Discuss your challenges with our solutions experts

Extended production cuts show OPEC's enduring influence over oil

It has been written off many times, but the oil producers' group remains relevant. In the long term, its influence could grow

9 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

-

Opinion

Carbon capture continues to grow, despite challenges

Dune, a science fiction allegory about the Middle East and oil that in its film version is currently filling cinemas around the world, has often been praised for its almost supernatural prescience. First published in 1965, the novel seemed to anticipate the oil shocks and energy crises of the 1970s.

But already while Frank Herbert was writing Dune in the early 1960s, there had been a series of signs indicating the growing geopolitical importance of energy, including the formation of OPEC in 1960. He was not so much a prophet as a first-class analyst.

The decision by several OPEC+ countries to extend their existing production cuts through the second quarter of 2024, announced last weekend, is a sign that some of the features of the energy landscape he observed remain intact. Despite some fundamental changes over the past six decades, including the downfall and then revival of the US as the world’s largest producer, the OPEC countries in the Middle East continue to play a unique role in managing global oil markets. Projected shifts in oil supplies over the coming decades suggest that influence is only going to grow.

The OPEC statement issued last Sunday listed seven countries as extending the voluntary production cuts first announced last April – Saudi Arabia, Iraq, the United Arab Emirates, Kuwait, Kazakhstan, Algeria and Oman – and an additional cut from Russia.

In practical terms, however, most of the burden of curbing production has been borne by the four countries from the Gulf region: Iraq, the UAE, Kuwait and, above all, Saudi Arabia. From recent peaks in the third quarter of 2022, liquids production has dropped by about 550,000 barrels a day for Iraq, 250,000 b/d for the UAE, 380,000 b/d for Kuwait, and 1.8 million b/d for Saudi Arabia, on Wood Mackenzie’s estimates.

Over the same period, Russia’s liquids production has dropped about 210,000 b/d, although there is some uncertainty over the data because of international sanctions and methods used by oil exporters to evade them.

Ann-Louise Hittle, Wood Mackenzie’s head of Macro Oils, says the decision to extend the voluntary production cuts should have a “dramatic” impact on the short-term oil market outlook. Demand is growing strongly this year: we expect an increase of about 2 million b/d for 2024 as a whole. But non-OPEC supply has also been growing, particularly in the US, Brazil and Guyana.

Extending the cuts will accelerate the expected drawdown from global oil stocks. Wood Mackenzie had forecast that without the extension, the implied stock draw would be about 600,000 b/d in the second quarter. With the extension, we expect the draw to be about 1 million b/d greater than that.

The announcement seems to have been effective. Brent crude was trading at about US$84 a barrel on Friday morning, having been on a gently rising trend since the end of last year. If demand remains healthy, we think the cuts could start to be unwound gradually later in the year.

For the longer term, we expect those core OPEC countries in the Middle East, and Saudi Arabia in particular, to be able to play a continuing role in managing the market. Wood Mackenzie’s most recent Investment Horizon Outlook for oil, published last November, projected that growth in total non-OPEC production would slow by the end of the 2020s, and turn into outright declines in the 2030s, as the core US tight oil inventory starts to deplete. As a result, OPEC’s share of the oil market is set to grow.

OPEC has many times in recent years been pronounced dead, killed off by the US tight oil boom. But it remains influential today, and could be even more influential in the future as US production starts to decline. The geopolitical issues around oil and the critical importance of the Middle East will be just as relevant as they were when Frank Herbert first realised their significance more than 60 years ago.

Satellite methane detection takes a giant leap

The most advanced satellite yet designed for detecting methane emissions was successfully deployed in orbit this week. MethaneSAT was developed by the Environmental Defense Fund (EDF) and is backed by a consortium of companies, environmental groups, research institutes and the government of New Zealand. It will be able to identify and measure methane emissions over wide areas, generating data that will be made available to the public free of charge.

The EDF last year joined forces with Bloomberg Philanthropies and other environmental groups, as well as the UN Environment Programme and the International Energy Agency, to launch a new initiative that will track and analyse methane data to monitor progress towards emissions reduction goals, push for stronger regulation and work on solutions for cutting leakage.

Michael Bloomberg, the UN secretary-general’s special adviser on climate ambition and solutions, said the goal in collecting and sharing the MethaneSAT data was “bringing more transparency to the problem, giving companies and investors the information they need to take action and empowering the public to hold people accountable”.

There are other systems already using satellites to detect methane, but Patrick Barker, Wood Mackenzie’s senior analyst for upstream oil and gas emissions, says MethaneSAT is unique in providing a combination of high sensitivity and wide coverage.

