Get Ed Crooks' Energy Pulse in your inbox every week

Buoyant LNG market a sign of the coming recovery

A strong rise in prices in Asia and record US exports show how demand for LNG is bouncing back. Other markets are set to follow

1 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is the competitive power market model broken?

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

On 8 December, 90-year-old Margaret Keenan became the first person to be given a Covid-19 vaccine as part of a mass immunization programme. It was an emotional moment at the Coventry hospital in the UK where she was given the jab, a sign of a better year ahead in 2021. But there are some regions of the world, and some energy markets, where that better future has already arrived.

LNG prices in Asia have risen from lows around US$2 per million British thermal units to over US$9 this month, driven by disruptions to supply from some large projects, including Gorgon and Prelude, and by a robust recovery in demand. Bustling offices, schools and even cinemas in China, South Korea and Japan are reminders to Europeans and Americans, who are still facing lockdowns and high infection rates, of what successful control of Covid-19 looks like.

The growth in China’s gas demand has slowed to 4% this year, but LNG is increasing its share of the market and continues to grow at more than 11%, according to Wood Mackenzie’s short-term LNG service. In South Korea, electricity consumption has rebounded strongly since May, helping to support demand for gas for power generation. And although the recovery in Japan’s electricity use has been weaker, nuclear plant outages have sustained the need for gas-fired generation. Worldwide LNG imports, which in the second and third quarters of 2020 were running below last year’s levels, have jumped back to about 3% above 2019 in the fourth quarter.

For US LNG exporters, the rebound in demand has transformed the immediate outlook. In the spring and summer US export volumes plunged, as prices in Europe and Asia fell to levels that meant offtakers could not cover their variable costs of production and shipping. It is estimated that more than 150 US LNG cargoes were cancelled between April and November, and in July and early August, supplies of gas to US export plants dropped to about a third of their liquefaction capacity.

Now that position has reversed completely, with the rise in LNG prices driving a surge in US exports. This year the US has added capacity to export an additional 2 billion cubic feet per day, with new trains at the Freeport, Cameron and Corpus Christi plants entering service, and Elba Island starting full commercial operations. And with US Henry Hub benchmark gas down at around $2.60 per million BTU, the economics of exports look attractive again. Feedgas deliveries to US terminals have hit new record highs and were running this week at about 11.2 bcf/d, easily surpassing the previous high point of 9.5 bcf/d in March.

The long-term outlook for LNG demand depends on global climate policy. In Wood Mackenzie’s base case forecast, representing what we think is the most likely outcome, by 2040 the world needs an additional 450 billion cubic metres of LNG supply, above the output of plants already in service or under construction. In a scenario with the world on course to limit global warming to 2°C, as opposed to the 3°C implied by our base case, the new LNG supply needed by 2040 could be only about a third as much, at about 145 bcm per year.

In the short term, however, the LNG market is giving us a foretaste of what we can expect for energy demand and prices more generally. Oil faces somewhat different market dynamics. The hit to demand will be longer lasting for oil than for LNG. Wood Mackenzie’s latest long-term Macro Oils outlook projects that world liquids consumption will not return to 2019 levels until the second half of 2022. The large amount of potential supply still being held off the market by the OPEC+ countries, waiting for the right opportunity to bring it back, will weigh on prices. But the price of oil has also been recovering: this week Brent crude nudged over $50 a barrel for the first time since March. As Covid-19 vaccines become widely available, global economic activity, and hence energy use, will rise, which will have the general effect of putting upward pressure on prices.

In brief

Another market with strong recovery in recent months is greenhouse gas allowances in the EU’s Emissions Trading System. The price of the allowances hit a new high on Friday at €31.30 per tonne of carbon dioxide equivalent, above the previous record of €31 per tonne reached in 2006, the year after the system was launched. The price of the December 2020 futures has doubled from its low of €15.30 a tonne in March.

