Sign up today to get the best of our expert insight in your inbox.

How the Iran war could change energy markets

Implications for longer term oil and gas demand

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

Can US success in tight oil and shale gas go global?

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash leads a team of analysts designing research for the energy transition.

Latest articles by Prakash

-

The Edge

Will falling populations reshape energy demand?

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Africa

-

Opinion

Energy transition outlook: Middle East

Jom Madan

Principal Analyst, Scenarios & Technologies

Jom Madan

Principal Analyst, Scenarios & Technologies

Jom works on scenario modelling for country and global-level energy mixes across all major energy commodities

Latest articles by Jom

-

Opinion

Energy transition outlook: Americas

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Middle East

-

Opinion

Energy evolution: navigating the path to a sustainable future

Lindsey Entwistle

Principal Analyst, Energy Transition

Lindsey Entwistle

Principal Analyst, Energy Transition

Lindsey provides analysis and insights into global policy, regulations and disruptive technologies.

Latest articles by Lindsey

-

Opinion

Energy transition outlook: EU

-

Opinion

Energy transition outlook: Americas

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: UK

-

Opinion

Energy evolution: navigating the path to a sustainable future

The inherent risk to economies relying on oil and LNG shipped from the Gulf has been laid bare. Could supply disruption and the high prices triggered by the war be the last straw for countries that depend heavily on hydrocarbon imports?

In a recently published new scenario, our Energy Transition experts – Prakash Sharma, Jom Madan and Lindsey Entwistle – consider what happens if the war in Iran proves to be the catalyst for hydrocarbon-importing countries to push hard for energy independence. I asked them about the implications, including for oil and gas demand.

What problem has the war exposed?

The vulnerability of economies with energy systems that are heavily dependent on imported oil and gas. The Iran war comes not long after the economic turmoil caused by the Russia-Ukraine war. Both conflicts politicised oil and gas supply, inflicted supply insecurity, high prices and extreme price volatility.

The Strait of Hormuz blockade, which began five weeks ago, halted 15% to 20% of global oil and LNG flows and pushed Brent crude above US$100 per barrel while LNG spot prices have doubled. These wholesale prices flow rapidly through the economy to consumers at the pump, into their gas and electricity bills, and indirectly to a wide range of food products, goods and services. Import-dependent countries are hit disproportionately.

What measures are governments taking?

So far, a few particularly exposed import-dependent Asian countries have taken emergency demand-side measures: mandatory work-from-home and fuel rationing, industrial users facing curtailment orders with essential sectors prioritised.

This is the thin end of the wedge. In the next two to three months, shortages will ripple out through Asia and into Europe and even the US. Europe and Asia will become increasingly reliant upon their strategic reserves to sustain supplies of oil and refined products. In the power sector, most countries have alternatives to keep the lights on – more coal-fired generation and nuclear plants running harder. But these measures are minor adjustments to the immediate crisis and can only be a temporary fix.

Is there a sustainable solution?

If countries are prepared to use the crisis to push harder towards energy independence, then the obvious answer is aggressive electrification. Achieving energy independence, though, requires governments to bite the bullet. They would have to enact policy to accelerate the shift to an economy powered by electrons and away from the current dependence on imported oil and gas molecules.

Even if governments were to commit to such a strategy, change on the ground can’t happen overnight. In our integrated modelling analysis, change starts to take hold only after 2030: electrification accelerates, coal retirements are deferred and renewables expand. After 2040, nuclear power and supporting supply chains rapidly scale. Road transport power demand surges 57% as EVs achieve a dominant market share and oil demand in transport drops 30%, relative to our current base case.

Sustainable in one sense, less so in another – the scenario leads to higher energy-related net emissions. After dropping by 4% due to supply outages in the Gulf, resilient coal demand lifts cumulative emissions above our base case from the late 2020s through to 2040.

What’s the impact on global oil and gas demand?