Existing satellites have either good spatial coverage but poor sensitivity to small facility-scale emissions, or are able to pick up small point source emissions at the cost of spatial coverage. MethaneSAT is the first satellite to copmbine the strengths of both types of existing systems, allowing detection of facility-scale emission events from 80% of the world's oil and gas-producing regions, and regular monitoring with a revisit time of three to four days.

Wood Mackenzie’s Barker said: “MethaneSAT will provide an unprecedented level of transparency in the form of a global, freely accessible emissions dataset, making the challenge of methane in the oil and gas industry easier to address but equally harder to ignore.”

The first data from MethaneSAT will arrive this summer, with the full publicly available data stream expected in early 2025.

If you are interested in digging deeper into methane detection technology and its implications for the energy industry, our Horizons report ‘Mission invisible: Tackling the oil and gas industry's methane challenge’ gives a great overview.

In brief

Investment in the US solar industry boomed last year, according to the latest US Solar Market Insight from Wood Mackenzie and the Solar Energy Industries Association. Installations of solar capacity in 2023 totalled 32.4 gigawatts DC, up 51% from the previous year. Solar accounted for 53% of all new electricity-generating capacity added to the US grid in 2023, making up over half of capacity additions for the first time. However, there were declines in residential solar in the fourth quarter, as the pipeline of projects in California sold under the previous more beneficial net metering rules was built out.

The US Securities and Exchange Commission has adopted new regulations intended to standardise and strengthen climate-related disclosures. The new rules require US listed companies to disclose climate-related risks that might have a material impact on their business, and the potential impacts of those risks on their strategy, business model, and outlook. They do not require companies to disclose Scope 3 emissions from their supply chains and the use of their products. The regulations are expected to face a series of legal challenges.

The dispute over Hess’s Guyana assets is heading for arbitration. Neil Chapman, an ExxonMobil senior vice-president, said at a conference on Wednesday that the company had filed a case with the International Chamber of Commerce in Paris, seeking a ruling on its right of first refusal over the stake owned by its partner Hess in the Stabroek block in Guyana. ExxonMobil argues that Chevron’s agreed US$53 billion acquisition of Hess means that it has the right to buy the Guyana assets under a change of control provision in the Starbroek joint operating agreement. Chevron and Hess reject that claim. ExxonMobil’s Chapman said the arbitration process could take up to six months. He added: “We’re extremely confident in our position that pre-emption rights exist under this contract.”

There is a price war in China’s electric vehicle market, with a range of new discounts and other offers for customers, after sales slowed at the beginning of 2024.

Other views

Why women are at the heart of a successful energy transition

Hydrogen: how carbon intensity rules can muddy the waters – Simon Flowers and Flor Lucia De la Cruz

The global nuclear SMR project pipeline has expanded to 22 GW, increasing more than 65% since 2021

Government tenders to drive 102 GW of global renewable capacity in 2024

US solar shattered records in 2023, but will this continue in 2024? – Michelle Davis

US distributed solar companies navigate economic headwinds – Amanda Colombo

The biggest topics in global upstream – Fraser McKay

Carbon management frequently asked questions part 1: emissions – Linda Htein

The global economy maintains momentum after upside surprise – Peter Martin

Amid explosive demand, America is running out of power – Evan Halper

Eight things to know about converting coal plants to nuclear power – the US Department of Energy

Vehicle to Grid: Network tariffs report – the Australian Renewable Energy Agency

Quote of the week

“Most traditional data centres that were built 10 years ago were 10 megawatts or less. Today, it’s not uncommon to see 100-megawatt data centres. And with our clients, we are talking about data centres that approach 1,000 megawatts. And they require 24/7 power. This is something that doesn’t get talked about enough, in my opinion…. Data centres are 24/7 consumers. We are 24/7 producers. So it’s kind of a perfect marriage. And then when we add on top of that our ability to provide clean energy to meet the sustainability objectives of [these companies], we think that there is an opportunity for us that is quite sizeable.” – Joe Dominguez, chief executive of Constellation Energy, talked on the company’s recent earnings call about its “exciting” prospects as the largest operator of nuclear power plants in the US.

As discussed in Energy Pulse last week, the rapid growth of data centres and the consequent rise in demand for zero-carbon electricity is creating both opportunities and challenges for the US power industry. Nuclear power is increasingly being discussed as one of the potential solutions.