In Phase 4 of the system, which begins in January, the European Commission had planned to cut the number of allowances by 2.2% a year, compared to a 1.74% annual decline in Phase 3, to achieve a 40% reduction in total EU emissions from 1990 levels by 2030. In the small hours of Friday morning, EU leaders agreed a more ambitious goal of a 55% cut, which is likely to mean the total number of allowances will have to be reduced at a faster rate.

The US oilfield services industry has lost more than 81,000 jobs over the past year, according to the Petroleum Equipment and Services Association. Employment in the industry has risen by about 9,300 over the past three months, but that has brought back only a fraction of the 100,000 jobs that the association estimates were lost as a result of demand destruction caused by the Covid-19 pandemic.

New York State’s pension fund has set a goal of net zero greenhouse gas emissions by 2040, and will review its investments in energy companies over the next four years. The review will “assess transition readiness and climate-related investment risk”, and “where consistent with fiduciary duty, divestment of companies that fail to meet minimum standards”. The fund has already divested from 22 coal companies. It is currently wrapping up its evaluation of nine oil sands companies, and it will develop minimum standards for its investments in shale oil and gas. That will be followed by assessments of the integrated oil and gas majors, other E&Ps, oilfield services companies, and midstream businesses.

The New York State fund will monitor the oil and gas companies it holds to check if they “are meeting minimum standards and are on viable low-carbon transition pathways”, and will “increase its engagement efforts with companies across industries to encourage them to reach net zero carbon emissions more quickly”.

Advocates of energy efficiency often lament the inflexible heating systems in apartment buildings in New York and other cities, which leave radiators on for much of the year whatever the weather, forcing apartment dwellers to throw open a window to cool down. A fascinating article in Bloomberg CityLab explained that this was actually a deliberate design feature, prompted by the Great Influenza of 1918-20 because with the flu, as with Covid-19, circulation of fresh air can help prevent the spread of infection.

QuantumScape, a company with an innovative solid-state lithium metal battery technology, joined the stock market through a merger with a special purpose acquisition company last month, and its shares have soared since then. This week, it issued performance data that it said showed that its technology “addresses fundamental issues holding back widespread adoption of high-energy density solid-state batteries, including charge time (current density), cycle life, safety, and operating temperature”. QuantumScape batteries could be charged to 80% capacity in just 15 minutes and would allow electric vehicles to have 80% more range than using today’s lithium ion technology, the company said.

Jeremy Grantham, the famous investor who now is now focused on work to address the threat of climate change, made a profit of about $200 million on QuantumScape “by accident” after his foundation invested $12.5 million in the business seven years ago, the Financial Times reported.

And finally: a crash landing for Elon Musk’s SpaceX. The company this week launched a prototype of its Starship rocket, intended carry humans to the Moon and eventually Mars. The take-off and flight went fine, but while attempting to land, the rocket descended too fast and exploded in a ball of fire when it hit the ground. The SN8 prototype “did great”, Musk said, and “we got all the data we needed” for future launches.

Musk revealed this week that he had relocated from California to Texas, to be closer to the launch site and factory for the Starship prototypes, and to the new factory Tesla is building near Austin. He tweeted after the Starship launch: “Thank you, South Texas for your support! This is the gateway to Mars.”

Other views

Simon Flowers — The Euro Majors’ big bet on new energy

Valentina Kretzschmar — The Majors’ energy transition: Corporate New Energy Series

Gavin Thompson — Nuclear: the cleanest dirty word

Romana Adamcikova and Nouran Ezzat — North Sea decommissioning: a turning point lies ahead

Clyde Russell — China scores coal own goal as domestic, import prices surge

Jason Bordoff — How Biden’s climate plans will shake up global energy markets

Quote of the week

“I talked a few days ago to the head of a big oil company. And they understand that changes are coming, and that things need to be done to move to American leadership in these new [energy] technologies… I am listening to what their needs are and how they view the world, so I can begin to understand better what the possibilities may be once the president is sworn in on January 20.” — John Kerry, announced as President-Elect Joe Biden’s climate envoy, explained his outreach to the US oil and gas industry. He said he wanted to build a consensus on addressing the threat of climate change, and argued that markets could be “a very powerful force for good”.

