Interested in learning more about our gas & LNG solutions?

What will the gas market look like in a net zero world?

Gas and LNG have an important role to play in realising a 1.5-degree scenario by 2050 – but the resulting market would be nearly unrecognisable

3 minute read

Kateryna Filippenko

Research Director, Global Gas Markets

Kateryna Filippenko

Research Director, Global Gas Markets

Principal Analyst with a focus on the European gas market and the development of alternative scenarios.

Latest articles by Kateryna

-

Opinion

Biomethane price puzzle: why demand-side policy is the missing piece

-

Featured

Gas & LNG: region-by-region predictions for 2026

-

Opinion

Europe gas & LNG: 5 things to look for in 2026

-

Opinion

FuelEU Maritime: a catalyst for bio-LNG market growth

-

Opinion

Green gains: inside the rise of North American renewable natural gas

-

Opinion

Gastech 2024: Our top three takeaways

The global gas and LNG market faces a number of ‘great unknowns’. With the market in turmoil uncertainty abounds – from the scale of the current energy crisis to the long-term impact of decarbonisation. What will demand look like in different regions if the world succeeds in getting onto a 1.5 °C pathway? How big are the investment opportunities? What will the trade flows look like in a net zero world?

We tackled these questions and more in a new report – Accelerated energy transition 1.5-degree scenario: global gas industry in a 2050 net zero world – which draws on our proprietary Global Gas Model Next Generation. Read on for an introduction – the full report is available to subscribers to our Global Gas Service.