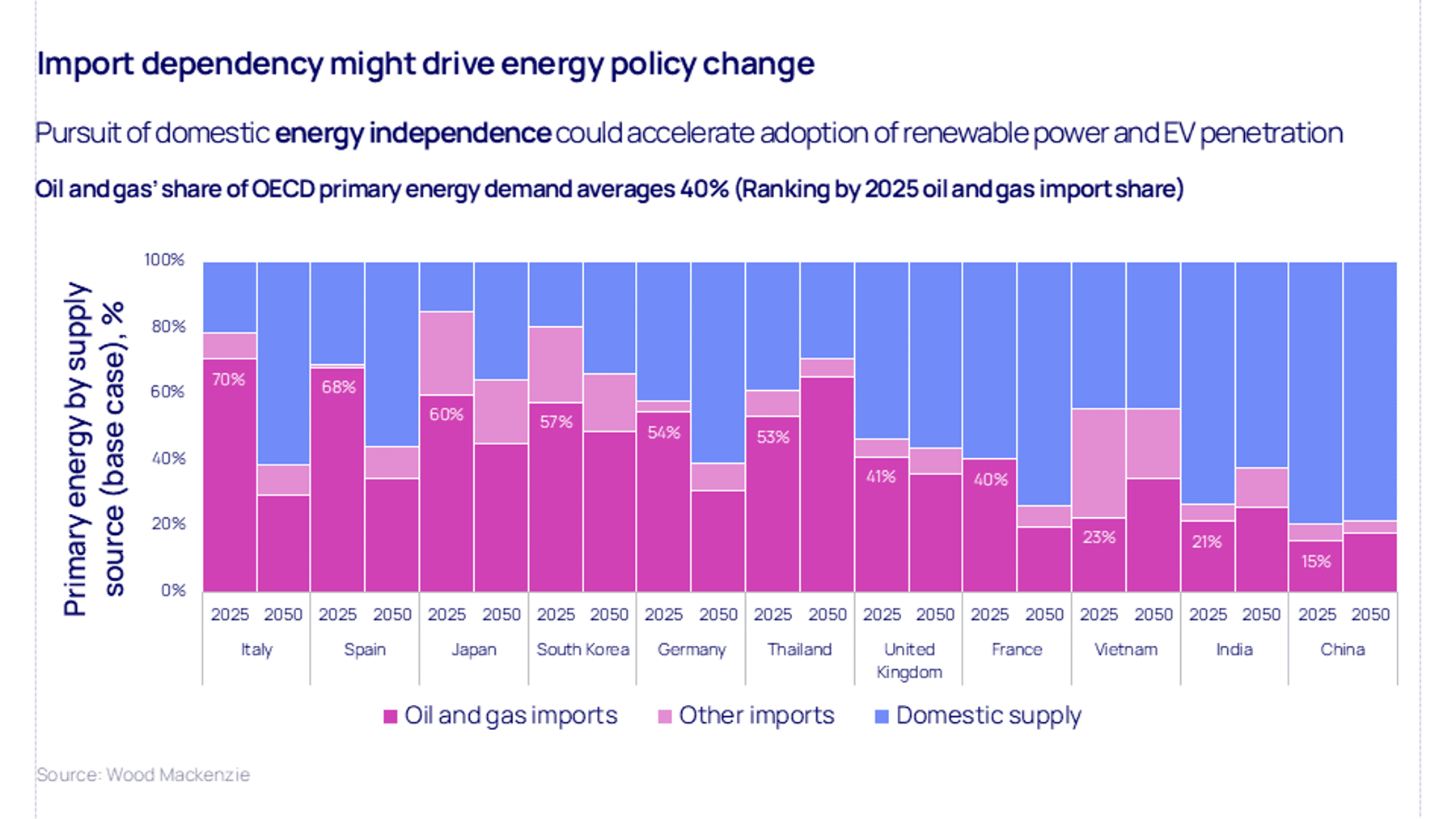

Significant for both. The scenario driver is that import-dependent countries halve imports of oil and gas by 2050. We recognise that complete elimination is unrealistic in this timescale, given hydrocarbons’ grip on some sectors of the economy.

In the scenario, global oil demand falls to 95 million b/d by 2040, 8% lower than our latest base case and 75 million b/d by 2050, 20% lower. Global gas demand falls by 10% by 2050. LNG trade could still form a substantial part of the mix, but countries might diversify sources of supply and optimise portfolios.

What’s stopping countries going faster down this path?

Energy independence won’t come cheap – huge investment will be needed to build out a domestic electron-based energy system. Almost inevitably, this will come at a price premium compared to the optimised global hydrocarbon supply chains built up over decades.

Even so, with electorates feeling the pressure from soaring prices, the crisis presents an opportunity for certain import-dependent economies to strike while the iron is hot. Some countries will have more fiscal capacity to go down this route than others – many governments’ finances are already stretched after dealing with the effects of Covid-19 and the Russia-Ukraine war.

The oil and gas industry has a vested interest in ‘staying relevant’. Governments that commit to energy independence must recognise that the going could get tough if oil and gas prices fall back to competitive levels.

Who stands to win?

China looks to be an out-and-out winner. It has plentiful coal, as well as a material domestic oil and gas resource, and can leverage its dominant existing cleantech platform. That may, however, prompt importing nations to invest in domestic cleantech value chains and manufacturing rather than simply swap one form of dependence for another.

{kind=link}

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.

Sign up today using the form at the top of the page.