-emergence of coronavirus. The hope is that with quick action, local outbreaks will not lead us back to the drastic nationwide lockdowns we all experienced through the first half of 2020.

In their recently published H1 2020 commodity outlooks, Wood Mackenzie’s oil and gas teams include two critical assumptions on the pandemic: that containment measures are broadly effective (with only localised lockdowns where required) and an effective vaccine is available by mid-2021. This results in global GDP rebounding to 4.6% growth in 2021 from -4% in 2020. Economic and energy demand growth then broadly trend back to pre-coronavirus levels.

Bold assumptions, but not unrealistic. But what would happen with a second wave of prolonged, nationwide lockdowns? What would this mean for economic activity? How will oil and gas supply and prices be affected? Will Asia’s demand-led recovery be blown off course? Wood Mackenzie’s oil and gas teams have used our proprietary global oil and gas models to assess what a second wave of lockdowns could mean.

Read more: A second wave of coronavirus lockdowns: implications for oil and gas markets

A coronavirus-lockdown second wave case

In our H1 2020 base case, Q2 2020 was the nadir of the global economy. As restrictions are lifted, economies do what they do best, they grow. Critically, this assumes no mass second wave of lockdowns and that a vaccine is delivered in Q2 2021.

Based on this, our oil and gas teams anticipate prices rebound as demand recovers through H2 2020 and into 2021. The recovery in oil prices is proportionally stronger than for gas, primarily related to long-anticipated LNG oversupply.

This is a positive outlook and so must come with a health warning. With the easing of restrictions in recent months, Covid-19 infection rates have quickly started to rise in many parts of the world. The outlook could rapidly deteriorate.

Given this, we have developed a coronavirus-lockdown second wave (CSW) case that sees measures to ease lockdown stalling globally by Q4, and a return to strict and widescale lockdowns in H1 2021. Restrictions are then not eased until the second half of next year and a vaccine isn’t available until the end of 2021. Consequently, GDP falls more sharply in 2020 to -8%, with no return to positive growth until 2022.

What this could mean for oil markets and prices

From the lows of March, oil prices have begun to recover as supply has been cut and demand has rebounded. We now expect Brent to reach US$50/barrel by the end of the year and to rise above US$80/barrel in real terms by 2030. In our CSW case, prices continue to trend upwards – supply being affected more severely than demand in both cases. But with a longer recovery and slower demand growth, Brent only climbs to around US$70/barrel real by the end of the decade.

In terms of demand, efforts to reduce oil consumption see demand declining across the OECD and China by 2030 in both the H1 base and CSW cases. But the downward revision to GDP in the CSW case hits the freight sector in particular. Oil demand in Asia is not immune, though the developing economies of India and Southeast Asia in particular benefit from lower prices, supporting a return to demand growth and reducing dollar outflows.

You might be interested in: What forces will shape global gas markets over the next two decades?

Impact on Asia’s gas and LNG markets

A second wave of lockdowns results in global gas demand reducing by 4.4% in 2020 (vs 2019). But the longer-term demand outlook remains robust, underpinned by Asia’s economic growth and switch away from coal. The CSW case only sees a 1.1% reduction by 2030 (vs H1 2020). European and North American gas demand is hit hardest.