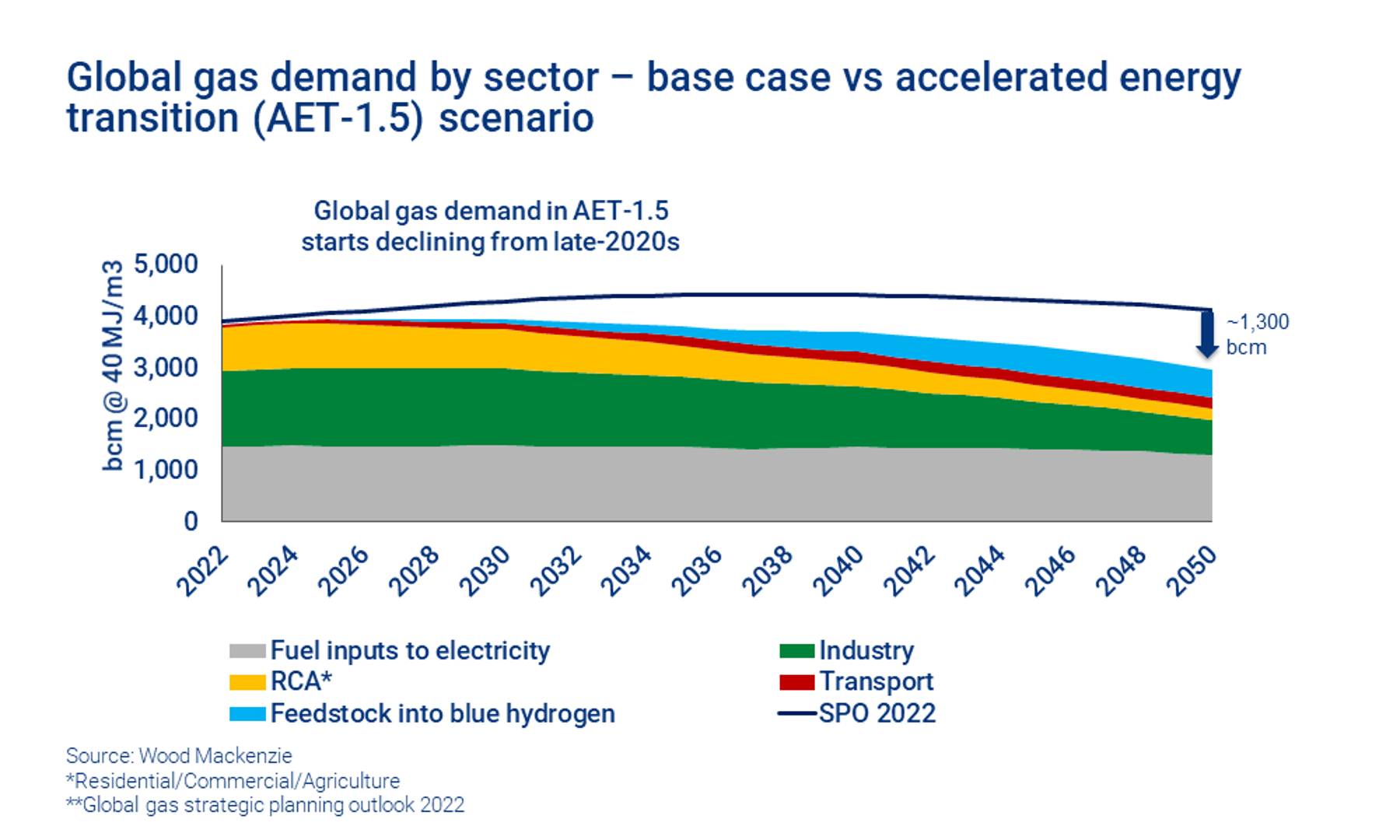

Gas demand remains resilient – if it can decarbonise

The energy transition is a truly transformative force. Our accelerated energy transition scenario (AET-1.5) explores a pathway on which the rise in global temperatures since pre-industrial times is limited to 1.5 °C by the end of this century, and we reach global net zero by 2050. Under AET-1.5, hydrocarbon demand declines rapidly, except for natural gas.

While decarbonisation measures undoubtedly put pressure on end-use energy demand, gas still has a crucial role to play. The phase-out of coal supports gas, and there’s also a growing need for gas as a feedstock for blue hydrogen. And, crucially, with widespread electrification and buildout of renewables, gas paired with carbon capture and storage (CCS) can be a source of flexibility and dispatchable generation – even as battery technology is advancing.

However, this is only possible if CCS technology improves, allowing for an efficient, low-cost method of reducing emissions from gas.