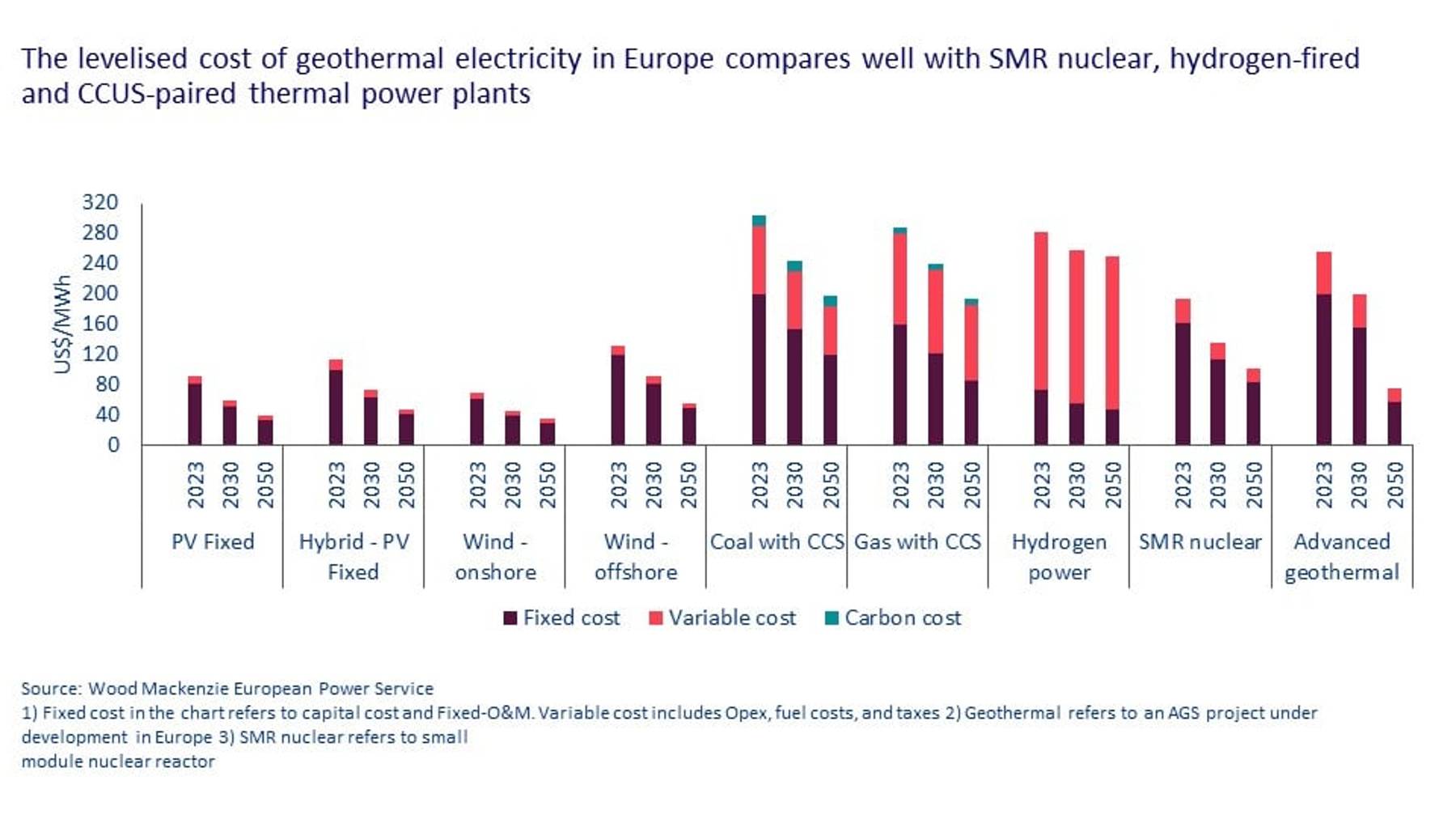

Chart of the week

This comes from a recent paper on geothermal energy by Wood Mackenzie’s Andrew Latham and Prakash Sharma. It shows comparisons of the levelised cost of electricity for a variety of low-carbon technologies, today and in 2030 and 2050. Advanced geothermal, over on the right-hand side, is clearly today much more expensive than solar and wind, even offshore wind. But compared to some other sources of “clean firm power” – dispatchable zero-carbon generation – such as hydrogen and fossil fuel plants with carbon capture, it is already competitive.

The outlook for 2050 is particularly interesting. We expect steep declines in the cost of advanced geothermal to make it highly competitive against small modular reactors, another possible source of clean firm power that is attracting considerable interest today.

{kind=link}

Get The Inside Track

Ed Crooks’ Energy Pulse is featured in our weekly newsletter, alongside more news and views from our global energy and natural resources experts. Sign up today to ensure you don’t miss a thing.