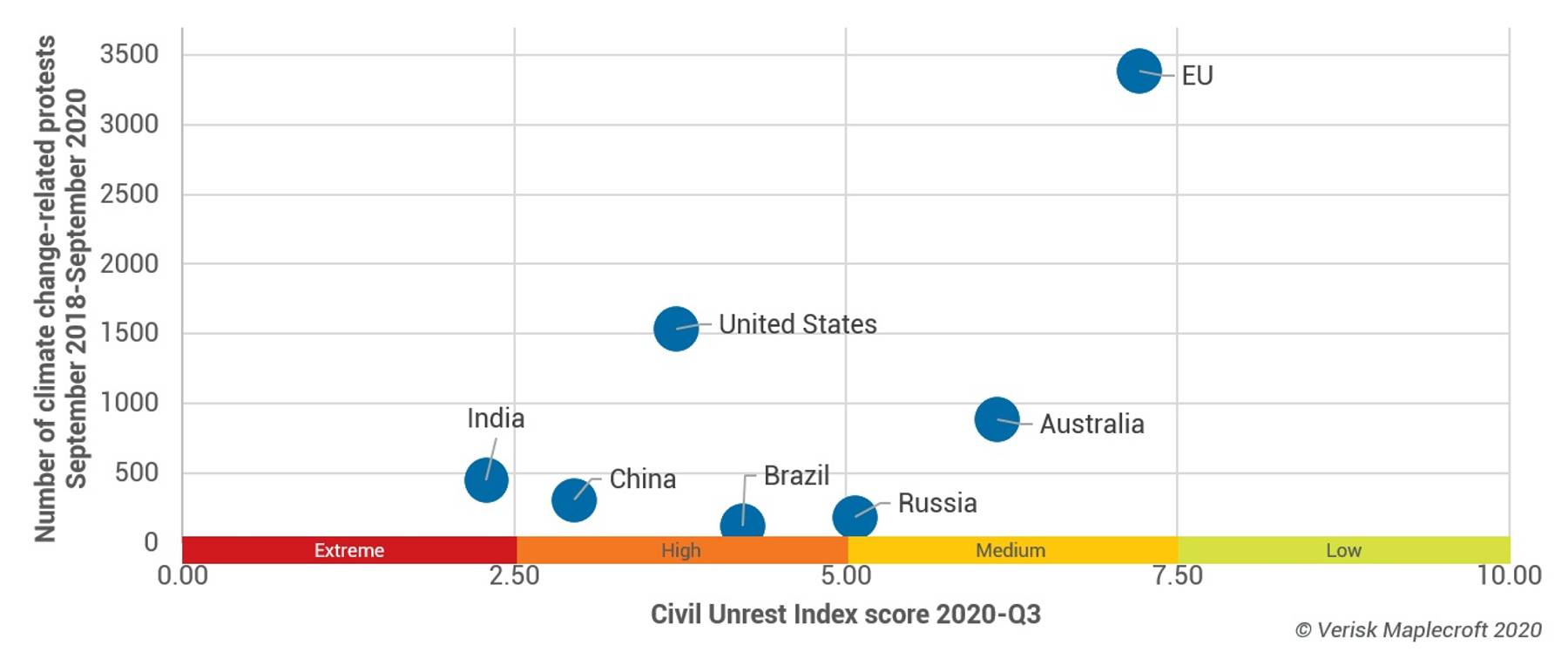

Chart of the week

This chart showing the prevalence of climate protests in selected leading economies comes from Franca Wolf of Verisk Maplecroft, an affiliated company of Wood Mackenzie. It shows on the y axis the number of climate-related protests over the past two years, plotted against a civil unrest index score on the x axis, with a higher score indicating less unrest. The key point to notice is that the EU, the US and Australia have had the most climate protests among this group of developed and emerging economies, but that is not simply because they see more demonstrations in general. China and India, for example, are countries that are more exposed to civil unrest, but they have seen relatively few climate protests. The chart illustrates that it is people in richer countries who are generally the most highly motivated to take political action on climate change.

{kind=link}