Sign up today to get the best of our expert insight in your inbox

Geothermal revolution approaches critical moment

Fervo Energy is close to starting up its first large-scale enhanced geothermal systems plant

1 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

-

Opinion

Carbon capture continues to grow, despite challenges

SpaceX, Elon Musk’s space technology and AI company, joined the Nasdaq market in a record-breaking IPO last week, raising US$75 billion. Since then, the shares have been volatile. But as of Thursday night, they were still 37% above their issue price, giving SpaceX a market capitalisation of about US$2.4 trillion.

The success of SpaceX has wide-ranging implications for energy. Musk is committed to developing data centres in space, a strategy assessed by my Wood Mackenzie colleague Robert Liew in a report that we published last week.

But some in the energy industry think that another IPO in the past month might be even more significant. Fervo Energy, a pioneer in enhanced geothermal systems (EGS), joined the Nasdaq in May, in one of the largest low-carbon energy IPOs on record, raising about US$1.9 billion.

Fervo does not yet have a single large-scale project in operation. But it has caused excitement because of its potential to revolutionise the geothermal industry, using the technologies of unconventional oil and gas production.

Conventional geothermal power systems rely on water naturally flowing through hot rock underground. They work only where the right conditions exist, in specific areas including parts of Indonesia, the Philippines and western states in the US.

By using horizontal drilling and hydraulic fracturing, Fervo’s enhanced geothermal system is able to flow hot water through rocks with much lower natural permeability. That makes geothermal power generation possible in a wider range of locations.

An injection well is used to pump cold water into the formation, where it heats up and flows to a production well. The hot water and steam come to the surface, where they heat another liquid, an organic fluid used to turn a turbine. The produced water can then be reinjected and used again.

If the EGS technologies being pioneered by Fervo and other companies can be made to work at scale, they could have huge advantages, providing 24/7 dispatchable power with zero carbon emissions. They are particularly attractive for the US, because the technologies build on America’s comparative advantages in horizontal drilling and hydraulic fracturing for oil and gas production.

Fervo has a wide range of backers and partners, including the E&P company Devon Energy and the hydraulic fracturing firm Liberty Energy, where the current US energy secretary Chris Wright was previously chief executive.

That combination of attributes has helped build support for next-generation geothermal energy across the political spectrum in the US.

Besides Fervo, several other companies are developing EGS, including Sage Geosystems, 400C Energy and Ormat.

Other companies, including Eavor, are developing advanced geothermal systems (AGS), which are similar but circulate water around a closed loop, and do not require hydraulic fracturing. And some are specialising in particular segments of the value chain, including Quaise, which has innovative drilling technology using millimetre waves to bore wells for geothermal plants.

Electricity from these pioneering EGS and AGS companies is attracting interest from utilities and other buyers that have emissions goals to meet but still need dispatchable power.

The big tech hyperscalers are among those buyers. They have demanding targets for cutting emissions, but often require “five nines” reliability for their data centres, meaning that they are available 99.999% of the time. Meta and Google have been the most active in partnerships with EGS companies. Google was the ultimate offtaker for Fervo’s first project, a small 3.5-megawatt plant in Nevada called Project Red.

All eyes are now on Fervo’s first large-scale project, Cape Station in Utah. The 100-MW first phase is expected to come online early next year, followed by the 400-MW Phase 2 in 2028.

Project Red started producing electricity back in November 2023, and has logged over 600 days in operation. But until Cape Station has a demonstrated track record , investors will inevitably see some uncertainty around EGS execution risk.

The regulatory framework for enhanced geothermal projects can also be an issue. Securing permits can be a lengthy process and may face resistance in areas that oppose hydraulic fracturing. Supporters of the industry have put forward the case for regulatory reform to expedite development.

Even so, EGS undeniably has a favourable wind at its back. Many people across the energy industry and across the political spectrum will be hoping that the new geothermal techniques can succeed.

The Wood Mackenzie view

Although it is still early days for EGS, Wood Mackenzie analysts agree that the technology’s prospects look bright.

Our estimates for the levelised cost of electricity (LCOE) suggest that in the US, EGS plants will be significantly higher-cost than solar or wind power, but highly competitive against other dispatchable technologies such as gas-fired power plants.

International comparisons are also noteworthy. China is typically the world’s lowest-cost producer of electricity from most generation technologies, from gas to nuclear to renewables. In EGS, however, it is North America that is currently the lowest-cost region, because of its expertise in hydraulic fracturing and horizontal drilling. China’s EGS costs are projected to fall over time, but only a little below North American levels, and will remain broadly similar into the 2030s and beyond.