Timing is everything as the future of gas unfolds

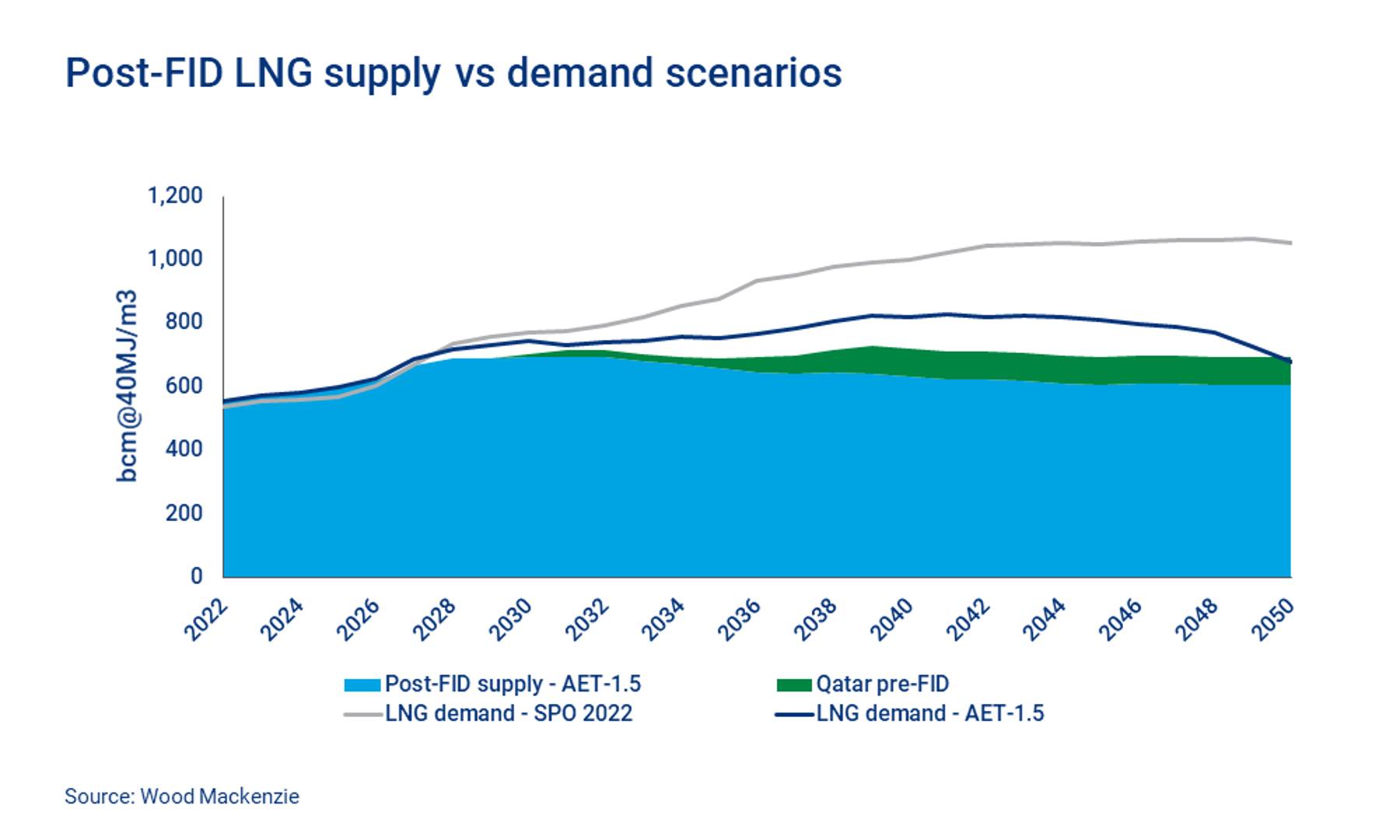

Near-term gas and LNG investment is still needed as Europe pivots from Russian gas. Russia’s war with Ukraine sparked a massive shift in the global gas market – much of it irreversible. Demand for LNG in Europe in particular has soared.

However, a raft of FIDs – which has already begun and is likely to continue into the next year – will fill up this space quickly. As our Q3 LNG FID tracker notes, FID momentum has continued after the 50 mmtpa of new capacity that was sanctioned in 2021. So far this year 26 mmtpa has been sanctioned in the US and 2 mmtpa outside. Venture Global’s 13 mmtpa Plaquemines Phase 1 (13 mmtpa) and Cheniere’s Corpus Christi Stage 3 (>10 mmtpa) have been sanctioned in Louisiana. New Fortress Energy has ordered long lead items for three of its Fast LNG units – one for Congo (1.4 mmtpa) and two for offshore Louisiana (2.8 mmtpa total). Based on recent long-term contracts signed, more than 100 mmtpa of new LNG supply could be sanctioned in the next two years, with the majority of activity on the US Gulf coast. This activity – coupled with continued expansion in Qatar – increases the risk of oversupply in the late-2020s/early-2030s in an AET-1.5 scenario. The window of opportunity will open again after that as Asian demand continues to grow, but will be limited by long-term gas demand reduction.

{kind=link}

{kind=link}

The global gas market looks very different in a net zero world

Longer term gas demand decline is unavoidable in a 1.5 degree pathway. And the market could become more competitive and dynamic as green commodities for decarbonisation, such as hydrogen and ammonia, enter the market in big way.

Inevitably lower prices and demand uncertainty would impact multi-billion dollar investments into major fixed infrastructure projects – such as new large-scale international pipelines. Low prices would also challenge the economics of high-cost unconventional upstream developments and reduce the appetite for further exploration. Existing infrastructure assets may go underutilised as the market contracts faster than some assets reach the end of their lives.

The competitiveness of supply projects would likely be assessed very differently in an AET-1.5 scenario. Carbon offsetting and innovative commercial offerings will come into sharper focus. Broadly, company strategies, policies and investor attitudes may change, leading to a very different set of trade flows and reshaped commercial relationships. Our global gas and LNG experts will be tracking the evolution of the market closely.

Explore the shifting landscape of the global gas market in a net zero world in more detail

Accelerated energy transition 1.5-degree scenario: global gas industry in a 2050 net zero world delves into regional demand forecasts, price relationships and changing trade patterns in more detail. The full report is available to subscribers to our Global Gas Service.