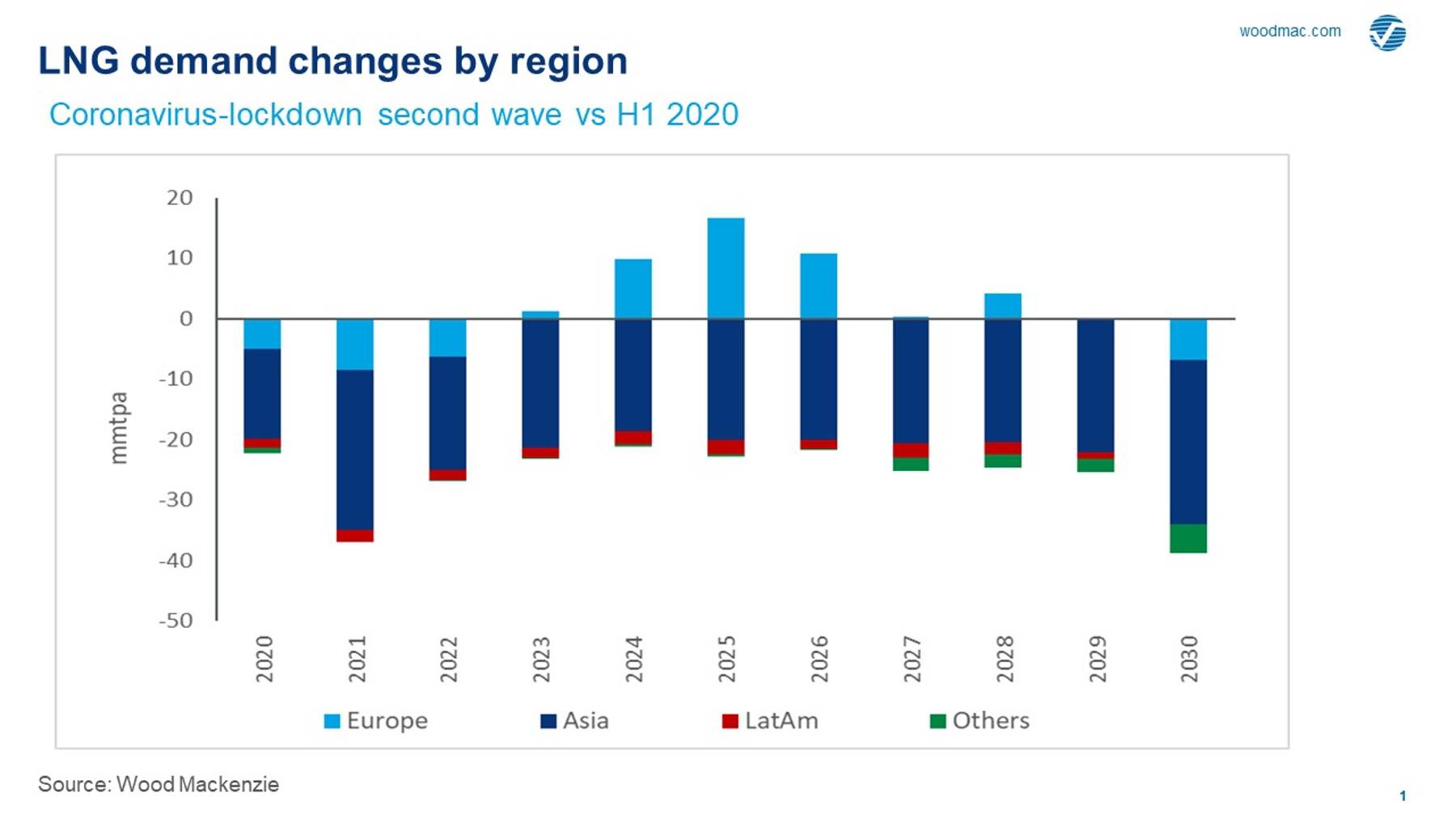

Northeast Asian LNG demand, including China, remains resilient but demand nevertheless falls in the CSW case. Excluding Europe, global LNG demand reduces by around 24 mmtpa between 2020 and 2030 due to secondary lockdown. This is an Asian story, as the chart below clearly illustrates. Asian LNG demand reduces by an annual average of 21 mmtpa over the coming decade in the CSW case.

{kind=link}

Asia’s near-term demand pain puts pressure on Europe

Through the short term, any decline in Asian LNG demand inevitably puts further pressure on Europe to absorb LNG oversupply through to the mid-2020s. Russia seeking to maintain market share will contribute to LNG curtailments, particularly from the US. A second wave of lockdowns would also result in further delays to LNG projects under construction – we expect an additional three-month lag to commissioning on top of delays already included in our H1 2020 outlook.

Pre-FID supply pushed back beyond 2025

The next wave of LNG investment is hit hard in the CSW case. On average, pre-FID projects are pushed back by around two years. We have maintained the assumptions of four Qatari trains, alongside Obskiy LNG, Costa Azul and Corpus Christi taking FID in the next 18 months. No other projects take FID in this timeframe. This delay to new supply is intensified as the new Qatari mega-trains ramp up after 2025, resulting in a paltry supply-demand gap by 2030 of only 15 mmtpa in the CSW case.

For Asian buyers, the CSW case is a double-edged sword. A second wave of lockdowns would ‘flatten’ the Asian LNG spot price, with limited upside as US LNG underutilisation is required to balance the market. Importers and consumers will benefit, and low prices will stimulate more gas demand. But LNG buyers want choice, and with projects delayed, the negotiating strength of producers with uncontracted supply will increase.

APAC Energy Buzz is a blog by Wood Mackenzie Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.