However, two important considerations should be taken into account when assessing the prospects for geothermal energy. One is the social licence to operate. Kate Adie, a Wood Mackenzie analyst who covers the geothermal sector, says EGS is most likely to scale up quickly in the US, where many parts of the country are already comfortable with the idea of hydraulic fracturing and horizontal drilling.

In some parts of the world, the mere mention of “fracking” might be enough to build momentum for a ban on EGS, despite its advantages as a source of zero-carbon power.

The other key consideration with EGS is that – like other emerging zero-carbon electricity technologies, including small modular reactors, nuclear fusion and long-duration storage – it is unlikely to make a material difference to the immediate challenges faced by the energy system.

Worldwide, next-generation geothermal projects have been announced with a total capacity of about 1.9 gigawatts, according to Wood Mackenzie data. In our base case forecast, worldwide annual geothermal generation is projected to rise by about 22 terawatt hours, or about 40%, between 2026 and 2035.

Over the same period, annual global power demand is expected to rise by about 9,000 TWh. So the forecast increase in geothermal production, which includes both conventional and EGS projects, meets only a little over 0.2% of the increase in global power consumption.

That said, in the right places and at the right times, EGS could be very useful. It is a familiar story: no single technology can meet every need. But a diverse toolkit of solutions will be essential for tackling the challenges the system faces.

Tensions emerge after the US and Iran agree deal to end conflict

Last weekend, the US and Iran agreed a Memorandum of Understanding to end the war that began 28 February, with the aim of starting a 60-day period of negotiations to lead to a lasting peace.

On Wednesday, President Donald Trump said the alternative to the agreement would have been “a worldwide depression” caused by the loss of energy supplies previously exported through the Strait of Hormuz.

The full text of the 14-point MoU has now been published. Key provisions include an end to all fighting, including in Lebanon, the reopening of the Strait of Hormuz within 30 days, a US$300 billion reconstruction fund for Iran, to be backed by partner countries in the Gulf region, and an end to international sanctions on Iran once the final peace deal has been agreed.

Wood Mackenzie’s VesselTracker service recorded an increase in traffic through the strait in the days after the deal was announced, albeit nowhere near pre-war levels.

However, there have been emerging signs of strain on the newly agreed peace deal. The Iranian news agency Fars reported suggestions that Iran would not enter negotiations about a long-term peace agreement until the fighting ends in Lebanon. Israel and Hezbollah have clashed repeatedly during the week, exchanging missile, drone and bomb attacks.

Oil prices rose slightly in response to those reports. Brent crude, which at one point on Thursday dropped below US$77 a barrel, was trading at about US$80 a barrel on Friday morning.

FERC issues orders to expedite grid connections for large loads

The US Federal Energy Regulatory Commission (FERC) has launched its long-awaited plan for expediting grid connections for new large loads such as data centres. The regulator has issued a set of orders to the six US regional grid operators, calling on them to either justify or reform the rules they use for connecting large loads to the grid.

The orders follow a directive from Chris Wright, the energy secretary, last October. He called on FERC to find ways to accelerate “speed to power” for new data centres and factories, to support the development of AI and manufacturing capacity in the US.

Laura Swett, the FERC chairman, said the regulator’s goal was to transform “the way large energy users access the grid”. Because the six regional grid operators all differ in their load connection procedures, market design, stakeholder composition and geography, FERC is issuing each one with a specific targeted order, rather than attempting a blanket ’one-size-fits-all’ solution.

The common themes running through the orders include developing efficient study processes for proposed transmission projects, requiring transparency in transmission costs, accommodating co-location agreements and behind-the-meter generation, and providing new transmission services for large loads that can offer flexible demand.

Other views

Johor's data centres could consume 40% electricity demand by 2035, testing grid expansion plans

Data centre metals demand isn’t an asset story. It’s a grid story

EU carbon storage target falls 35% short as value-chain fragmentation constrains NZIA 50 mtpa goal

Trump’s ‘nuclear bros’ race to deliver US atomic revival – Jamie Smyth

A frontier without an ecosystem is not stable – Satya Nadella

Quote of the week

“We run out of reserves in about four weeks. You know, there are reserves all over the world, and we would really run out, and there’d be a time when you wouldn’t be able to get it. And you want to see Bedlam…?”

US President Trump explained the thinking behind his decision to sign the Memorandum of Understanding with Iran to end the war in the Middle East.

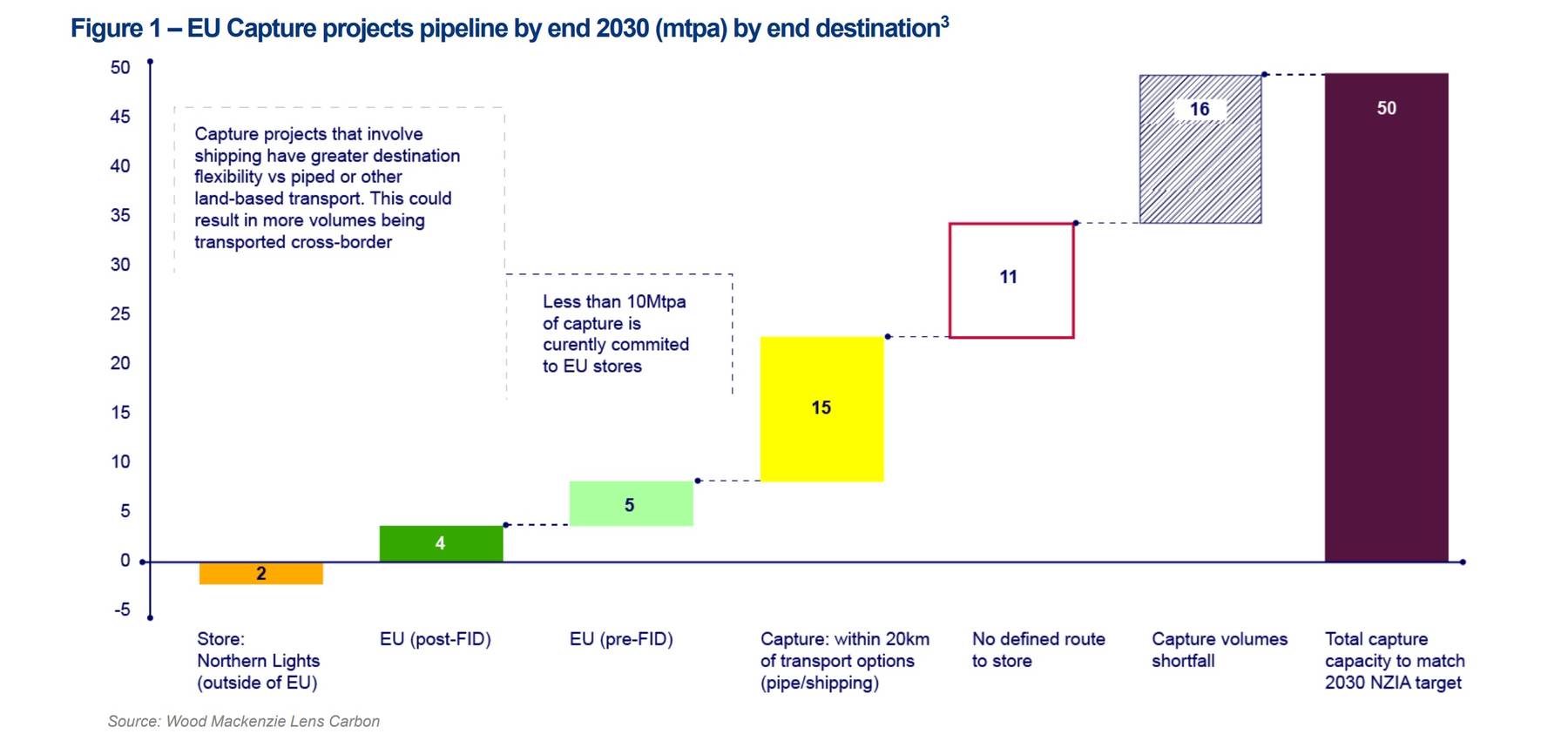

Chart of the week

This comes from a recent Wood Mackenzie analysis looking at the feasibility of complying with the EU’s carbon capture target mandated by the Net Zero Industry Act.

It illustrates the key point in that analysis. Even in a highly optimistic scenario, where all the projects in advanced stages of development progress as planned, the EU will still face a storage shortfall in 2030 of at least 17.5 million tons per annum (mtpa) of carbon dioxide, about 35% of the 50-mtpa target.

Download the full 14-page report for a more detailed analysis with a case study of a key project.

{kind=link}